The report stated international brands such as Tim Hortons, Victoria's Secret, and Uniqlo continued to expand during Jul-Dec ‘22, despite global headwinds. As Tier II cities continued to gain popularity, Uniqlo opened its first store in Chandigarh, Tim Hortons entered Ludhiana, and Starbucks, Biba, and Shoppers Stop opened in Dehradun. During the second half of 2022, the American home furnishings shop chain Pottery Barn forayed in Delhi-NCR, opening two stores in rapid succession. Adidas opened their largest experience store in Delhi-NCR, and Zara, Nike, and Azorte are among the other companies that have launched experience/ flagship stores with a wide range of tech and other services in the city.

Fashion and apparel retailers continued to expand their footprint, accounting for a share of more than 42 percent in overall leasing in Jul-Dec ‘22. Other prominent categories that continued to drive leasing activity during Jul-Dec ‘22 included food & beverage (12 percent), along with hypermarket (7 percent) categories. The entertainment category, which was impacted the most during the pandemic, also emerged as one of the top demand drivers during Jul-Dec ‘22 with 6 percent share in overall space take-up.

Some prominent brands expected to launch in India over the next few months include Lavazza and Armani/Caffe from Italy, Jamba from the United States, and The Coffee Club from Australia.

The report elaborates how shoppers returned to physical retail as cities began reopening after tapering of COVID-19. Since then, shoppers have been increasingly opting for ‘hybrid commerce’ – which is essentially a mix of offline + online retail. CBRE’s Live-Work-Shop survey, whose findings will be released later this month, also indicated strong preference for offline + online retail, with more than 90 percent of respondents stating that they shopped via multiple channels. Despite the continued growth of online retail, ‘physical retail’ continues to gain prominence among Indian shoppers. As a result, strong footfalls led to expansionary space take-up by domestic and international retailers, especially during Jul-Dec ‘22. CBRE’s Asia Pacific Leasing Sentiment Survey (December 2022) also reported stronger expansionary sentiments among retailers since mid-2022.

According to the report, retail leasing activity surged by 5 percent to 2.43 million sq. ft in Jul-Dec ‘22 as against 2.31 million sq. ft. reported in Jan- Jun ’22 period. Overall, in 2022, leasing activity in the retail sector grew by 20 percent Y-o-Y to 4.7 million sq. ft.

Anshuman Magazine, Chairman & CEO - India, South-East Asia, Middle East & Africa, CBRE said, “The Indian retail sector is recovering, and we anticipate that it will continue to gain momentum through 2023. Even amid difficult global economic conditions, international brands are expanding not only in tier-I cities but also penetrating tier-II & III cities as they see India as a potential market."

Ram Chandnani, Managing Director, Advisory & Transactions Services, CBRE India stated, “As the cities started to reopen after the pandemic, many shoppers returned to physical retail and since then have adopted ‘hybrid commerce’. Sales in Jul-Dec ‘22 surpassed the pre-pandemic levels owing to increased consumer confidence, leading to a hike in spending. Leasing momentum is expected to further pick up in Jan-Jun ‘23 owing to anticipated space take-up in newly completed malls.”

Rental values inched up on a half-yearly basis in certain micro-markets across most cities, driven by robust retail demand. Among high streets, rents rose by about 4-8 percent across select locations in Delhi-NCR, Bangalore, by 4-12 percent in Ahmedabad, and by about 1-3 percent in Mumbai. Meanwhile, prominent mall clusters in Delhi-NCR and Bangalore witnessed rental growth of 3-15 percent and 2-6 percent respectively.

With the addition of two investment-grade malls totaling nearly 1.0 million square feet in Bangalore and Pune, supply addition during Jul-Dec ’22 increased by 129 percent on a half-yearly basis. Even though supply addition decreased by 69 percent Y-o-Y during the review period, pent-up supply is expected to become operational in the first half of 2023, and the overall supply for the year is predicted to exceed the pre-pandemic levels.

DMart is an unusual firm. It primarily operates two businesses, of which the supermarket one has been growing year-on-year. From FY 2023 to 2025, revenues grew by 34%, while net profit was up by 15%, impressive given the strong threat posed by the online grocery delivery segment in these years. However, the firm’s share price has largely remained stagnant during this period, especially because its grocery delivery business, started in 2017, has been facing significant losses year-upon-year. From ₨. 194 crore in FY 2023, the net loss widened to Rs. 247 crore in FY 2025.

Why does it happen that a firm which has such a strong competence in one segment of retail is unable to crack the code in another? While the new CEO and the management team would also be actively looking for the answer, it perhaps lies in DMart’s capabilities that give rise to its success in the supermarket business.

Firstly, what DMart excels at are activities such as vendor management and store operations, which essentially confer the competitive advantage in the supermarket business. Unfortunately, these are not the key success factors in the grocery delivery business, where the platform interface, number of dark stores, delivery fleet and speed, and the number of SKUs are of prime importance. Thus, simply put, the key problem is the limited applicability of DMart’s strengths in the other business, even though on the surface it might appear that the grocery delivery business is an extension of what the firm does in the supermarket business.

For instance, in the supermarket business, the customer walks the last mile, whereas in the grocery delivery business, the firm walks the last mile. The scenario is similar to the struggles experienced by film-based camera makers such as Kodak and Polaroid, who were expected to shift easily into digital cameras but struggled because the capabilities required were very different from their strengths (which were essentially in chemicals and film-making).

Secondly, DMart’s key differentiator in the supermarket business is its lowest prices. It primarily attracts price-conscious customers to its supermarkets and makes this a successful endeavour by consistently keeping its operating costs the lowest. Its key capabilities, such as bulk purchase of SKUs, fast payments to vendors and its ability to keep store running costs low, translate first into a cost advantage and then into the price advantage it enjoys over rivals.

However, since these are not the key cost drivers in the grocery delivery segment, the ability to offer the lowest prices in a profitable manner gets hampered. Thus, even if its prices may be the lowest amongst all grocery delivery players, since its costs are not, it must sell below cost, incurring a loss on each sale, unlike the supermarket business.

DMart’s challenge in the grocery delivery segment is somewhat similar to that of Ola Electric, which scaled its electric bike business without putting in place the commensurate capabilities required for success. While it sold more electric bikes than others initially, quality and service-related complaints soon surfaced, marking the beginning of a persistent slide that has continued till date. From being the market leader with a 35% share in late 2024, Ola Electric is down to single digits as per the January 2026 data.

So how should DMart approach its grocery delivery business? Patience and a slow scale-up will be the key strategic elements. While it entered the segment relatively late compared with others, ramping up its presence in the hope of catching up with them, without establishing the requisite capabilities, will only result in greater losses. Though it currently operates in 19 cities, it must first get the operating model right by gaining control over the necessary capabilities and only then attempt a nation-wide scale-up. Otherwise, in the absence of the requisite capabilities and a clear, profitable differentiator, scaling up will only result in continued losses of an even greater magnitude.

Authored By:

Kapil Khandeparkar, Associate Professor of Marketing, S.P. Jain Institute of Management & Research (SPJIMR)

Rohit Prabhudesai is an Associate Professor of Strategy and Consulting, Goa Institute of Management.

Father's Day gifting has evolved far beyond predictable presents and last-minute purchases. Today's consumers are increasingly choosing gifts that reflect their fathers' personalities and fit naturally into their everyday routines. From premium accessories and practical work essentials to smart lifestyle products and timeless fashion, the focus has shifted towards gifts that combine functionality with thoughtful intent. Whether your dad is always on the move, appreciates classic style, enjoys long drives, or loves creating memorable moments at home, these carefully curated picks celebrate his interests while adding comfort, convenience, and a touch of luxury to his daily life.

Best Father's Day Gifts for Dads Who Appreciate Style, Smart Living and Everyday Luxury

1. Que Retro Large Sunglasses by Que Universe

Some fathers rarely buy accessories for themselves despite appreciating timeless style. The Que Retro Large Sunglasses from Que Universe make for a thoughtful Father's Day surprise by combining retro-inspired aesthetics with everyday practicality. Designed to add personality to any look while offering protection during daily commutes, vacations, and weekend outings, the sunglasses strike a balance between fashion and functionality. Their versatile design makes them suitable across age groups and personal styles. For fathers who seldom indulge themselves, this accessory becomes more than a style statement—it is a reminder to enjoy life's simple pleasures with confidence and flair.

3. Laptop Bag by MR. D.I.Y

For fathers who are constantly on the move, balancing work commitments, travel, and everyday responsibilities, a functional laptop bag makes for a thoughtful and practical Father's Day gift. The Laptop Bag from MR. D.I.Y is designed to help dads carry their daily essentials with ease while maintaining a polished and professional look. Sleek, lightweight, and versatile, it is suitable for office commutes, business trips, and everyday errands alike. Combining style with convenience, the bag complements busy lifestyles and simplifies everyday organisation. For dads who are always juggling multiple roles, it is a useful gift that seamlessly blends practicality, functionality, and everyday sophistication.

4. Cruise Sunglasses by D'YAVOL X

For fathers who appreciate timeless style and a life well-travelled, Cruise by D'YAVOL X offers a sophisticated gifting option inspired by journeys and memorable experiences. Designed with a bold pilot silhouette and effortless versatility, the sunglasses are suitable for vacations, road trips, and everyday wear alike. Their contemporary yet classic design appeals to fathers who enjoy exploring the world and creating new memories. More than just an accessory, they symbolise adventures taken and experiences yet to come. For dads who appreciate premium style and meaningful experiences, Cruise makes for a Father's Day gift that feels both personal and aspirational.

5. Aérosonic Smart Car Fragrance Diffuser

For fathers who spend significant time on the road, whether commuting to work, travelling for business, or enjoying leisurely weekend drives, the Aérosonic Smart Car Fragrance Diffuser offers a thoughtful blend of convenience and luxury. Designed to elevate the in-car experience, it features intelligent motion-sensor activation, adjustable fragrance intensity, rechargeable cordless operation, and premium IFRA-certified fragrances. Its sleek, modern design integrates seamlessly into any car interior while keeping the cabin fresh and inviting. Practical yet sophisticated, the diffuser transforms routine drives into more enjoyable journeys, making it a meaningful Father's Day gift for dads who appreciate comfort and refined experiences.

6. XYXX Chambray Pyjama

The best gifts often become part of cherished moments, and the Chambray Pyjama from XYXX is designed exactly for that. Crafted from breathable fabric and featuring a relaxed fit, the loungewear is ideal for slow Sundays, movie marathons, and quality time spent with family. It offers all-day comfort without compromising on style, making it suitable for fathers who value ease and simplicity. Whether he is unwinding after a long week or spending time with loved ones, the pyjama celebrates comfort and togetherness. It is a practical gift that transforms ordinary moments at home into meaningful family memories.

7. Cantabil Father's Day Collection

For fathers who appreciate timeless style and versatile wardrobe essentials, Cantabil's curated Father's Day collection brings together thoughtful gifts that combine elegance and functionality. The collection includes a premium cotton-blend polo T-shirt designed for everyday comfort and durability, a Men's Mix Perfume Gift Set featuring four distinct fragrances for different moods and occasions, a sleek blue bifold wallet that balances practicality with sophistication, and a classic tie and pocket square set for formal dressing. Whether your father enjoys refined accessories, effortless casual wear, or polished occasion dressing, the collection offers versatile gifting options that celebrate his personal style while becoming part of his everyday routine.

8. Park Avenue Father's Day Edit

Park Avenue's Father's Day Edit brings together pieces from its FlexTech, SmartPress, Sport, and Festive collections to create a wardrobe designed for fathers who are constantly on the move. The FlexTech collection features advanced stretch fabrics engineered for ease of movement through dynamic workdays, while SmartPress shirts are crafted from wrinkle-resistant fabrics that maintain a crisp appearance with minimal upkeep. The collection also includes breathable seersucker pieces from the Sport range, textured festive shirts in refined shades, and a structured beige suit for special occasions. Designed to balance comfort, sophistication, and practicality, the edit offers versatile wardrobe solutions for every aspect of a father's lifestyle.

10. ECCO Offroad M Tex Lea Shoes & Flat Pouch City Crossbody Bag

Designed with comfort and functionality in mind, ECCO's Father's Day picks combine premium craftsmanship with everyday versatility. The Offroad M Tex Lea Shoes, crafted using FLUIDFORM technology, are designed for fathers who lead active lifestyles and appreciate footwear that transitions effortlessly between daily wear and travel. Complementing the shoes is the Flat Pouch City Crossbody Bag, a sleek leather accessory that offers convenient storage while adding a stylish touch to everyday looks. Together, these pieces make thoughtful gifts for dads who value practicality, comfort, and sophisticated design.

11. Alcatel V3 Ultra 5G

Many fathers are known for holding onto gadgets long after they have stopped performing efficiently. The Alcatel V3 Ultra 5G offers a meaningful upgrade through sleek design, powerful performance, and modern connectivity. Whether he is video-calling family members, watching cricket highlights, managing work responsibilities, or capturing precious memories, the smartphone supports everyday digital experiences with ease. For fathers who rarely spend on themselves despite relying heavily on technology, a smartphone upgrade can significantly improve convenience and communication. It is a practical and thoughtful gift that enhances both productivity and everyday enjoyment.

12. Wonderchef Luxe Multi C ook Kettle

ook Kettle

The Wonderchef Luxe Multi Cook Kettle combines elegance and versatility in a compact appliance designed to simplify everyday routines. Featuring a sophisticated ivory finish, the kettle is suitable for kitchens, home offices, and workspaces alike. Whether used for brewing tea, preparing instant noodles, making soup, or enjoying a late-night cup of hot chocolate, it offers multiple uses within a single appliance. Quick boiling, dual power modes, and thoughtful safety features further enhance convenience and flexibility. For fathers who appreciate practical gadgets that make everyday tasks easier, this kettle delivers comfort, functionality, and understated style.

13. FabIndia Brown Gulzar Mango Wood Wine Rack

For fathers who enjoy entertaining family and friends at home, the Brown Gulzar Mango Wood Wine Rack from FabIndia offers a combination of thoughtful design and functionality. Crafted from mango wood, the rack neatly stores bottles and stemware while adding warmth and character to interiors through its natural grain and elegant structure. Its foldable design enhances versatility, allowing it to fit comfortably into different spaces around the home. More than simply a storage solution, the wine rack becomes a statement piece for fathers who appreciate organisation, home décor, and the joy of hosting memorable gatherings with loved ones.

Market Insight

India's Father's Day gifting market is increasingly moving towards lifestyle-led and utility-driven purchases. Consumers are moving beyond symbolic gifts and choosing products that support hobbies, improve routines, and deliver long-term value. Fashion essentials, premium accessories, smart lifestyle products, and home experiences are emerging as popular gifting choices because they combine thoughtfulness with functionality and become part of everyday life rather than one-time celebrations. The growing preference for practical and experience-led gifting reflects a broader trend towards personalised purchases that celebrate individual interests and create lasting memories.

Conclusion

The most meaningful Father's Day gifts are often the ones that fit naturally into a father's daily life. Whether it is a stylish accessory, a practical work essential, a smartphone upgrade, a smart car accessory, or an elegant home piece, thoughtful gifting today is centred on products that add comfort, convenience, and enjoyment to everyday moments. This Father's Day, celebrate dads with gifts that recognise their personalities, passions, and the little routines that make them who they are.

FAQs

1. What are the best Father's Day gifts for dads who love fashion?

Wardrobe staples, sunglasses, shoes, and premium accessories make excellent gifts for style-conscious fathers.

2. What are some practical Father's Day gift ideas?

Laptop bags, smartphones, car accessories, and home essentials are practical gifts that become part of a father's everyday routine.

3. Are lifestyle and utility gifts popular for Father's Day?

Yes. Consumers are increasingly choosing products that offer long-term usefulness and align with their fathers' hobbies and routines.

4. What should I gift a father who already has everything?

Choose products that enhance everyday experiences, such as premium accessories, smart lifestyle products, or thoughtful home essentials.

5. Why are personalised lifestyle gifts becoming popular for Father's Day?

They combine functionality, comfort, and emotional value, making gifts feel more meaningful and relevant to the recipient's personality and daily life.

Father's Day gifting has evolved beyond wallets and coffee mugs. Today's consumers are increasingly choosing gifts that encourage fathers to slow down, prioritise themselves, and enjoy life's little indulgences. From premium coffee hampers and artisanal desserts to wellness supplements and grooming essentials, gifts centred around self-care are emerging as one of the biggest Father's Day trends. The appeal lies in their practicality—they fit naturally into everyday routines while showing thoughtfulness and appreciation. Whether your father is a coffee connoisseur, fitness enthusiast, wellness advocate, or someone who rarely buys things for himself, these carefully selected gifts are designed to make him feel valued long after Father's Day celebrations are over.

Best Father's Day Gifts for Dads Who Love Food, Wellness and Self-Care

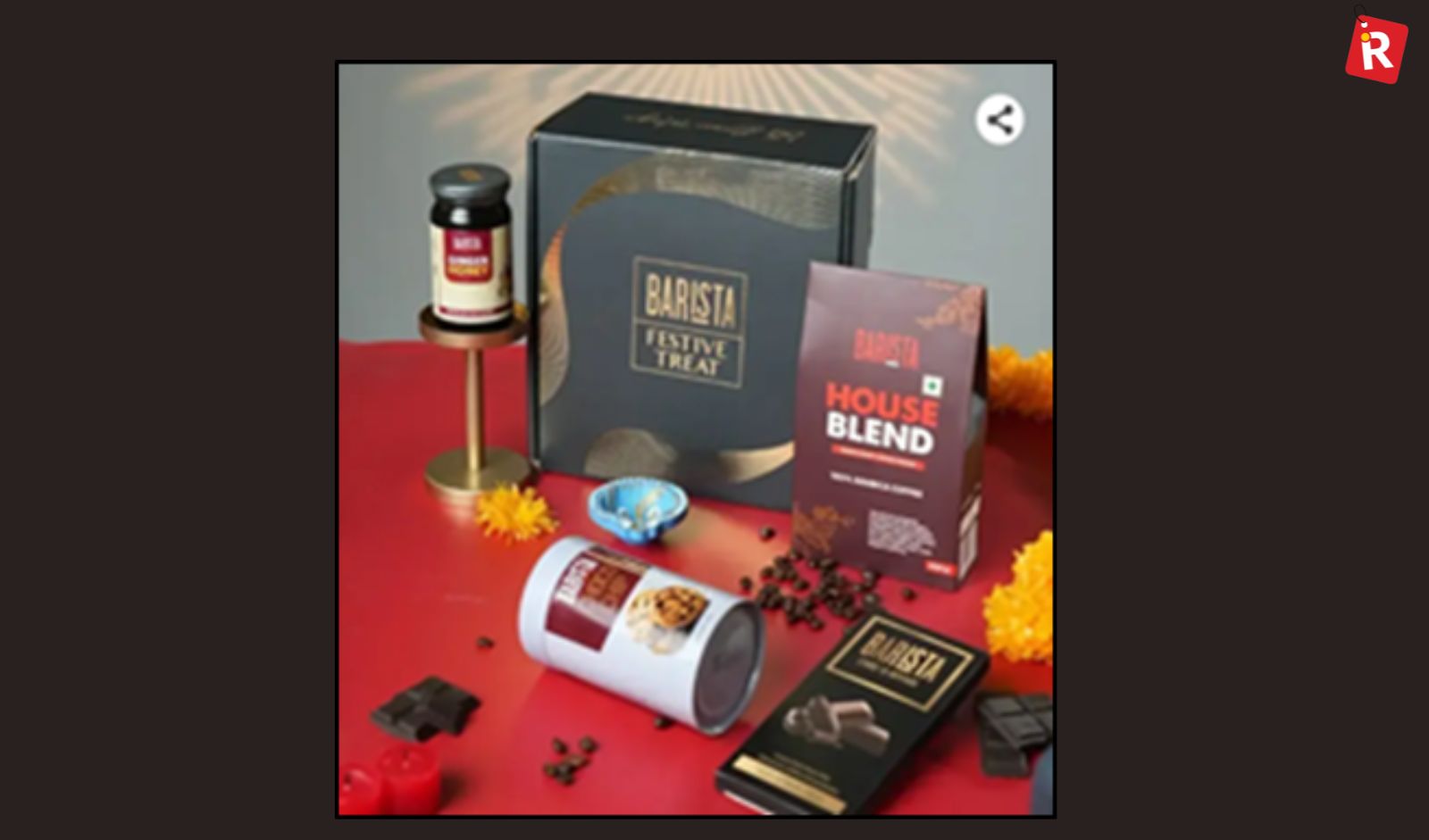

1. Barista Exotic Hamper

For fathers who treasure their morning coffee ritual, the Barista Exotic Hamper transforms an ordinary cup of coffee into a complete experience. The hamper includes the brand's signature House Blend coffee alongside a French Press, dark chocolate, cookies, ginger honey, and a decorative diya. The thoughtfully assembled collection encourages dads to slow down and savour quiet moments before the day begins. Rather than being just another gift basket, it celebrates the comfort of familiar routines and mindful indulgence. Ideal for coffee lovers who appreciate life's simple pleasures, this hamper is a meaningful way to elevate a daily ritual into a memorable Father's Day experience.

Read more: Skincare, Wellness and Pet Care Account for Over 80 Pc of D2C Orders in India

Top 8 Ready-to-Drink Protein Shake Brands Riding India’s On-the-Go Nutrition Trend

Top Air Coolers for Homes and Commercial Spaces This Summer

2. Bakingo Father's Day Collection

Bakingo's limited-edition Father's Day collection turns celebrations into delicious shared experiences. The range includes Father's Day Special Chocolate Cigars, the indulgent Rocher Brulee Cake inspired by classic French desserts, and a no-added-sugar Strawberry Rocher Pastry designed for guilt-free indulgence. Combining rich flavours, premium ingredients, and thoughtful craftsmanship, the collection caters to every kind of sweet tooth. These desserts are more than festive treats—they become the centrepiece of family celebrations and memorable conversations around the table. For fathers who enjoy desserts or families looking to create sweet moments together, Bakingo offers a gifting option that feels celebratory, personal, and indulgent.

3. Ubalance Naturals Liver & Kidney Revitalizer

For fathers who are increasingly prioritising preventive wellness and everyday vitality, Ubalance Naturals Liver & Kidney Revitalizer offers a holistic approach to supporting internal health. The Ayurvedic formulation is powered by Punarnava, a revered Rasayana herb known for its rejuvenating properties, and is enriched with Vitamin C, calcium, iron, and natural botanical ingredients. Designed to support the body's natural detoxification processes, it helps promote liver health, healthy kidney function, fluid balance, and nutrient absorption. By addressing concerns such as bloating, low energy, and dull skin through better digestion and internal balance, the supplement encourages fathers to make self-care and overall wellbeing an integral part of their daily routine.

4. Provilac High Protein Cacao Milk

For fitness-focused fathers who never miss a workout and encourage healthy living within the family, Provilac High Protein Cacao Milk combines nutrition with indulgence. Packed with high-quality protein and enriched with rich cacao flavour, the beverage supports muscle recovery and everyday nutritional requirements while delivering a satisfying taste experience. It fits seamlessly into active lifestyles, whether enjoyed after exercise, during busy mornings, or as an energising snack. The product celebrates fathers who value wellness and consistent self-improvement. By combining convenience, nutrition, and flavour, it makes for a thoughtful Father's Day gift that aligns perfectly with health-conscious routines and active living.

5. Healthy Master Collection

Healthy Master offers a wide range of flavourful snacks that transform everyday tea breaks and family moments into enjoyable experiences. The collection includes multi-millet ajwain cookies, crispy ragi chips, peri peri millet balls, traditional bhakarwadi, millet bhel, and roasted salted almonds. Designed for fathers who appreciate simple indulgences and delicious snacking experiences, these products combine familiar flavours with thoughtful ingredient choices. Whether enjoyed during work breaks, evening conversations, or movie nights with the family, the assortment caters to diverse preferences. The collection demonstrates that meaningful gifts do not need to be extravagant—they simply need to align with the recipient's everyday joys and routines.

6. The Body Shop Father's Day Gift Sets

The Body Shop's Father's Day collection celebrates self-care through thoughtfully curated gifting options from its bestselling Edelweiss, Ginger, Black Musk, and Maca Root & Aloe ranges. The Maca Root & Aloe set transforms shaving into a soothing ritual, while the Black Musk range offers a layered fragrance experience. The brand's Create Your Own Box option adds a personalised touch by allowing customers to curate bespoke combinations based on individual preferences. Rooted in ethical and nature-inspired beauty, these products encourage fathers to turn everyday grooming routines into moments of indulgence, relaxation, and care, making them meaningful gifts that extend beyond a single occasion.

7. L'Occitane en Provence Cade Range

L'Occitane en Provence elevates shaving from a routine task into a luxurious ritual through its Cade Rich Shaving Cream and Cade Refreshing Shaving Gel. Formulated with Cade essential oil derived from wild juniper from Provence, the products are designed to soften beard hair, calm the skin, and create a comfortable shaving experience. The cream delivers a rich lather and woody fragrance, while the gel provides a lighter, refreshing alternative suitable for warmer months and sensitive skin. These products appeal to fathers who appreciate premium grooming experiences and thoughtful details that make daily routines feel more indulgent and enjoyable.

8. Lonnue THRIVE Body Serum

Lonnue's THRIVE Body Serum brings facial-serum science to body care through a carefully curated blend of 33 ingredients. The lightweight formula contains niacinamide for tone-evening, hyaluronic acid for deep hydration, and vitamin E for antioxidant protection. Designed to absorb quickly without residue, the serum offers an elevated approach to body skincare that many men may not have previously considered. It is reef-safe, vegan, and cruelty-free, making it suitable for conscious consumers seeking high-performance products. For fathers who deserve products designed specifically for their wellbeing, THRIVE offers an opportunity to embrace self-care through a category that remains largely unexplored in men's grooming.

9. Shea Series Haircare Collection

The Shea Series is a shea butter-powered haircare range designed to deliver hydration, repair, and long-lasting nourishment across different hair types and concerns. The collection includes shampoos, conditioners, masks, oils, and reconstructive treatments enriched with keratin, amino acids, multi-vitamins, collagen, and advanced technologies. Dedicated products for wavy and curly hair focus on reducing frizz and improving definition, while the 18-MEA Collagen Therapy range addresses damage recovery and overall hair strength. For fathers who value grooming and hair health, the series offers targeted solutions that elevate everyday care routines and encourage investment in long-term hair wellbeing.

Explore more articles: 5 Smart Kitchen Appliance Brands for Everyday Use

Top 5 Supplements That Help Improve Appetite and Digestion Naturally

Best Slow Juicers in India for Summer

Market Insight

India's gifting market is increasingly moving towards wellness and experience-led purchases. Industry trends show rising demand for gourmet hampers, self-care products, functional wellness offerings, and premium grooming essentials, particularly during occasions such as Father's Day. Consumers are choosing gifts that fit naturally into daily routines and encourage healthier, more mindful lifestyles.

Conclusion

The most meaningful Father's Day gifts are often those that encourage dads to pause and prioritise themselves. Whether it's coffee, desserts, wellness products, grooming essentials, or flowers, thoughtful gifting today is increasingly centred on everyday care, comfort, and appreciation.

India's direct-to-consumer (D2C) shopping basket is undergoing a profound transformation. The products increasingly filling consumers' carts are no longer occasion-driven purchases such as jewellery or festive fashion, but categories centred around daily habits and recurring needs.

According to a new report by ClickPost, categories such as skincare, wellness, new-age fashion, pet care and sleep and comfort now account for 81.8 per cent of all D2C orders, signalling a decisive shift in the country's ecommerce landscape. The findings are based on an analysis of 50.8 million forward shipments across 62 Indian D2C brands spanning seven categories during FY2026, with comparisons drawn against FY2025 using a same-brand cohort methodology. India's ecommerce evolution is now being powered by products that consumers reorder, refill, restock and replace with increasing frequency.

Skincare and Wellness Lead the Frequency Economy

The scale of this shift is the most visible in the skincare category. The skincare brands averaged nearly 37,900 orders a day during FY2026, while jewellery brands averaged just under 6,000 orders daily. Around six skincare parcels reached consumers' doorsteps for every jewellery order delivered. The report suggests that while high-ticket categories continue to retain their significance, frequency of purchase has emerged as the defining metric of ecommerce growth.

Challenger categories are also significantly outpacing traditional segments in terms of growth. Sleep and comfort categories expanded at more than twice the pace of jewellery, while wellness grew nearly 2.7 times faster than conventional fashion. Categories that were virtually absent from mainstream commerce a decade ago are now emerging as some of the most dynamic drivers of India's digital retail economy.

Bharat Emerges as the Growth Engine for Digital-First Brands

The report also highlights how digital-native brands have achieved a geographical reach that often surpasses conventional retail channels. Smaller cities and towns have become the primary engine of D2C growth, with skincare brands now delivering to nearly 21,700 pincodes across the country, a footprint that is 9 per cent wider than conventional fashion. Around 44 per cent of wellness and skincare orders now originate from Tier III cities and beyond, reflecting the growing demand for categories that are often unavailable in local retail environments.

This deep penetration into Bharat is producing surprising consumption patterns. Jaipur, for instance, recorded one skincare or wellness order for every ten residents during FY2026, while Kanchipuram generated one new-age fashion order for every three residents. The findings underscore the extent to which smartphones and social commerce have democratised access to niche categories and enabled brands to cultivate demand far beyond metropolitan markets.

The Rise of Categories That Sell Beyond the Festive Calendar

Unlike traditional retail segments that typically witness sharp spikes during festive periods, habit-led categories are demonstrating remarkably stable demand throughout the year. Wellness brands averaged over 35,000 orders a day in July 2025, almost matching their November volumes during the Diwali season. Skincare orders in July even exceeded festive month volumes, indicating that these products have become routine household purchases rather than discretionary indulgences.

The same trend is visible in pet care and new-age fashion. Pet care brands maintained nearly 89 per cent of their Diwali order volumes even in July, reflecting the emergence of regular replenishment cycles among pet owners. New-age fashion retained 93 per cent of its festive demand during the same period, highlighting the consistency of categories built around social media-led discovery and continuous engagement.

Social Commerce Gives New-Age Fashion a Decisive Edge

Perhaps the most significant disruption has occurred within fashion itself. New-age D2C fashion brands shipped 11.83 million orders in FY2026, substantially ahead of the 7.05 million orders shipped by conventional fashion brands. Brands such as The Souled Store, Snitch and Bewakoof built their scale primarily through digital channels and social media communities long before establishing physical retail networks.

The report notes that these brands shipped 68 per cent more orders than traditional fashion players despite operating at lower average order values. New-age fashion recorded an average order value of ₹1,586 compared with ₹1,854 for conventional fashion, while also growing faster at 28 per cent versus 17 per cent. With social media now influencing a majority of retail purchase decisions in India, the report argues that digital feeds have effectively become storefronts and creators have become the new retail shelves.

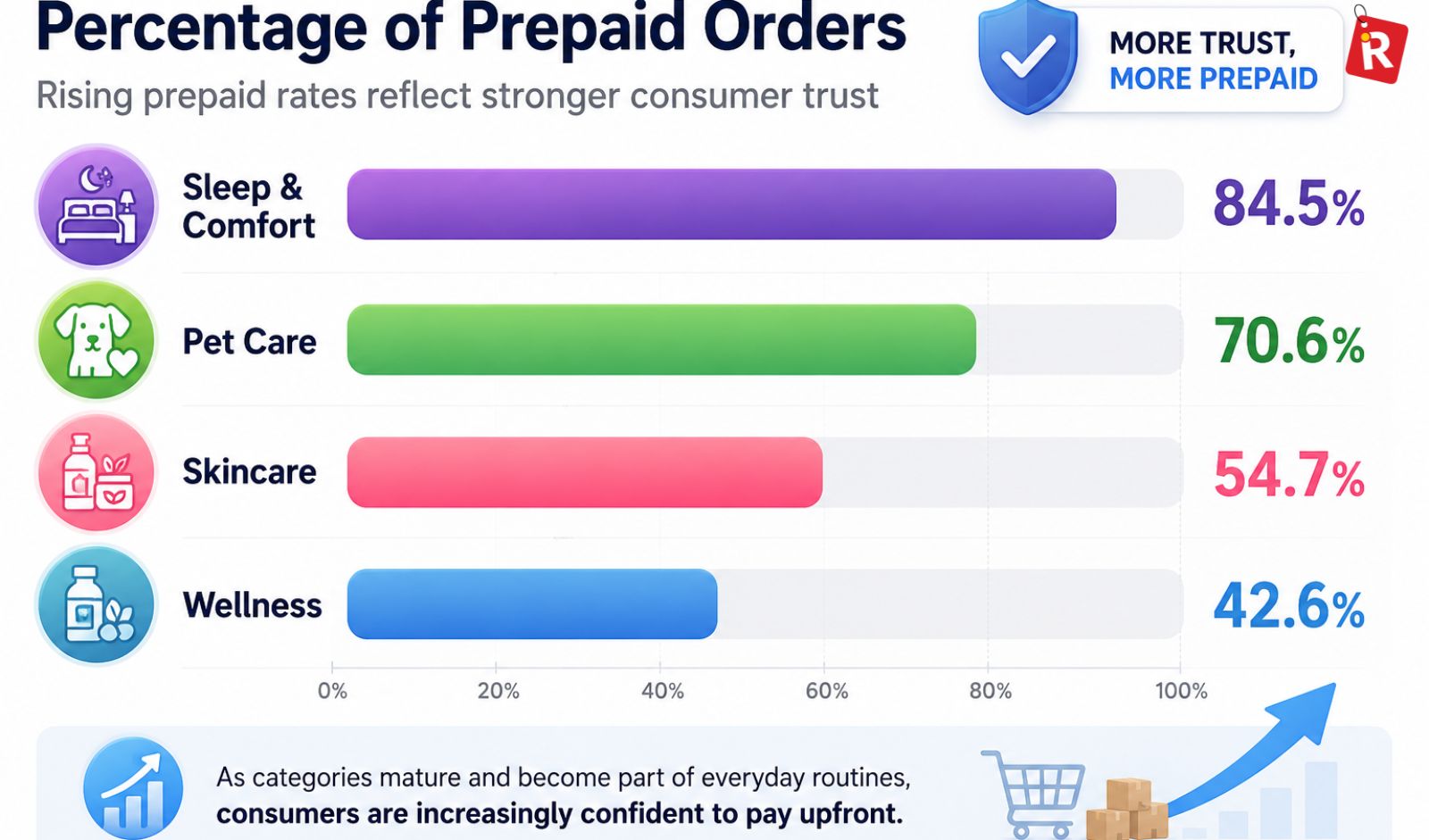

Consumer Trust and Spending Patterns Are Evolving

Consumer trust is also evolving alongside these shifts. The report uses prepaid transactions as an indicator of category maturity and customer confidence. Wellness currently records a prepaid rate of 42.6 per cent, reflecting its expansion into newer markets and first-time buyer cohorts. Skincare has reached 54.7 per cent, while pet care has climbed to 70.6 per cent. Sleep and comfort has emerged as the highest among challenger categories, with an 84.5 per cent prepaid rate.

Interestingly, jewellery also reports one of the highest prepaid rates at 83.6 per cent, suggesting strong consumer confidence despite its lower order frequency. However, the report points to the gap between online presentation and physical unboxing as one of the category's most pressing challenges.

A New Definition of Essential Spending

The report further shows that new categories like sleep and comfort products command an average order value of Rs 10,633, the highest among all emerging categories, while also recording the lowest return-to-origin rate. This indicates that consumers are making highly considered purchases in categories such as mattresses and sleep solutions, often treating them as investments in lifestyle and wellbeing.

Meanwhile, skincare and wellness have become regular household expenditures, with average order values of Rs 987 and Rs 1,074 respectively. Their recurring nature suggests that these categories are increasingly being incorporated into monthly budgets in much the same way as groceries and other everyday essentials.

India's D2C economy in FY2026 was defined by three parallel shifts: the rise of habit over occasion as replenishment categories dominated shipment volumes, the growing role of Bharat as the market driving repeat purchases and deeper category penetration, and the emergence of new forms of considered spending where consumers are increasingly willing to invest in personal wellness, sleep and self-care. The report concludes that India's ecommerce story is no longer merely about buying online; it is increasingly about building everyday consumption habits around categories that barely existed in mainstream retail a few years ago.

India’s protein conversation has shifted from niche fitness circles to everyday routines, and the market numbers reflect that change. IMARC estimates that India’s protein supplements market reached $912.9 million in 2025 and is projected to rise to $1.58 billion by 2034. At the same time, the latest government nutrition data shows that cereals still contribute 46-47 percent of rural protein intake and about 39 percent of urban protein intake, which underlines how strongly Indian diets still lean on basic staples for protein.

That gap between convenience and nutrition is exactly where the ready-to-drink protein shake category is gaining traction. For consumers searching for the best protein shake in India, the appeal is straightforward: no shaker, no prep, and a faster route to high-protein drinks during commutes, work breaks, post-workout windows, or travel. The result is a growing shelf space for protein beverages and protein drink brands in India that are building around portability as much as formulation.

Why Ready-to-drink Protein Shakes are Finding a Wider Audience

The new wave of ready-to-drink protein drinks is not only about muscle recovery. It is also about convenience, cleaner labels, and formats that fit into busy schedules. Some brands are leaning on dairy protein, others on plant protein, while a few are adding fibre, vitamins, caffeine, or functional ingredients to stand out. For shoppers comparing protein shake brands, the real decision now is less about whether to buy protein and more about which bottle matches their routine.

1. Yoga Bar

Yoga Bar has built one of the most visible ready-to-drink protein shake lines in India with its 26g Protein Shake range. The brand positions the product as a no-added-sugar drink with 26g of protein per 250ml bottle, designed as an easy top-up after workouts or during a busy day. It is available in flavours such as cold coffee and double chocolate, making it a familiar entry point for consumers who want a higher-protein option without moving too far away from a milkshake-style taste.

Read also: 5 Modern Nutrition Brands Transforming the Way India Consumes Protein on the Go

Top Air Coolers for Homes and Commercial Spaces This Summer

5 Smart Kitchen Appliance Brands for Everyday Use

2. Raw Pressery

Raw Pressery remains a strong name in protein milkshakes, especially for shoppers who prefer a fruitier or coffee-led profile. Its Banana Honey Protein Milkshake and Cold Coffee Protein Milkshake each carry 18g protein, are lactose-free, and are marketed as ready-to-drink options for everyday convenience. The brand has helped normalise the idea that a protein drink can sit somewhere between a wellness beverage and a regular snacking choice.

3. Phab

Phab has carved out space with its 18g Protein Milkshake range, which is sold in flavours such as vanilla almond, strawberry, chocolate, and cold coffee. The brand highlights no-added-sugar, gluten-free positioning, and gut-friendly ingredients, including fibre and prebiotics. That makes Phab relevant for consumers who are looking beyond simple protein counts and want a slightly broader nutrition story in their ready-to-drink protein shake.

4. Nuvie

Nuvie is one of the clearer examples of how protein beverage brands are borrowing from café culture. Its Protein Iced Latte, Chocolate Protein Shake, and Vanilla Protein Shake each deliver 20g protein, with lactose-free and no added sugar claims across the range. The coffee variant adds caffeine to the mix, which gives the line a stronger on-the-go, morning-commute appeal than a standard protein drink.

5. Not Rocket Science

Not Rocket Science is pushing a more functional angle with its Protein Punch range. The brand says each bottle delivers 26g dairy-based, lactose-free protein, zero added sugar, 4g gut-friendly fibre, and 280mg of KSM-66 Ashwagandha. With flavours such as vanilla, chocolate, and iced coffee, the brand is trying to appeal to consumers who want their protein drink brands in India to do more than just deliver protein.

6. Max Protein

Max Protein has moved beyond snack bars into the ready-to-drink protein shake space with its milkshake line. The Choco Burst and Berry Blush variants each deliver 26g protein per 250ml bottle, and the brand says the range is made without added sugar and palm oil. For shoppers already familiar with the Max Protein name, the move into bottles is a logical extension of its protein-first positioning.

7. JUST

JUST is keeping its pitch simple. The brand’s ready-to-drink protein shake comes in vanilla flavour and delivers 20g dairy-based protein with 0g sugar, no aspartame, and no preservatives. In a category where some products can feel overloaded with claims, JUST stands out by offering a straightforward protein beverage for people who want a clean, familiar format.

8. Maiva

Maiva is building a plant-based alternative in a category that has long been dominated by dairy. The brand says its protein drinks deliver 20g of clean plant protein along with 20 essential vitamins and minerals, and that the drinks are ready to consume without mixing. For consumers looking for nutrition drink brands that sit outside whey-heavy options, Maiva gives the segment a cleaner vegan and plant-based route.

Know more: Top 5 Supplements That Help Improve Appetite and Digestion Naturally

Best Slow Juicers in India for Summer

Best Spiritual Home Décor Brands to Watch For

What this category says about India’s nutrition habits

The rise of ready-to-drink protein beverages is not only a retail story. It reflects a larger shift in how urban consumers think about nutrition. The category is moving toward portability, smoother taste profiles, and format-led convenience, while the broader protein market continues to benefit from rising health awareness and stronger product innovation. In India, that creates room for both mainstream dairy brands and newer functional startups to compete for the same consumption occasion.

FAQs on Best Ready-to-Drink Protein Shake Brands

What is a ready-to-drink protein shake?

A ready-to-drink protein shake is a bottled or packaged protein beverage that can be consumed directly, without mixing powder or using a shaker. Many products are designed for travel, work, gym sessions, or quick meal gaps.

How much protein do these drinks usually contain?

In India, many ready-to-drink protein shakes fall in the 18g to 26g range per bottle, though exact numbers vary by brand and formula.

Are ready-to-drink protein drinks suitable for busy office schedules?

Yes. Their main appeal is convenience, since they do not need preparation and can be carried easily in bags or picked up during commutes and work breaks.

What should buyers check before choosing the best protein shake in India?

The label matters. Buyers should look at protein content per bottle, added sugar, lactose-free claims if needed, and whether the drink uses dairy or plant protein.

Can lactose-intolerant consumers consider these products?

Some can, but not all. Brands such as Raw Pressery, Nuvie, Not Rocket Science, and several others clearly highlight lactose-free positioning, while others are dairy-based and should be checked carefully on the label.

With Indian summers becoming increasingly intense, consumers are looking beyond traditional cooling solutions and opting for air coolers tailored to their specific needs. The market is witnessing a shift from one-size-fits-all products to specialised cooling appliances designed for different environments, ranging from compact urban apartments and family living rooms to large commercial spaces and industrial facilities.

Manufacturers are also focusing on energy efficiency, sustainability, durability, and convenience, introducing features such as honeycomb cooling pads, inverter compatibility, anti-bacterial technology, and larger water tanks. As a result, today's air cooler market offers products that cater to a wide spectrum of users, proving that effective cooling is no longer limited to a single category of appliance.

Why India's Air Cooler Market Is Shifting Towards Specialised Cooling Solutions

The modern consumer has increasingly specific cooling requirements. Urban apartment dwellers seek compact and aesthetically designed coolers that fit smaller spaces, while businesses and large establishments require powerful machines capable of cooling expansive areas. This has led manufacturers to diversify their portfolios and introduce products tailored to distinct use cases rather than relying solely on generic cooling solutions.

The trend is also being driven by rising electricity costs and growing awareness around sustainability. Consumers are prioritising energy-efficient products that deliver effective cooling while minimising power consumption and environmental impact. Consequently, brands are innovating across categories, introducing personal, desert, and commercial coolers that cater to varied lifestyles and budgets.

Air Coolers Designed for Every Space and Cooling Need

The latest generation of air coolers demonstrates how the category has evolved to address multiple consumer segments. Eco-friendly residential coolers, compact room coolers, and heavy-duty commercial units now coexist within the same market, offering buyers greater flexibility and choice.

Features such as anti-bacterial cooling pads, inverter compatibility, silent operation, easy mobility, and durable components have become key differentiators. Instead of merely offering relief from the heat, modern air coolers are increasingly being positioned as lifestyle and productivity solutions that enhance comfort across homes, offices, retail outlets, restaurants, and industrial facilities.

From compact room coolers designed for apartments to heavy-duty commercial coolers built for warehouses and large halls, the market is witnessing significant innovation. Consumers are increasingly looking for products that combine energy efficiency, portability, and high cooling performance without compromising on sustainability and durability.

Read more: Top 8 Ready-to-Drink Protein Shake Brands Riding India’s On-the-Go Nutrition Trend

5 Smart Kitchen Appliance Brands for Everyday Use

Top 5 Supplements That Help Improve Appetite and Digestion Naturally

Best Air Coolers for Summer 2026

1. Surya Roshni – Breezo and Chill Air Coolers

Surya Roshni has expanded its consumer appliances portfolio with the launch of its eco-friendly Breezo and Chill air cooler range. Designed for both residential and commercial applications, the series offers multiple variants with tank capacities ranging from 45 litres to 150 litres. The coolers feature high-efficiency honeycomb cooling pads with anti-bacterial properties, powerful air throw, and silent operation to enhance user comfort. Additional features such as inverter compatibility, pump protection technology, heavy-duty castor wheels, and easy-drain functionality make the range highly practical. Select models also feature 100% copper winding pumps and durable fan blades, making them suitable for diverse cooling requirements.

2. THERMOCOOL – Boss Commercial Cooler

The THERMOCOOL Boss Commercial Cooler is designed for users seeking industrial-grade cooling performance. Equipped with a large-capacity water tank and a powerful 24-inch commercial fan, the cooler is capable of efficiently cooling large halls, factories, warehouses, workshops, restaurants, and event venues. Its robust build and high air throw make it particularly suitable for commercial and semi-industrial environments where conventional residential coolers may prove inadequate. The large water reservoir enables longer operating hours with fewer refills, while the heavy-duty construction ensures durability and reliable performance under demanding conditions. It is a practical option for businesses prioritizing cooling efficiency and operational convenience.

3. Godrej – Edge MiniCool

The Godrej Edge MiniCool caters to consumers looking for a compact and stylish personal room cooler without compromising on functionality. Designed for rooms of up to 23 square metres, the cooler features mobility-friendly wheels, thermal safety mechanisms, and antibacterial cooling pads. One of its standout attributes is its transparent approach to specifications, with the brand highlighting a true water capacity measurement that factors in the overflow outlet, helping consumers better understand runtime expectations. Available in contemporary colour options, the Edge MiniCool breaks away from the conventional design language of cooling appliances. Its compact footprint and efficient performance make it particularly suitable for apartments, bedrooms, and smaller urban living spaces.

4. Symphony – Diet 3D Air Cooler

Symphony's Diet 3D Air Cooler continues to be a popular choice among consumers seeking an energy-efficient and space-saving cooling solution. The cooler is equipped with advanced honeycomb cooling technology and a three-side cooling pad design that enables better airflow and enhanced cooling efficiency. Its compact design makes it ideal for bedrooms, study rooms, and smaller apartments where space is a premium. The inclusion of features such as i-Pure technology for improved air quality and low power consumption further enhances its appeal. The Diet 3D range demonstrates how compact coolers can deliver effective performance while remaining economical and easy to use.

5. Crompton – Ozone Desert Air Cooler

The Crompton Ozone Desert Air Cooler is designed to address the cooling needs of medium to large rooms. Known for its high air delivery and large-capacity tank, the cooler offers prolonged cooling even during extreme summer conditions. The use of high-density honeycomb cooling pads improves cooling efficiency and moisture retention, resulting in better air circulation. Features such as inverter compatibility and easy mobility add to its practicality, particularly during extended power outages. The Ozone series has gained popularity among households seeking a balance between powerful performance, durability, and energy efficiency, making it a strong contender in India's growing air cooler market.

Know more: Best Slow Juicers in India for Summer

Best Spiritual Home Décor Brands to Watch For

Best Footwear Brands and Sneaker Destinations in India

Rising Demand for Energy-Efficient and Sustainable Cooling Solutions

India's air cooler market is witnessing strong growth, driven by rising summer temperatures, increasing electricity costs, and greater consumer awareness around energy-efficient appliances. Manufacturers are increasingly introducing products that incorporate eco-friendly materials, advanced cooling technologies, and features such as inverter compatibility and antibacterial cooling pads. There is also a noticeable shift towards specialised products catering to different use cases, ranging from compact room coolers for urban apartments to heavy-duty commercial coolers for industrial spaces. As consumers seek affordable and sustainable alternatives to air conditioning, the air cooler segment is expected to remain a key growth category in the home appliances market.

Conclusion

The Summer 2026 air cooler market offers a diverse range of products designed to cater to varying consumer requirements. Whether it is Surya Roshni's environmentally friendly Breezo and Chill series, THERMOCOOL's heavy-duty commercial cooler, Godrej's compact Edge MiniCool, or trusted offerings from Symphony and Crompton, consumers today have access to feature-rich and energy-efficient cooling solutions across categories. As innovation continues to shape the segment, choosing the right air cooler depends on room size, cooling requirements, and the desired balance between performance, convenience, and energy savings.

Frequently Asked Questions (FAQs)

1. Are air coolers more energy-efficient than air conditioners?

Yes. Air coolers generally consume significantly less electricity than air conditioners, making them a cost-effective option for summer cooling.

2. Which type of air cooler is best for large rooms?

Desert coolers and commercial coolers with larger water tanks and high air throw are better suited for large rooms and open spaces.

3. Do air coolers work during power cuts?

Many modern air coolers feature inverter compatibility, allowing them to operate seamlessly during power outages.

4. What features should consumers consider while buying an air cooler?

Important factors include tank capacity, cooling pad type, air throw, energy efficiency, inverter compatibility, mobility features, and maintenance requirements.

5. Are modern air coolers suitable for small apartments?

Yes. Compact personal room coolers with smaller footprints and efficient cooling technologies are specifically designed for apartments and smaller living spaces.

The modern kitchen has evolved into a multifunctional space where cooking, wellness, and convenience come together. As urban lifestyles become busier and homes increasingly adopt modular designs, smart kitchen appliances have become essential for simplifying daily routines while maintaining an organized and clutter-free environment.

Today's consumers are looking for appliances that offer efficiency, save time, and complement contemporary kitchen aesthetics. From intelligent cooking solutions to compact wellness gadgets, leading appliance brands are introducing innovative products that make everyday tasks easier and more enjoyable.

Why Smart Kitchen Appliances Are Becoming Everyday Essentials

The demand for smart kitchen appliances has grown significantly due to changing consumer preferences. Modern families seek appliances that not only perform multiple functions but also reduce effort, save space, and encourage healthier lifestyles. Features such as energy efficiency, easy maintenance, compact designs, and smart technology integration are now key factors influencing purchasing decisions.

The Rise of Functional and Space-Saving Kitchen Solutions

Modular kitchens prioritize clean designs and maximum functionality. Appliances that blend seamlessly into kitchen layouts while offering superior performance are increasingly preferred by homeowners. Whether it's a built-in cooking appliance, a high-performance blender, or a portable nutrition companion, smart appliances are redefining the way people interact with their kitchens.

Read more: Top 8 Air Fryer Brands Indians Are Buying in 2026

Top Air Coolers for Homes and Commercial Spaces This Summer

Best Slow Juicers in India for Summer

5 Smart Kitchen Appliances for Everyday Use

1. KAFF Appliances

KAFF Appliances has established itself as a leading name in premium kitchen solutions, offering products that combine aesthetics with functionality. Its product portfolio includes built-in matte finish hobs, auto-clean chimneys such as Lynn, Casto, and Vasco, built-in dishwashers, ovens, microwaves, and induction cooktops. Designed specifically for modular kitchens, these appliances help maintain clutter-free countertops and create a seamless cooking environment. The brand focuses on innovation, energy efficiency, and easy maintenance, making its products suitable for contemporary households seeking stylish and practical kitchen solutions that enhance both convenience and everyday cooking experiences.

2. Jaypee Plus

Jaypee Plus offers a thoughtfully curated range of kitchen appliances that combine functionality, wellness, and convenience for modern households. Its portfolio includes mixer grinders, personal blenders, electric kettles, food processors, and innovative solutions such as the Nutri Blend Turbo, Twister portable blender, and the CookSmart Electric Casserole. The Nutri Blend Turbo features a powerful motor and multiple jars for preparing smoothies, shakes, and everyday meal ingredients with ease. The compact Twister personal blender is designed for people with active lifestyles, enabling quick and convenient nutrition on the go. For cooking enthusiasts, the CookSmart Electric Casserole is a versatile 3-in-1 appliance that allows users to cook, reheat, and serve in a single stylish unit. Featuring a non-stick interior and a toughened glass lid, it simplifies meal preparation while reducing kitchen clutter. Together, these appliances reflect Jaypee Plus's focus on practical innovation, healthy living, and effortless everyday cooking experiences.

3. Philips

Philips is widely recognized for its innovative kitchen appliances that focus on healthier cooking and user-friendly technology. The brand's extensive product portfolio includes air fryers, mixer grinders, food processors, induction cooktops, coffee makers, electric kettles, and blenders. Its air fryers have gained popularity for enabling low-oil cooking while delivering convenience and versatility. Philips appliances are designed with intuitive controls, energy-efficient technologies, and compact footprints that fit seamlessly into modern kitchens. The brand continuously invests in innovation to help consumers simplify meal preparation while supporting healthier lifestyle choices and improving overall kitchen efficiency.

4. Bosch

Bosch has positioned itself as a premium appliance brand known for precision engineering and smart technology integration. Its kitchen appliance range includes built-in dishwashers, ovens, hobs, chimneys, refrigerators, and coffee machines. Bosch dishwashers are particularly valued for their water-efficient cleaning technologies and quiet operation, making them ideal for contemporary modular kitchens. The brand's products are designed to optimize space, reduce maintenance requirements, and deliver consistent performance. By integrating advanced features and elegant designs, Bosch offers kitchen solutions that cater to consumers seeking convenience, sustainability, and sophisticated living experiences.

5. Prestige

Prestige has become a household name by offering a diverse range of kitchen appliances tailored to everyday Indian cooking needs. Its product lineup includes induction cooktops, air fryers, mixer grinders, rice cookers, electric kettles, sandwich makers, and pressure cookers. The brand focuses on creating appliances that simplify daily cooking routines while maintaining affordability and functionality. Prestige induction cooktops and air fryers have gained widespread acceptance due to their ease of use, compact designs, and energy-efficient performance. With a strong understanding of Indian cooking habits, the brand continues to develop products that deliver convenience and versatility for modern households.

Know more: Top 8 Ready-to-Drink Protein Shake Brands Riding India’s On-the-Go Nutrition Trend

Top 5 Supplements That Help Improve Appetite and Digestion Naturally

Best Footwear Brands and Sneaker Destinations in India

Market Insights

The global smart kitchen appliance market is witnessing steady growth, driven by rapid urbanization, increasing disposable incomes, and rising awareness of healthy lifestyles. Consumers are increasingly investing in appliances that save time, conserve energy, and support multifunctional cooking experiences. The growing popularity of modular kitchens and compact living spaces has further accelerated demand for built-in appliances, portable blenders, air fryers, and smart cooking devices. Additionally, technological advancements and the integration of intelligent features are expected to shape the future of kitchen appliances, making convenience and connectivity key drivers of market expansion.

Conclusion

Smart kitchen appliances have become indispensable in modern homes, offering the perfect balance of functionality, efficiency, and aesthetics. Brands such as KAFF Appliances, Jaypee Plus, Philips, Bosch, and Prestige are continuously innovating to meet evolving consumer needs with products that simplify everyday tasks and enhance kitchen experiences. From built-in cooking solutions and auto-clean chimneys to portable blenders and healthy cooking appliances, these brands are helping homeowners create organized, efficient, and future-ready kitchens that support contemporary lifestyles.

FAQs on Smart Kitchen Appliance Brands

1. What are smart kitchen appliances?

Smart kitchen appliances are advanced devices designed to improve convenience, efficiency, and functionality through innovative technologies, compact designs, and user-friendly features.

2. Why are built-in appliances becoming popular in modular kitchens?

Built-in appliances create a seamless and organized appearance, maximize available space, and contribute to a clutter-free and modern kitchen environment.

3. Are air fryers suitable for everyday cooking?

Yes, air fryers are versatile appliances that support healthier cooking by using minimal oil while preparing a wide range of everyday dishes.

4. How do portable blenders benefit busy consumers?

Portable blenders allow users to prepare fresh smoothies and beverages conveniently, making them ideal for individuals with active and fast-paced lifestyles.

5. Which factors should be considered when choosing kitchen appliances?

Consumers should consider functionality, energy efficiency, ease of maintenance, available space, design compatibility, and whether the appliance aligns with their daily cooking and lifestyle requirements.

The last few years have seen a flood of cashback offers across India. Almost every new app, whether fintech, e-commerce, food delivery, or even some banks, was busy trying to outdo the other with instant rewards. “Sign up and get cash back”, “Pay now and earn instant discount” these lines became very common. And for some time, this strategy worked well. Many companies saw their user numbers grow fast and transactions pick up quickly.

But now, things are starting to look different. A lot of brands are realising that while cashback helped them acquire customers quickly, it has come at a heavy price. Marketing budgets are getting burnt fast, but the loyalty they were hoping for isn’t really showing up. This has led to a noticeable shift, as companies are slowly moving away from depending so much on discounts and looking at smarter, engagement-led approaches instead.

The Cashback Reality

Let’s be clear, cashback does have its advantages. Customers like getting money back, and it makes trying a new service feel less risky. For new players trying to break into tough markets, it has been a useful weapon to get noticed fast.

The problem, however, is who this money attracts. Too often, it brings in deal hunters people who keep jumping from one brand to another looking for the best offer. You spend a lot to bring them in, but they don’t stick around once the rewards dry up. This keeps acquisition costs high while lifetime value remains low.

Cashback tends to work better in categories where transactions happen often and don’t involve much thought. It doesn’t deliver the same results in areas where trust and long-term relationships matter more.

The biggest issue is this: cashback is quite good at bringing customers in especially during launches and big sales, but very poor at keeping them. Once people get used to discounts, they start waiting for the next offer before they make any transaction. Brands slowly get trapped in a cycle where they keep paying customers to use their service. They simply cannot be the main strategy for sustainable growth. Real loyalty takes time and needs consistent value.

Why Engagement Makes More Sense

That’s why more brands are now focusing on genuine engagement. Instead of giving the same flat offer to everyone, they are trying to understand their customers properly; their habits, needs, and what actually matters to them at different stages.

This means building a proper view of each customer across all channels. It means offering rewards that feel relevant and timely. Some brands are creating milestone benefits for regular users, personalised recommendations, or experiential rewards that add real value.

Many are also building bigger ecosystems where customers can earn and redeem points across different partners in shopping, travel, dining, entertainment and more. This makes the entire program much more useful in everyday life. Brands that have successfully made this transition are seeing significantly higher customer retention and stronger business results.

Making the Shift

This transition is not easy. It requires a fundamental change in mindset, moving away from the acquire-customers-at-any-cost approach.

Companies need to invest in strong customer data, design better journeys, and create meaningful rewards that truly resonate with people. It also demands patience. While short-term growth may slow down, the long-term benefits in retention, engagement, and profitability make it worthwhile.

The brands that succeed are those willing to play the long game.

Looking Ahead

Customers in India have become much smarter. They’ve seen too many cashback campaigns to get excited by them anymore. What they value now is brands that understand them and deliver consistent, meaningful experiences.

Loyalty is rarely built with one big discount. It grows through many small, relevant interactions over time that show the customer they matter.

This is the direction we are supporting our clients at Loylty Rewardz, helping them move beyond the burn of endless discounting and build engagement that drives real, sustainable growth. In my view, this shift is not just necessary, it’s long overdue.

Authored By

Amresh Acharya, Managing Director & Chief Executive Officer, Loylty Rewardz

India's relationship with garment care has always been deeply rooted in tradition. For generations, local dhobis formed the backbone of fabric care services across cities and towns. Their role extended beyond washing clothes; they were trusted custodians of wardrobes, serving households for decades through personal relationships and community trust.

However, as India has evolved into a consumption-driven economy, wardrobes have transformed significantly. The average urban consumer today owns a wider variety of garments than ever before, ranging from business wear and designer apparel to luxury ethnic clothing, premium casuals, leather accessories, and delicate fabrics requiring specialised treatment. This shift has fundamentally changed expectations from garment care providers.

The fabric care industry, estimated to be worth over ₹15,000 crore, is now witnessing the same transition that food delivery, mobility, and retail experienced over the last decade—from fragmented local operators to organised, technology-enabled brands focused on convenience, consistency, and customer experience.

Consumers no longer view garment care as a basic utility. It has become a service category where reliability, speed, transparency, and sustainability matter as much as cleaning quality.

One of the most visible changes in this evolution is the growing demand for convenience. Traditional models often required customers to physically visit retail outlets or coordinate manually with service providers. Today's consumers expect services to fit into their schedules rather than the other way around.

Speed, however, is only meaningful when combined with reliability. Garments entrusted for premium care require specialised handling and quality control. That is why operational processes must balance efficiency with precision. Through standardised workflows and technology-led operations, organised fabric care brands are increasingly delivering predictable turnaround times. At Pressmate.in, our target turnaround time is typically 72 hours, enabling customers to plan their wardrobe management with confidence.

Technology has emerged as the defining differentiator in this industry transformation. Historically, garment care was largely opaque. Customers had little visibility into where their garments were, what processes were being applied, or when they would be returned.

Modern fabric care platforms are changing that through end-to-end digitisation. Mobile applications now allow customers to schedule services, generate self-invoices, manage orders, and make payments seamlessly. Real-time notifications keep customers informed throughout the garment care journey.

Advanced tracking technologies are further improving transparency. RFID-based garment identification enables accurate tracking at every operational stage, significantly reducing errors and enhancing accountability. Geo-tagged pickups and deliveries provide greater visibility, while live order tracking ensures customers remain informed from pickup to delivery.

The result is a customer experience that mirrors the transparency consumers have come to expect from e-commerce and food delivery platforms.

Alongside convenience and technology, sustainability is becoming a central theme in the future of fabric care. The traditional laundry and cleaning industry has historically been resource intensive, particularly in terms of water consumption and packaging waste.

As environmental awareness grows, consumers are increasingly evaluating brands not only on service quality but also on their environmental impact.

At Pressmate.in, sustainability is integrated into operational decision-making rather than treated as a marketing initiative. One of the most significant examples is our adoption of advanced hydrocarbon cleaning technology. Unlike conventional cleaning processes that consume substantial amounts of water, our waterless garment care systems utilise solvent recovery mechanisms capable of recovering up to 99 percent of the cleaning solvent for reuse.

This approach delivers two important benefits. First, it ensures effective garment care for delicate and premium fabrics. Second, it significantly reduces freshwater consumption. Through these systems, Pressmate.in is projected to conserve approximately 35 lakh litres of water annually, contributing to responsible resource management in an increasingly water-stressed world.

Packaging is another area undergoing transformation. Polybags have long been an industry standard despite their environmental impact. Recognising the need for change, Pressmate.in has consciously moved away from conventional plastic packaging. Instead, we use compostable garment bags designed to degrade within approximately 180 days under suitable conditions. While seemingly a small operational change, such decisions contribute meaningfully to reducing long-term plastic waste.

The sustainability journey extends beyond garment processing and packaging. Last-mile logistics represent a growing source of urban emissions, particularly as service businesses expand. To minimise environmental impact, Pressmate.in's delivery operations are focused on electric vehicles, reducing dependence on fossil-fuel-based transportation while supporting cleaner urban mobility.

The evolution of India's fabric care industry reflects a broader shift in consumer expectations. Convenience is becoming non-negotiable. Transparency is replacing uncertainty. Sustainability is becoming a business imperative. And technology is transforming an industry that remained largely unchanged for decades.

Just as organised brands reshaped sectors such as food delivery, grocery commerce, and mobility services, the fabric care industry is entering a new era driven by innovation and customer-centricity.

The local dhobi will always remain an important part of India's service heritage. But the future belongs to organised, technology-enabled fabric care platforms capable of delivering superior convenience, consistent quality, environmental responsibility, and complete transparency.

India's wardrobes are evolving. The way we care for them must evolve too.

Authored By

Bajrang Saharan, Founder & CEO, Pressmate.in

Maintaining a healthy appetite and efficient digestion is essential for overall wellness, energy levels, and nutrient absorption. Poor digestion can impact metabolism, reduce nutrient uptake, and lead to fatigue, while a healthy appetite ensures the body receives adequate nutrition to support daily functions.

As consumers become increasingly health-conscious, there is growing interest in supplements that support digestive wellness and appetite management. From Ayurvedic formulations to protein-rich nutritional blends, a variety of products are designed to help improve gut health, stimulate appetite, and support overall metabolic function.

Why Appetite and Digestive Health Matter

A healthy digestive system plays a critical role in breaking down food, absorbing nutrients, and maintaining overall bodily functions. Digestive issues such as bloating, indigestion, poor appetite, and nutrient deficiencies can negatively affect quality of life and long-term health.

Supplements formulated with herbs, proteins, vitamins, minerals, and botanical extracts can help address these concerns by supporting digestive function, improving appetite, enhancing metabolism, and promoting better nutrient utilization. When combined with a balanced diet and healthy lifestyle, these products can contribute to improved energy, strength, and overall well-being.

Top 5 Supplements That Help Improve Appetite and Digestion

1. Ayuvya i-Gain+ Weight Gainer

Ayuvya i-Gain+ Weight Gainer is formulated to support healthy weight gain through improved appetite, digestion, and nutrient utilization. Designed around holistic wellness principles, the supplement helps the body absorb nutrients more effectively while supporting lean muscle development and overall strength. Its formulation works to naturally stimulate hunger and promote digestive efficiency, helping individuals meet their nutritional requirements consistently. By supporting metabolic function and energy production, it may also help reduce fatigue and improve overall vitality. Suitable for individuals seeking a balanced and sustainable approach to weight management, Ayuvya i-Gain+ focuses on promoting healthy weight gain rather than excessive calorie accumulation.

Read more: Best Slow Juicers in India for Summer

Best Spiritual Home Décor Brands to Watch For

Best Footwear Brands and Sneaker Destinations in India

2. Quista PRO Mass by Himalaya Wellness

Quista PRO Mass from Himalaya Wellness combines Ayurvedic ingredients with modern nutritional science to support healthy weight gain and digestive health. The supplement features a balanced carbohydrate-to-protein ratio designed to support muscle growth, repair, and recovery while providing sustained energy. It is enriched with essential vitamins, minerals, and botanical ingredients that help improve appetite, support digestion, and strengthen overall nutritional status. The formulation also aims to address common nutritional deficiencies that may affect energy levels and metabolic performance. By promoting better nutrient absorption and digestive function, Quista PRO Mass offers a comprehensive approach to healthy weight management and overall wellness.

3. Dabur Himalayan Shilajit Resin

Dabur Himalayan Shilajit Resin is a traditional wellness supplement derived from naturally occurring shilajit sourced from the Himalayan region. Rich in fulvic acid and trace minerals, it is widely recognized for supporting stamina, energy production, and metabolic balance. The formulation helps combat fatigue and supports the body's natural ability to absorb and utilize nutrients effectively. Its antioxidant properties may help reduce oxidative stress and support overall vitality. Regular use can contribute to improved endurance, better physical performance, and enhanced well-being. Carefully processed and tested for purity, Dabur Himalayan Shilajit offers a natural solution for individuals seeking greater strength, resilience, and digestive support.

4. Goodcare Garcinia Juice by Baidyanath

Goodcare Garcinia Juice is formulated using Garcinia Cambogia, a fruit known for its Hydroxycitric Acid (HCA) content and its role in appetite regulation. The supplement helps promote healthy eating habits by supporting appetite control and reducing unwanted cravings. It also assists the body's natural metabolism of fats and carbohydrates, encouraging balanced energy utilization throughout the day. Free from artificial additives, the formulation offers a simple and natural approach to digestive and metabolic wellness. Its refreshing composition can be easily incorporated into daily routines, making it suitable for individuals seeking long-term support for weight management, digestive health, and overall lifestyle improvement.

5. Oziva Protein & Herbs for Men

Oziva Protein & Herbs for Men combines clean protein sources with Ayurvedic herbs such as ginseng and green tea to support muscle development, stamina, recovery, and metabolic health. The formulation helps provide essential protein required for muscle repair while supporting sustained energy levels and physical performance. Herbal ingredients contribute additional wellness benefits by supporting digestion, metabolism, and overall vitality. Designed for active individuals, the supplement helps meet daily nutritional requirements while promoting better recovery following physical activity. Its balanced nutritional profile makes it suitable for those looking to support fitness goals, maintain energy levels, and improve overall health through a combination of protein and herbal nutrition.

Know more: Top 6 Talcum Powder Brands in India for Everyday Freshness and Comfort

5 Best Robot Vacuum Cleaners in India for Effortless Daily Cleaning

Best Tech Gadgets Every Student Needs to Stay Productive

Market Insights: Growing Demand for Digestive and Wellness Supplements

India's dietary supplement market continues to witness strong growth, driven by increasing awareness of preventive healthcare, nutrition, and holistic wellness. Consumers are increasingly seeking products that support digestive health, immunity, appetite management, and overall vitality. The growing popularity of Ayurvedic ingredients such as shilajit, herbal extracts, and plant-based formulations has further fueled demand across age groups. Additionally, rising interest in fitness, healthy weight management, and personalized nutrition is encouraging consumers to incorporate supplements into their daily routines. As a result, brands are expanding their portfolios with innovative formulations that combine traditional wellness principles with modern nutritional science.

Conclusion