Associate Editor, IndianRetailer.com & Retailer Media Jan 29, 2024 /

In the ever-evolving landscape of online shopping, the traditional dominance of metros and Tier I cities is undergoing a transformation. While comprising only 14 percent of the total population, these urban centers command a significant 43 percent share of online shoppers, according to a recent report by Alliance Bernstein. However, as the aftermath of the COVID-19 pandemic continues to unfold, growth patterns are experiencing a notable shift.

As we navigate the post-COVID era, the dynamics of online shopping are undergoing a profound transformation. The expansion into Tier II and beyond, the normalization of growth patterns, and the influence of seasonal trends underscore the resilience and adaptability of the online market. The evolving landscape presents both challenges and opportunities, making it imperative for internet companies to stay agile and responsive to ever-changing consumer behaviors.

Changing Trends

The overall monthly shopper base (MTUs) has surged, constituting 31 percent of Active User Base (ATUs), a considerable leap from the pre-COVID figure of 23 percent. This signals a maturation of the online user base, with an evident rise in the frequency of online shopping activities. Concurrently, internet companies are strategically expanding their supply chains into Tier II and beyond, capitalizing on improving consumer bases and ordering metrics in these cities.

Post-COVID Normalization of Growth

Across various internet sub-segments, user growth is gradually normalizing after the initial COVID-induced traction. Particularly, in severely under-penetrated markets like grocery delivery, which accounted for less than 1 percent of total grocery retail spend, there was a remarkable surge in active user base, peaking at an impressive 228 percent YoY growth in July 2022. Meanwhile, slightly mature sectors such as E-Commerce and Fashion continue to witness sustained growth rates, fueled by increased competition from a plethora of Direct-to-Consumer (D2C) platforms.

OTT's Uptick

The Over-The-Top (OTT) segment experienced an uptick towards the end of the year, showcasing a 10 percent increase in Monthly Active Users (MAUs) in July-23, which escalated to an impressive 55 percent increase in MAUs by November-23. This surge was attributed to the broadcast of World Cup screenings, especially in cricket (ICC World Cup, T20) and football (FIFA World Cup). Noteworthy gainers in this arena were Jio Cinema and Disney+Hotstar, boasting exclusive broadcasting rights.

Seasonality Trends

Three sectors have emerged as notable examples of strong seasonality trends. Firstly, in the realm of E-Commerce, the festive season in October drives the highest uptick in active user base, culminating in end-of-year sales across various categories. Secondly, Fashion Commerce, particularly apparel-led firms, experiences two festive seasons each year, with Q1 and Q3 being the strongest quarters, propelling user growth through end-of-season sales. Lastly, Digital OTT's key growth driver lies in sports content viewership, primarily cricket and football, with platforms like Jio Cinema and Disney+Hotstar securing exclusive broadcasting rights.

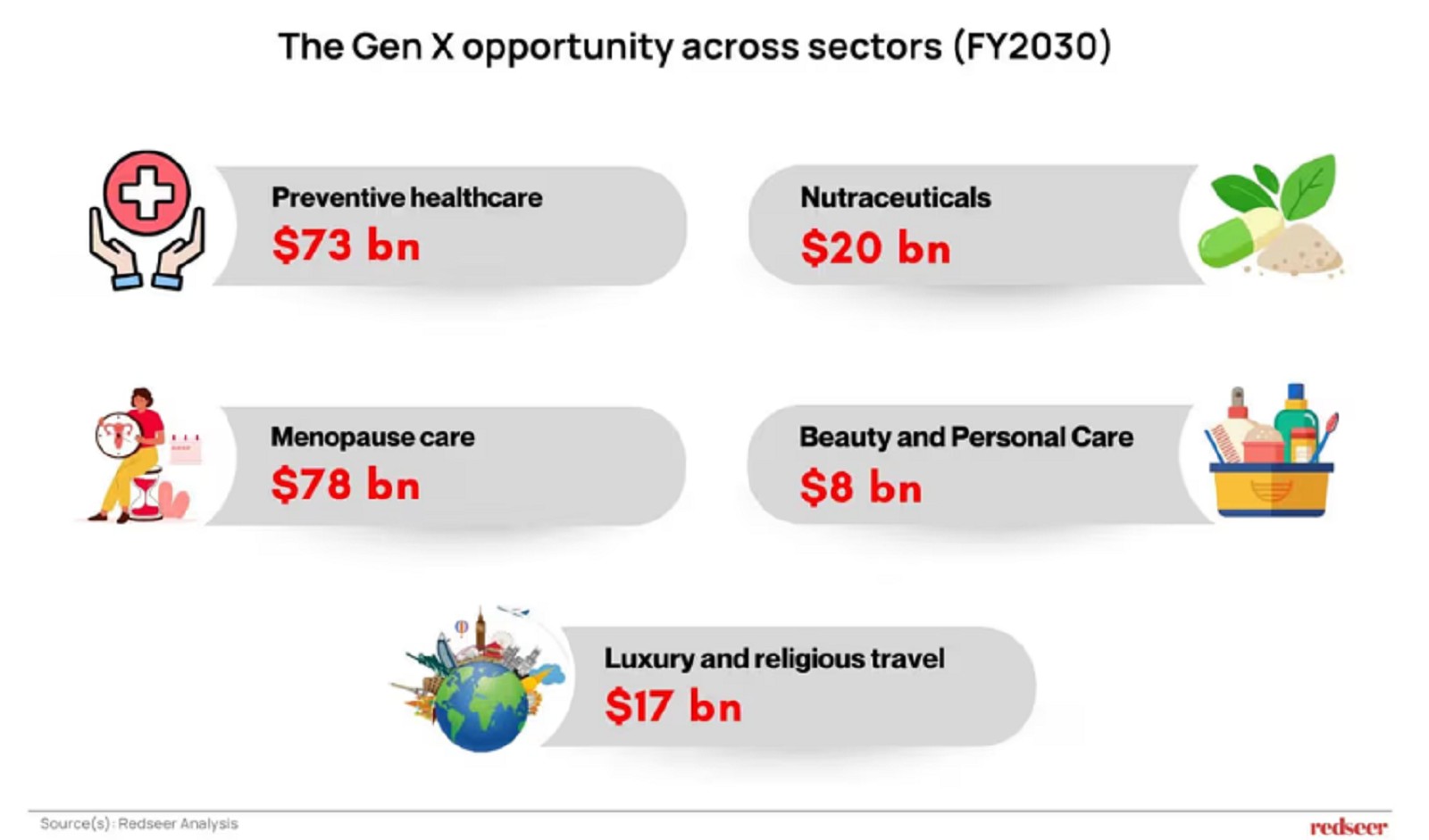

Gen X is projected to consume over $500 billion worth of goods and services by FY30. This significant scale is underpinned by a steady rise in per capita consumption and a unique combination of financial stability, digital fluency, and clarity of preferences. Unlike younger cohorts driven by discovery and trend cycles, Gen X is emerging as a more “sorted” consumer—one that prioritizes reliability, efficacy, and long-term value.

India’s consumption narrative is entering a new phase—one that is less about aspiration-led experimentation and more about purposeful, outcomes-driven spending. A recent report by RedSeer brings this shift into sharp focus. At the heart of this transformation lies Generation X, a cohort that has long operated under the radar but is now poised to become a defining force in shaping India’s premium consumption landscape.

Premiumisation Gets a Reality Check

One of the most striking insights from the report is the evolving definition of premiumisation. Traditionally associated with aspiration and status, premium consumption in India is now being recalibrated by Gen X to focus on credibility, convenience, and measurable outcomes. This cohort is less inclined towards impulsive purchases and more towards investments that deliver tangible benefits—whether in health, lifestyle, or personal well-being.

This shift is particularly visible in high-consideration categories such as healthcare, wellness, beauty, travel, and education. For brands, this signals a fundamental change in the rules of engagement. The era of loud marketing and rapid customer acquisition is giving way to a more nuanced approach centered on trust, consistency, and experience design.

Health and Wellness: From Reactive to Preventive

Gen X’s approach to health is perhaps the most telling indicator of this transition. Preventive healthcare spending is expected to reach $73 billion by FY30, growing at a robust 17 percent CAGR. This reflects a clear shift from reactive treatments to proactive, longevity-focused care.

Parallelly, the nutraceutical market is projected to grow even faster, reaching $20 billion by FY30 at a 25 percent CAGR. From supplements to functional foods, Gen X consumers are increasingly investing in products that promise everyday health optimization. The emphasis here is not on quick fixes, but on sustained outcomes—an approach that aligns with their broader consumption philosophy.

Read also Top Brands to Watch for Eid Gifting

Top 5 UK Beer Brands in India Gaining Popularity in the Premium Segment

Top 10 Trends Redefining Marketing in 2026

Beauty and Personal Care: Efficacy Over Trends

In the beauty and personal care (BPC) segment, Gen X is steering the market towards efficacy-led premiumisation. The Gen X BPC market is expected to touch $8 billion by FY30, driven by a clear preference for treatments over trends. This means a growing inclination towards scientifically backed products, dermatologically tested solutions, and personalized regimens.

For brands, this presents both an opportunity and a challenge. Success in this space will depend on the ability to build credibility, offer demonstrable results, and maintain consistency across customer touchpoints.

Travel: Comfort, Experience, and Indulgence

Travel is another category witnessing a noticeable shift in behavior. Gen X consumers are moving away from fast-paced itineraries to slower, more immersive experiences. This is reflected in the 25 percent year-on-year growth in alternative accommodations such as luxury villas and boutique stays.

Additionally, there is a strong preference for premium cabins and five-star accommodations, indicating a willingness to pay for comfort and quality. Travel, for Gen X, is no longer just about exploration—it is about indulgence, relaxation, and meaningful experiences.

Education: The Ultimate Legacy Spend

Education continues to remain a cornerstone of Gen X spending, often viewed as a “legacy investment.” Urban families are reportedly spending between Rs 10–20 lakh per child annually, with a growing inclination towards international curricula such as Cambridge and IB, as well as overseas education programmes.

This underscores the cohort’s long-term orientation and its focus on creating enduring value—not just for themselves, but for the next generation.

What This Means for Retail and Brands

As India’s retail market moves closer to the trillion-dollar milestone, the influence of Gen X will become increasingly pronounced. This cohort’s preference for outcomes-led consumption necessitates a shift in how brands approach product development, marketing, and customer engagement.

Trust-building will be paramount. Brands will need to invest in superior service design, ensure consistency across channels, and deliver on their promises with precision. Personalization, backed by data and insights, will play a crucial role in enhancing customer experience and driving retention.

Moreover, the emphasis will shift from short-term acquisition metrics to long-term value creation. Repeat behavior, customer loyalty, and margin resilience will become key indicators of success in this new consumption paradigm.

Know more: Top 5 Best Brands Offering Pedicure Kits to Try at Home

Top 5 Perfumes for Men and Women to Elevate Your Signature Scent

Best Hair Removal Cream Brands Gaining Strong Demand Across India

The Road Ahead

Gen X may have been an understated force in India’s consumption story so far, but its impact over the next decade will be anything but subtle. As this cohort continues to expand its spending across high-value categories, it will redefine what premium truly means in the Indian context.

For businesses and investors alike, the message is clear: the future of premium consumption lies not in aspiration alone, but in delivering consistent, credible, and outcome-driven value. In this evolving landscape, those who can align with the expectations of the “Sorted Generation” will be best positioned to build enduring brands and sustainable growth.

Introduction

In today’s fast-growing online trading world, selecting a trustworthy broker is crucial. EO Broker is a modern trading platform offering access to stocks, forex, commodities, indices, ETFs, and cryptocurrencies. With a focus on user experience and advanced trading tools, the platform caters to both beginner and experienced traders.

This review examines whether EO Broker is legitimate, safe, and trustworthy. This includes account types, trading instruments, security measures, withdrawal procedures, and user experience. We'll also answer common questions: Does EO Broker actually pay out? Is it a scam? Does EO Broker comply with Islamic financial principles?

Company Overview

EO Broker was established to provide traders with a secure and easy-to-use platform. Its intuitive interface, broad range of financial instruments, and educational resources make it appealing to traders.

The platform also features real-time market analytics, social trading options, and customizable trade durations, offering flexibility for users who value both reliability and advanced functionality.

Licensing and Compliance

EO Broker emphasizes regulatory compliance and security. Operating internationally, the brokerage implements KYC (Know Your Customer) procedures to verify client identities and protect against fraud.

Key Security Measures:

- SSL encryption for data transmission

- Segregated client accounts

- Internal audits to ensure compliance

- The platform is a registered member of The Financial Commission, reflecting a commitment to high standards of client service and fair business practices.

Is EO Broker Legit or a Scam?

With the rise of online scams, verifying legitimacy is crucial. EO Broker has earned a reputation as a trusted platform. Verified user reviews, successful withdrawals, and consistent platform performance indicate that EO Broker is not a scam.

Unlike fraudulent brokers, EO Broker does not make unrealistic promises or pressure users into high-risk trades. It focuses on providing a transparent and secure trading environment.

Does EO Broker Really Pay?

Yes, EO Broker reliably pays verified users. Withdrawal times depend on the chosen method, but most transactions are completed within 1–3 business days.

Supported Payment Methods:

- Cards: Visa, MasterCard, Maestro

- Bank Transfers: Wire and local bank options

- E-wallets: Skrill, Neteller, Paytm, PhonePe

- Cryptocurrencies: Bitcoin, Ethereum, USDT

The platform has a low minimum deposit, typically $10, and trades can start from $1, making it accessible for beginners.

Trading Platform Review

Web Platform

EO Broker’s web platform is fast and user-friendly, offering:

- Real-time market data and charts

- Multiple technical indicators including RSI, MACD, Bollinger Bands

- Customizable trade durations from 1 minute to several hours

- Social trading options to copy successful traders

- Embedded educational resources

Mobile App

The EO Broker mobile app for iOS and Android offers full platform functionality on the go:

- Real-time alerts and notifications

- Portfolio management and trade execution

- Access to educational materials

- Social trading and market news updates

Demo Account

EO Broker provides a demo account with virtual funds for risk-free practice. Features include:

- $10,000 virtual money

- Access to all trading instruments

- Practice of strategies and analysis tools

The demo account helps beginners gain confidence before starting live trading.

Account Types

EO Broker offers several account tiers for different trader levels:

|

Account Type |

Minimum Deposit |

Benefits |

|

Micro |

$10 |

Basic trading access |

|

Basic |

$50 |

Standard features |

|

Silver |

$500 |

Increased maximum deal amount, more simultaneously opened deals |

|

Gold |

$2,500 |

$1000 maximum deal amount, more simultaneously opened deals, Priority withdrawals |

|

Platinum |

$5,000 |

$2000 maximum deal amount, Unlimited simultaneously opened deals, Priority withdrawals |

Accounts can be upgraded automatically as deposits increase, unlocking additional features and benefits.

Trading Instruments

EO Broker offers over 100 instruments, including:

- Stocks: Apple, Microsoft, Tesla, Amazon, Google

- Forex: EUR/USD, GBP/USD, USD/JPY, AUD/USD

- Commodities: Gold, Silver, Oil

- Cryptocurrencies: BTC/USD, SOL/USD, DOGE/USD, BNB/USD

This diversity allows traders to build balanced portfolios and explore multiple markets.

Security and Safety Measures

EO Broker implements comprehensive measures to protect users:

- SSL encryption

- Two-factor authentication (2FA)

- Segregated client accounts

- Regular compliance checks

These measures ensure a safe and reliable trading environment.

Trading Tools & Features

- Technical indicators for market analysis

- Economic calendar and news updates

- Social trading and copy trading

- Customizable trade durations

- Risk management tools

These features help traders make informed decisions and develop successful strategies.

Education & Resources

EO Broker provides extensive educational resources:

- Video tutorials for beginners and advanced users

- Step-by-step strategy guides

- Webinars by professional traders

- Market analysis articles

The education section helps users improve skills and make informed trading choices.

User Experience & Support

EO Broker offers 24/7 support:

- Live chat for immediate assistance

- Email support for detailed queries

- FAQ and tutorial section

Users report smooth verification, fast withdrawals, and responsive customer service.

Compliance with Islamic Financial Principles

EO Broker offers a transparent, riba-free trading environment that is consistent with core Islamic financial principles. The platform emphasizes skill-based and knowledge-driven trading rather than speculation, and there are no interest charges or overnight swap fees. Traders have full control over their positions, can view all trade details in advance, and can use educational resources and a demo account to safely practice strategies.

Whether trading currencies, stocks, or commodities, EO Broker ensures ethical, fair, and responsible trading, making it a trusted choice for users who adhere to Islamic financial principles.

Reputation

EO Broker has built a positive reputation:

- Reliable withdrawals and payouts

- User-friendly interface and trading tools

- Transparent trading conditions

- Engaging features such as social trading and demo accounts

Tips for Beginners

- Start with the demo account for practice

- Learn basic technical analysis

- Diversify trades across assets

- Use small trade sizes initially

- Verify account before withdrawals

Common Mistakes to Avoid

- Over-investing or chasing unrealistic profits

- Ignoring risk management strategies

- Following unverified trading advice

- Trading based on emotions

Conclusion

Is EO Broker safe and legitimate?

Yes. EO Broker is a secure, transparent, and reliable trading platform. It offers verified payments, demo accounts, a riba-free environment, and extensive educational resources. Both beginners and experienced traders can access the tools, features, and guidance needed for effective online trading.

Risk Warning

Trading and investing involve a high level of risk and may not be suitable for all clients. Carefully consider your investment objectives, experience level, and risk tolerance before buying or selling. Trading carries financial risk and could result in partial or complete loss of funds. Only invest what you can afford to lose. Understand all associated risks and consult an independent financial advisor if in doubt.

Online trading has rapidly grown into one of the most popular investment methods today. Whether your goal is to diversify your income, explore financial markets, or develop trading skills, selecting a trustworthy brokerage is crucial. ExpertOption is a global platform that provides access to a broad range of instruments, including stocks, forex, cryptocurrencies, commodities, and ETFs.

A common question among potential traders is whether ExpertOption is legitimate, safe, or a scam. This review takes a close look at the platform’s features, security protocols, account options, trading tools, and withdrawal procedures. We also examine its payment reliability, compliance with islamic principles, and suitability for both novice and experienced traders.

Serving millions of users worldwide, ExpertOption strives to deliver a secure, user-friendly, and engaging trading environment. This review evaluates all aspects of the brokerage to help you make informed decisions before committing your funds.

Company Overview

Established in 2014, ExpertOption has built a reputation as a reliable online brokerage, serving traders across several continents. The platform caters to both beginners and experienced traders, offering an intuitive interface, innovative features, and educational tools designed to enhance trading knowledge.

One standout feature is the Achievements and Trading Battles system, which gamifies the trading experience and encourages active participation. Traders can earn rewards by reaching milestones, completing challenges, and competing with peers, fostering motivation and discipline.

With support for multiple languages and local payment methods, ExpertOption ensures accessibility for users worldwide. The platform is committed to transparency, trustworthiness, and continuous enhancement of its trading experience.

Licensing and Compliance

Security and regulation are critical in assessing a broker’s legitimacy. ExpertOption implements strict KYC (Know Your Customer) policies. All accounts are verified to ensure secure access and reduce fraud risk.

While ExpertOption is registered in some countries and does not hold licenses in every region, it implements the following security measures:

- SSL encryption for secure transactions

- Segregated client accounts to protect funds

- Regular internal compliance audits

Due to local regulations, the platform is restricted to the markets it services, operating legally only where permitted. These measures help build trust and maintain a safe trading environment.

Legitimacy: Is ExpertOption Safe or a Scam?

Fraud is a common concern in online trading, but verified user feedback, documented withdrawals, and independent reviews confirm that ExpertOption is a legitimate platform.

It ensures transparency in deposits, trades, and withdrawals, while offering features such as social trading, educational resources, and a demo account. Unlike scam brokers, ExpertOption does not make unrealistic profit claims or offer shortcuts, focusing instead on delivering a secure and reliable trading environment.

Does ExpertOption Really Pay?

A common question is whether ExpertOption reliably pays users. Verified withdrawals and community feedback confirm that the brokerage processes payments consistently.

Typical withdrawal time: 1–2 business days, depending on the method.

Available payment methods:

- Credit/Debit Cards: Visa, MasterCard, Maestro

- Bank Transfers: Wire transfer and local options

- E-wallets: Skrill, Neteller, Paytm, PhonePe

- Cryptocurrencies: Bitcoin, Ethereum, USDT

Minimum deposits are $10, and trades can start from $1, making the platform accessible to new traders. Verified accounts report fast and secure withdrawals.

Trading Platform Review

Web Platform

ExpertOption’s web platform is intuitive and responsive, offering:

- Real-time charts with 10+ technical indicators

- Customizable trade durations from 1 minute to several hours

- Social trading to follow and copy successful traders

- Gamification through Achievements and Trading Battles

- Educational resources for all levels

Mobile App

The iOS and Android apps replicate the desktop experience, including:

- Real-time market updates

- Push notifications and trade alerts

- Full functionality, including social trading and account management

- Educational tutorials and news updates

Demo Account

ExpertOption provides a demo account with $10,000 virtual funds, allowing users to:

- Practice trading strategies risk-free

- Explore all platform features

- Gain confidence before moving to live trading

The demo account is unlimited in duration, letting users learn at their own pace.

Account Types

ExpertOption offers six account tiers to suit different traders:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Accounts automatically upgrade when deposit thresholds are reached, unlocking additional benefits.

Trading Instruments

ExpertOption provides 100+ trading instruments:

- Stocks: Apple, Tesla, Google, Microsoft, Meta

- Forex: EUR/USD, GBP/USD, USD/JPY, USD/CAD

- Commodities: Gold, Silver, Oil

- Cryptocurrencies: BTC/USD, SOL/USD, DOGE/USD, BNB/USD

These instruments allow traders to diversify portfolios, manage risk, and identify emerging trends. ExpertOption also offers tutorials on market analysis, technical indicators, and trading strategies.

Security Measures

ExpertOption prioritizes user safety:

- SSL encryption for secure data transmission

- Two-factor authentication (2FA)

- Segregated client accounts

- Regular security audits

These measures ensure a secure and trustworthy trading environment.

Trading Tools and Features

- Technical indicators: RSI, MACD, Bollinger Bands

- Market news and economic calendar

- Social trading and copy trading

- Achievements and Trading Battles

- Customizable trade durations

These features help traders make informed decisions, improve strategy efficiency, and increase engagement.

Education and Resources

ExpertOption offers extensive educational materials:

- Video tutorials for beginners and advanced users

- Step-by-step guides and articles on strategies

- Webinars hosted by professional traders

- Detailed market analysis tools

These resources help users improve trading skills and make informed decisions.

User Experience and Support

ExpertOption provides 24/7 multilingual support:

- Live chat for instant assistance

- Email support for complex issues

- Knowledge base with FAQs and tutorials

Users report high satisfaction with verification, withdrawals, and responsive customer service.

Conformity to Islamic Financial Principles

ExpertOption offers a transparent, interest-free trading environment that does not take or give riba and conforms to ethical trading principles. The platform emphasizes skill, analysis, and responsible decision-making, while its demo account and educational resources allow users to safely practice strategies and trade with confidence.

Reputation

ExpertOption has a positive reputation among online traders:

- Verified payments and reliable withdrawals

- User-friendly interface and functional tools

- Transparent trading conditions

- Engaging features such as social trading, Achievements, and Battles

Tips for Beginners

- Use the demo account to practice trading

- Learn basic technical indicators

- Diversify investments across assets

- Start with small trades to manage risk

- Verify your account before withdrawals

Common Mistakes to Avoid

- Over-investing or chasing profits

- Ignoring risk management

- Blindly following other traders

- Overtrading or making emotional decisions

Conclusion

Is ExpertOption safe and trustworthy?

Yes. ExpertOption is a safe, reliable, and legitimate trading platform, suitable for both beginners and experienced traders. With verified payments, educational resources, demo accounts, social trading, and account options compliant with Islamic financial principles, it is one of the leading brokers globally.

Risk Warning

Trading and investing involves a significant level of risk and is not suitable and/or appropriate for all clients. Please make sure you carefully consider your investment objectives, level of experience and risk appetite before buying or selling. Buying or selling entails financial risks and could result in a partial or complete loss of your funds, therefore, you should not invest funds you cannot afford to lose. You should be aware of and fully understand all the risks associated with trading and investing, and seek advice from an independent financial advisor if you have any doubts.

In the increasingly crowded world of online retail, video has become the secret weapon that distinguishes high-performing e-commerce brands from everyone else. Product pages that include video consistently show higher engagement, better Time on Page, and significantly improved conversion rates. That’s because video marketing is able to achieve a level of engagement that just simply cannot be matched by static images – especially in the context of e-commerce sales, where it’s vital that brands can demonstrate value, set expectations, answer questions before they’re asked, and build trust at scale.

Effective video merchandise starts with a strong intention, followed by a thoughtful strategy that considers the entirety of your customer journey, from discovery and all the way through to conversion.

Below, we break down the most practical and impactful video merchandising tips and tricks to help you capitalise on video and stay ahead of the evolution of e-commerce.

The current value of video merchandising

To succeed in modern e-commerce, brands must offer an experience that makes customers feel confident about their purchase. Static images can only do so much, in that they really can’t compete with video marketing that can demonstrate scale, behaviour, texture, assembly, compatibility and lifestyle context. In short, video merchandising answers questions shoppers didn’t know they had, reduces uncertainty and strengthens the emotional connection between customer and product.

How to craft product videos that inspire confidence

A major benefit of today’s content landscape is that high-impact video is more accessible than ever. Production no longer requires large budgets or specialist crews. For instance, you can use an AI video editor like Adobe Premiere Pro to streamline your video production process, enabling teams to create polished content faster and with fewer technical barriers. This shift to autonomous editing allows businesses of all sizes, from boutique online stores to enterprise-level retailers alike, to produce professional-quality videos that fit seamlessly into product pages, landing pages, ads and email campaigns.

Here are just a few ways you can integrate video merchandising into your e-commerce platforms and across other components of your brand’s digital marketing efforts.

Use your product videos as an advertisement

Product videos are informative, but they’re also a great way to advertise your product on the product page. Like all advertisements, a compelling product video communicates a promise. The goal is to help customers imagine the product in their daily life, understand its value and trust its quality.

A clear storyline helps to achieve this. For example, the narrative might take the viewer from a product unboxing to real-world use, or it might focus on a problem-solution framework that highlights the customer’s pain points and how your product resolves them.

Visual clarity is key here. Make sure your shots showcase details that matter, whether it’s the quality of stitching used to produce a garment, the stability of a piece of furniture from its construction, the shine of A-grade leather, or the attention to detail in a user interface for tech offerings.

Movement should also feel purposeful rather than flashy – think gliding pans, slow zooms or real-time demonstrations make the product feel tangible. Even if filmed simply, well-executed footage gives the viewer a richer understanding than a still image ever could.

Consider lighting and setting to showcase products

Lighting and environment also influence the perception of your products significantly. Clean, consistent lighting helps the viewer focus on the product rather than distractions. Your backdrop should align with your brand identity, so when shooting, keep your studio uncluttered and minimal to convey quality and reliability.

Or if you’re going from emotion and relatively, go for lifestyle settings by shooting out in the wild, while curating what you can. Both approaches can work here. The key is simply to match the style to your brand values and your shopper’s expectations.

Integrate storytelling into your video merchandising

In video merchandising, you want to try to create a narrative that guides the viewer thoughtfully from introduction to decision. When customers understand what a product does and why it matters, they feel more connected to the brand and more comfortable proceeding to checkout.

Consider how your customers use your product in the real world. Craft short story arcs that highlight those moments. For instance, a kitchen appliance brand might show a family preparing a meal together, emphasising simplicity and reliability. A fitness brand might display the transformation a user feels as they incorporate a piece of equipment into their routine. These scenarios allow customers to see themselves in the story, making the product feel essential rather than optional.

Authenticity adds power to storytelling. Including user-generated clips, testimonials or behind-the-scenes glimpses can reinforce trust. These elements remind viewers they’re dealing with a genuine brand with a real community behind it. Even larger enterprises benefit from humanising their content and allowing a sense of transparency to shine through.

Using sound, voice and music to drive engagement

Sound design is an overlooked but super valuable component of e-commerce video merchandising. Music sets the tone and emotional pace, while voiceovers provide clarity and structure. A thoughtful soundscape helps viewers understand what they’re seeing and builds a sense of professionalism.

Voiceovers, in particular, are incredibly effective for product explainers, demonstrations and troubleshooting videos. They allow you to guide the viewer step-by-step, highlight key product advantages and reinforce brand messaging. Brands that want to scale voiceover production across hundreds of SKUs or frequent campaign updates can now learn how to create voiceovers using AI, enabling consistent tone, fast turnaround and full customisation without relying on external voice talent.

Music selection should reflect your audience’s preferences. Upbeat tracks work well for lifestyle product launches or youth-oriented brands, while calm, minimal soundtracks suit premium or technical products. Regardless of style, the audio should never overpower the visuals or narration. Subtlety and balance make the viewing experience feel more refined and intentional.

Transparency as a Way to Reduce Returns

One last, but absolutely not least, advantage of strong video merchandising is its power to reduce customer order returns. Many e-commerce returns stem from mismatched expectations rather than actual product flaws. When shoppers misunderstand dimensions, colours or functionality, dissatisfaction occurs, and the brand bears the cost.

Video helps bridge this gap by presenting products in a realistic and holistic way. Demonstrating scale with people or common household objects provides context. Showing the product under different lighting is a great way of being as transparent as possible and helping depict true colours. Displaying assembly steps or setup processes reassures customers that the product is manageable and user-friendly. When viewers can clearly see the product in action, they buy with confidence and keep the item once it arrives.

The final cut: harness the power of video merchandising for your e-commerce brand

Video merchandising has become a core part of selling your products online. It's one of the easiest ways to enhance storytelling, clarify product value, lift conversions and strengthen brand identity across every digital touchpoint.

By embracing accessible tools like AI-driven editors, refining your narratives, crafting appealing settings with good lighting and sound and being as transparent as possible, you can turn video from an optional add-on into one of your most influential sales assets.

Ultimately, the e-commerce brands that master this approach earn their consumer confidence and loyalty by creating a richer shopping experience that leaves an impression to remember in an increasingly crowded marketplace.

If you own a business, you’ve probably had at least one late night where you stare at an empty LinkedIn template or a half-finished post and wonder why making something “easy” feels so impossible. You may have wanted to whip up a flyer for an event the next day, or you needed a graphic for Facebook right this minute but lost an hour arguing with colours, fonts or layouts that just don’t look quite “right”.

And let’s be honest, not every business owner has a design team at their fingertips. Most days, it’s just you, your laptop, and a to-do list that doesn’t care how wiped out you are. When branding, marketing, and content creation become one more job on top of a laundry list of others, even the best intentions can fall through the cracks.

That’s why this list exists. Below, we’ve rounded up the ten design apps that actually make life easier. We’ll cover what each app excels at, who each one is best suited for, and how they can help you create on-brand designs without losing another evening staring at a blank screen.

1. Adobe Express

Adobe Express is one of the few design tools that allow busy business owners to generate AI images and high-quality marketing graphics all in one place, without any actual design experience. It has all the usual bells and whistles of the Adobe suite, with well-designed templates, intuitive drag-and-drop editing and brand kits that will keep your colours, fonts, and logos consistent on every post, flyer, or ad that you create.

But what makes it extra useful for small businesses is the Firefly technology working behind the scenes. Create custom visuals instantly, remove backgrounds, swap elements, or re-style images in a few clicks, with commercial-safe results you can use in your branding with confidence. For owners already juggling a hundred other tasks, Adobe Express makes design a quick, reliable process instead of a frustrating time sink.

2. Canva

Canva has become the most popular design app among business owners for good reason: it’s fast, intuitive, and you get professional-looking designs without having to navigate any intimidating tools.

With an expansive library of templates, it’s easy to whip up everything from Instagram graphics to menus, brochures, and POS assets, making it particularly popular among anyone working in retail design. Need signage, product tags, or seasonal campaign graphics and promotional posters? Canva has a layout you can customise in minutes.

Beyond the templates, the real magic of Canva lies in its approachability. You can also upload your brand colours, fonts, and logo so every piece of content has a consistent look, whether you’re designing for social media, your website, or an in-store display.

3. Figma

If you’ve ever tried to put together a social media post or page and had every designer in your company send you their “final draft”, then you know how frustrating design software can be. With Figma, every team member can work on the same file at the same time, and they can give real-time feedback, track changes and add comments without leaving a mess of multiple drafts.

As a business owner, this is where Figma starts to shine. If you need to prototype a landing page or a newsletter, redesign a logo, or just create a new set of social graphics, your team can watch you do it in real-time.

Even if you’re not a professional designer, Figma offers tons of templates, components and a drag-and-drop UI that will make you look like one, without leaving you lost for hours and hours. Figma can also scale to fit the size of your team, from a one-person show to a small internal creative agency.

4. Visme

Business often involves relaying concepts, plans and ideas to clients, customers, investors or even your team, and sometimes sitting through another presentation with boring slides or static charts and graphs can seem more like a punishment than a necessity.

Visme is a tool that makes it look easy. Whether you’re turning data into a story, creating a colourful chart, spinning a map into a captivating diagram, or even building an animated infographic, it’s easy to make slides that don’t look like slides.

Visme can also set itself apart with the way it enables good communication. Whether it’s displaying product statistics, explaining a process or presenting a marketing report, it’s designed to do just that (and do it with a visual flair that will grab anyone’s attention).

While many business owners would love to make their own slides, take a long look at their schedule and they’ll realise there’s no way to make the time. With Visme, you can log on from any location, put together compelling visual communication in minutes, and then move on with your day.

5. Desygner

Busy business owners rarely have the time to design graphics, flyers or emails, but sometimes you just need to get something out there, like an email newsletter or a flyer for a sale or promotion, and waiting until you have a weekend to spare just won’t cut it. Desygner makes it easy to get fast, efficient and (bonus) beautiful design, thanks to a fast, intuitive software that keeps your branding consistent with no extra work. Upload your logo, colours, fonts, and then start building your designs knowing that Desygner is automatically going to keep your style consistent from graphic to graphic.

Desygner can also separate itself with its speed and control. From choosing a template or starting from scratch, you can edit your elements in seconds, and then share them to social media, download them for print, or export them to your CMS without ever leaving the app.

It’s the feeling of having a small design team always on call, whenever the inspiration or need for new content arrives. For small business owners, it’s not just about time-saving but about the peace of mind in knowing that every post, flyer or banner will look good, even without touching design software.

6. PicMonkey

PicMonkey is a business owner’s best friend when it comes to making social media visuals that stand out without spending hours doing design work. Whether you’re sharing product updates, promotional graphics, or behind-the-scenes snapshots, PicMonkey allows you to quickly and easily create polished, eye-catching content. The drag-and-drop editor, layer-based image editing, and customizable templates empower even non-designers to produce professional-looking visuals.

What makes PicMonkey even more helpful is how you can use it to leverage different social media platforms. Resize your graphics for Instagram, Facebook, Pinterest, or LinkedIn with a few clicks to ensure that every post is ready for that channel. Sprinkle in branded elements, text overlays, or simple effects and your content can easily maintain a consistent style while being optimised for each social network.

7. Crello (Now VistaCreate)

VistaCreate (previously known as Crello) is ideal for entrepreneurs and business owners who want their images to move (quite literally). It is a template-based design tool that is entirely motion graphics and dynamic social content-oriented. From animated social posts, video clips, GIFs, and on-screen alerts to super-trendy eye-catching ads and animations that pop off your feed, VistaCreate has it all.

If you are a small business owner competing for eyeballs and attention online, VistaCreate makes the video animation process straightforward and a bit more exciting than you thought it could be. It also offers the best of both worlds: creativity and convenience. You don’t need an art background to create something that looks slick: drag-and-drop design templates, ready-made animations, and one-tap editing tools allow you to churn out high-quality designs in minutes.

Whether you need to create a quick promo video, a carousel for Instagram, or a branded social image, VistaCreate provides you with everything you need to tinker, revise, and bring your content to life (while staying on-brand and on-message).

8. Snappa

Snappa is a graphic design tool created for entrepreneurs and business owners that makes it easy to create professional graphics quickly and without hassle. It’s best used when you need to create graphics for ads, banners or online marketing campaigns and you actually want them to stand out. The platform offers a library of pre-made templates, intuitive editing tools, and a large collection of stock images that make it easy to create professional-grade graphics in a few minutes (no design degree required).

The main benefit of Snappa is for social media marketing. The ability to easily resize a design to work on multiple platforms, optimise your visuals for social engagement, and create your campaign assets so that they are cohesive across Facebook, Instagram, LinkedIn or Twitter is a huge help. For an entrepreneur who is typically wearing 12 different hats, Snappa allows them to plan, produce and publish their social media or marketing graphics without being stuck inside design software for hours on end.

9. Sketch

Sketch is a popular desktop application for macOS users who want a powerful, design-focused workspace without all the cruft. For business owners who also do hands-on web or app design work, it’s a great tool for whipping up interfaces, mockups, or other detailed digital assets.

It’s not quite an all-in-one design/prototyping suite like Figma, giving you the precise level of control and fine-tuning that lets you customise every element just the way you want it, which is helpful when building a brand with clean, professional design components.

But where Sketch really shines is in its surrounding ecosystem. Plugins, integrations, and shared libraries help even small teams work effectively and with consistent design standards across websites, apps, or marketing materials. For Mac users, Sketch gives the flexibility to get hands-on with design and feel like a professional without having a full design team at your disposal.

10. Gravit Designer

Gravit Designer is a free, cross-platform vector design app that’s feature-rich enough for business owners to create professional graphics but intuitive enough that you won’t get stuck in a time-consuming or expensive learning curve. Whether you’re designing logos, icons, illustrations, or custom social media graphics, it’s highly flexible enough to let you bring your ideas to life from the ground up.

One big advantage here is accessibility, since you can use it on any platform via browser or desktop app. For a small business that needs design flexibility but is on a tight budget, Gravit Designer offers a surprisingly full suite of features that won’t overwhelm beginners but will let you experiment, iterate, and produce polished visuals. It’s a great tool for business owners who want to create unique, scalable graphics that can evolve with their brand.

How to Choose the Right Design App for Your Business

It’s easy to get caught up in the bells and whistles of a design tool, but most importantly, it should work well for your business — that means if you’re working solo, you might prefer an app that allows for real-time collaboration with team members down the road. If you’re handling several clients, you’ll want to find an app that syncs with other tools you use, like your social scheduler, email app and/or file-sharing solution.

It’s also a good idea to think about how long it will take to learn the app, if at all. Some design apps are extremely simple and can be used without any prior knowledge, so you can get up and running in a matter of minutes. Other, more complex apps may require some practice to get the hang of, but you will be rewarded with precision and customisation down the road. Design speed may not seem important to some, but for many solopreneurs, it can save hours each week if you can accomplish a task in your preferred app with little to no frustration.

If you know the work you typically design for your business (social graphics, print materials, infographics, product mockups), start with apps that can help streamline the most common tasks. Ideally, the app you choose to use should feel like it’s working for you and your business, and not against you.

Turning Ideas Into On-Brand Visuals

The best design tool is the one that you’ll use. If you want to use design software to gain confidence and inspiration to make your own on-brand graphics, we’ve shown you a bunch of apps and websites to get you there. From social graphics to marketing material and other small graphics you need for your website, these tools are easy enough to use so that you won’t need to wait for or rely on a professional designer.

And for you, small business owners out there, that means you have an easier time of clearly and consistently communicating your brand in a way that’s truly your own, without getting sucked into complicated programs or spending your money on services.

The retail landscape in India is now transforming like never before. The way people pay for things, whether it’s a couch, sweater, or candy bar on the corner, has moved from cash and checks, to debit and credit cards, to digitalized mobile phones. Strong digital infrastructure, a high penetration of smartphones, and government-backed moves such as Digital India have paved the way for a payment revolution in the country.

Today, online transactions are a way of life. India, from small kirana stores to large retail chains, is accepting smarter, faster, and safer payments. According to the National Payments Corporation of India (NPCI), over 100 billion UPI transactions were recorded in 2024, a number that reflects how India has truly gone digital. Let’s explore the five payment innovations that are reshaping Indian retail right now.

India’s Retail Payments Go Real-time

India’s retail payments are rapidly shifting to real-time and mobile-first, as UPI, tap-to-pay, BNPL, wallets, and AI-led authentication reshape how consumers pay across kirana stores and large chains alike. Strong digital infrastructure, widespread smartphones, and policy support have pushed online transactions into daily life, with UPI enabling instant, low-friction payments, NFC cutting checkout times, BNPL lifting conversion and ticket size, super apps unifying commerce and financial services, and AI, biometrics, and voice interfaces expanding secure, inclusive access for both urban and rural shoppers.

1. UPI 2.0 and UPI Lite: The Backbone of India’s Cashless Growth

UPI (that is, Unified Payments Interface) lies at the heart of India’s digital payment success. Not only has it made transactions easier, but they’re instant, free and incredibly safe. Whether you’re buying a coffee, hailing a taxi, or making an online purchase, UPI is now the preferred way to pay. The UPI 2.0 had version had features like Overdraft facility and signed intent and invoice in the system of GST, which had made it even more business-friendly. Retailers now deploy it in use cases from fast checkouts to inventory management.

UPI Lite, introduced to enable small-value offline payments, is helping India’s smaller towns and rural areas go cashless. Even without internet connectivity, people can make payments of up to Rs 500, making it a reliable option for kirana stores, street vendors, and rural retailers. Apps like Paytm, PhonePe, Google Pay, and BHIM have taken UPI to the masses. These apps are now deeply integrated into retail ecosystems, from malls to roadside stalls, ensuring convenience for both sellers and buyers.

2. Tap-to-Pay and NFC: Redefining Speed at the Checkout Counter

Speed and convenience are key in today’s fast-moving retail world. Tap-to-pay and NFC (Near Field Communication) payments are making this possible. By simply tapping a card or smartphone on a POS machine, payments are completed within seconds, with no PIN no delay. Major banks in India have rolled out NFC-enabled debit and credit cards. Retailers are upgrading their POS systems to accept tap payments. The result is shorter queues, faster billing, and a smoother shopping experience.

Big brands like Reliance Retail, Big Bazaar, and Starbucks India have already adopted contactless payment systems. Even small businesses are catching up, especially after the pandemic highlighted the importance of touch-free transactions. Beyond speed, NFC payments also bring better security. Each transaction generates a unique code, reducing fraud risks. This combination of safety and convenience is helping retailers build customer trust and loyalty.

3. BNPL (Buy Now, Pay Later): India’s New Age Credit Revolution

The concept of “Buy Now, Pay Later” has gained massive traction among Indian consumers. BNPL allows customers to purchase products immediately and pay for them in easy installments, often without interest. This innovation has changed how people shop, especially young professionals and online buyers. BNPL options are available across e-commerce platforms, fashion brands, and even offline stores.

Leading players such as Simpl, ZestMoney, LazyPay, and Amazon Pay Later have made it easy to access short-term credit without traditional paperwork or bank approvals. For retailers, BNPL drives higher sales and improves customer retention. Shoppers are more likely to buy when flexible payment options are available. According to recent market reports, BNPL transactions in India are expected to grow by over 40 percent annually in the next few years. The Reserve Bank of India (RBI) is also monitoring the sector closely to ensure responsible credit practices. With regulation and innovation working hand in hand, BNPL is set to remain a key player in India’s retail payment future.

4. Digital Wallets and Super Apps: One App for Every Payment Need

Digital wallets have evolved far beyond simple money transfer tools. They have now become super apps, multifunctional platforms that combine payments, shopping, insurance, travel, and more in one place.

Apps like Paytm, PhonePe, Amazon Pay, and Google Pay are leading this transformation. They not only enable instant payments but also offer rewards, cashback programs, and financial services. Many of these platforms have built merchant tools that allow even small retailers to manage payments, invoices, and loyalty programs digitally. For consumers, this integration means convenience and control. They can book tickets, pay bills, or shop online, all within a single app. For businesses, it means access to a larger audience, faster settlements, and better data insights. The success of these super apps lies in their ecosystem approach, creating an all-in-one digital lifestyle that blends finance, commerce, and entertainment seamlessly.

5. AI, Biometrics, and Voice Payments: The Future is Already Here

The next wave of payment innovation in India is being powered by artificial intelligence and biometrics. These technologies are improving both security and accessibility. AI helps detect fraud in real time by identifying unusual spending patterns. Retailers using AI-powered payment systems can reduce chargebacks and enhance customer trust. Biometrics, such as fingerprint and facial recognition, are being used for authentication, making transactions faster and safer.

Voice payments are another emerging trend, especially for India’s rural and semi-literate population. Initiatives like RBI’s and NPCI’s voice-based UPI pilot are allowing users to make payments through simple voice commands in regional languages. This is helping bridge the digital divide and bringing millions into the formal financial system. These futuristic technologies are not just trends; they are tools for inclusion and empowerment. With AI, biometrics, and voice technology, India is proving that digital innovation can be human-centric too.

How These Innovations Are Transforming Retail Businesses

Digital payment systems enable growth for retailers. Transactions become more than just conversion. Payment systems provide businesses with real-time and streamlined more efficient data processing. Businesses understand consumer behaviour, optimize cash flow, and deploy targeted promotions. Digital payments also promote transparency, reduce cash dependency, and enhance customer trust. Quick settlement and simplified record keeping increase time efficiency for small retailers.

Large retail chains enjoy improved turnover and operational time efficiency. Government initiatives such as Digital India, PMGDISHA, and Jan Dhan Yojana improve financial literacy and drive digital payment use in India. In unison, these initiatives assist retailers and consumers to a cashless and more connected economy.

The Road Ahead

The evolution of a completely cashless economy in India is commendable. Innovation is making fast and integrated retail driven by UPI, BNPL, and AI-enabled payments. The combination of ease, safety, and inclusivity is what gives India a competitive advantage in the world. In the future, as technology continues to evolve and become ubiquitous, the distance between physical and digital retailing will continue to close. Early adopting retailers will have a competitive advantage in customer acquisition, engagement, and retention. The Indian retail sector of tomorrow is intelligent, integrated, and most importantly, inclusively cashless, funded by sleights of innovations and changes in India’s shopping, payment, and economic growth paradigms.

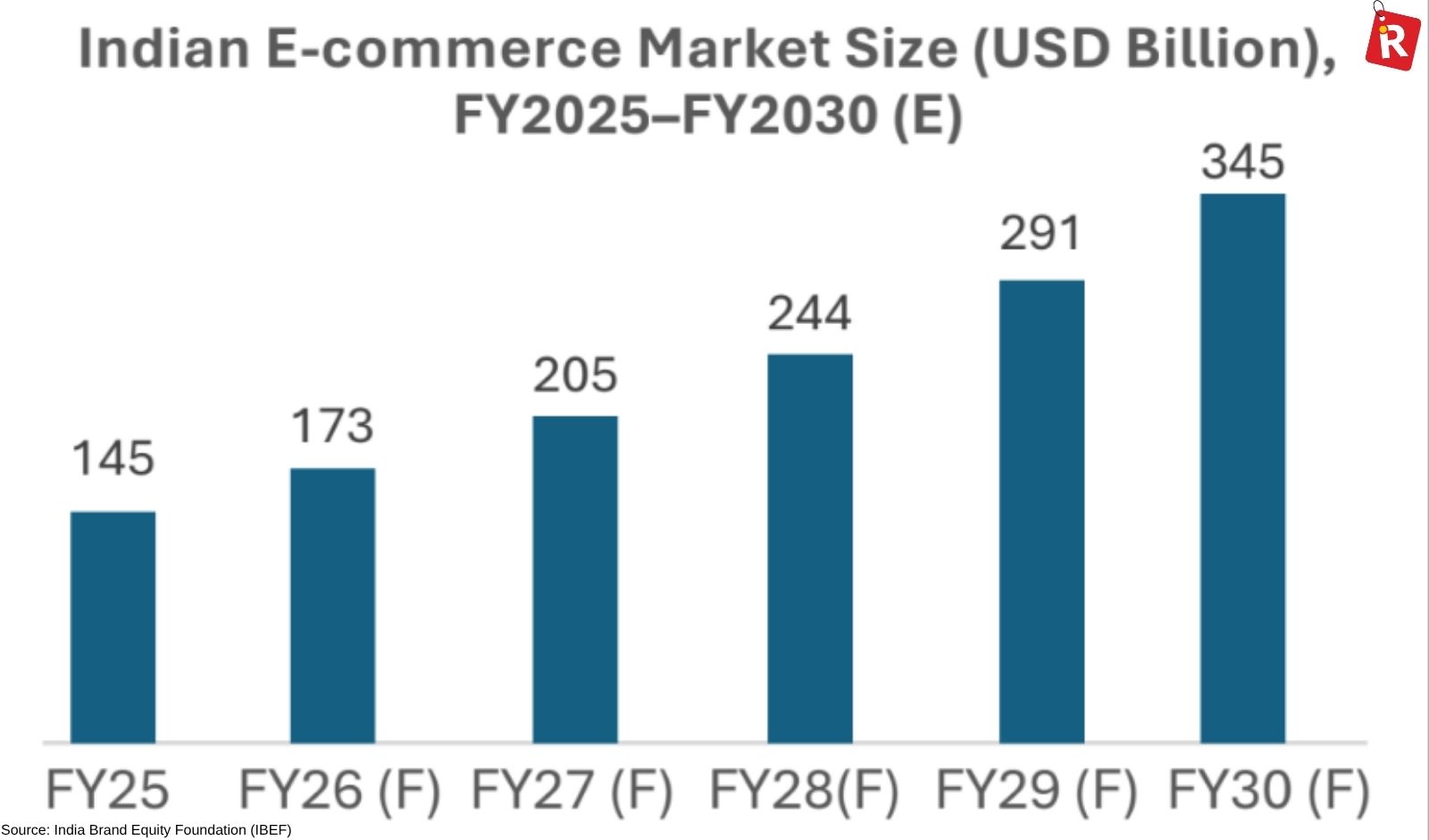

India’s e-commerce sector is entering an unprecedented growth phase, set to redefine how the nation shops, consumes, and does business. The country’s e-commerce market is projected to more than double from $145 billion in FY2025 to $345 billion by FY2030, growing at a compound annual growth rate (CAGR) of 19 percent.

This surge positions India firmly as one of the world’s fastest-growing e-commerce markets, underpinned by digital innovation, investor confidence, and expanding adoption across Tier II and III cities.

A Booming Retail Landscape

As of 2024, India has become the world’s third-largest retail market, with e-commerce contributing between 7 to 9 percent of total retail sales. The Gross Merchandise Value (GMV) of India’s e-commerce industry reached $14 billion in 2025, demonstrating how rapidly online channels have become central to domestic consumption, according to a new report by Rubix Data Sciences.

Segments like beauty and personal care, fashion, and fast-moving consumer goods (FMCG) are emerging as the fastest-growing verticals. Beauty and personal care alone are expected to expand at a 30–35 percent CAGR through 2030, while fashion and FMCG are each projected to grow by 27–30 percent.

Crucially, India’s smaller cities are powering this evolution. Tier II and III centers now represent over 56 percent of online shoppers and 60 percent of new e-commerce users, signaling a decisive shift in the country’s consumption geography. Improved logistics, increased internet penetration, and the normalization of digital payments post-GST reform have brought online retail to the country’s deepest pockets.

Investment Momentum Returns

The report highlights a strong rebound in investment activity, reflecting sustained confidence in India’s digital economy. Private equity and venture capital investments in e-commerce grew by 87 percent year-on-year in 2024, reaching $4.6 billion across 118 deals. E-commerce now commands 31 percent of total startup investment value in India, underscoring its strategic weight within the broader entrepreneurial ecosystem.

Investor optimism is being driven by the sector’s digital transformation potential and its increasing alignment with India’s long-term consumption growth story. From omnichannel retail models to AI-enabled supply chains, startups and established players alike are reimagining e-commerce through innovation and data intelligence.

Digital Payments Fueling Growth

The foundation of India’s e-commerce boom lies in its digital payments revolution. By the end of FY2025, the country had over 1 billion internet subscribers, while Unified Payments Interface (UPI) transactions accounted for Rs 261 trillion, representing 85 percent of India’s total digital payment volume.

The seamless integration of UPI across platforms has democratized online commerce, removing barriers to entry for millions of first-time digital shoppers. It has also paved the way for quick commerce, one of the most dynamic sub-segments in India’s retail landscape.

Quick commerce registered a Gross Order Value (GOV) of Rs 640 billion in FY2025 and is forecast to hit Rs 2 trillion by FY2028, fueled by consumer demand for instant gratification and hyper-local delivery networks. While early years were characterized by aggressive customer acquisition, leading platforms are now pivoting toward sustainable profitability, optimizing last-mile logistics, and building multiple revenue streams through subscription models, advertising, and private labels.

Government Initiatives and Policy Reforms

The government’s proactive role continues to be a key enabler of e-commerce expansion. The Government e-Marketplace (GeM)—a digital procurement platform—has achieved a cumulative GMV of Rs 15 trillion, growing at a remarkable 72 percent CAGR since FY2022.

In addition, the government is exploring policy shifts to relax foreign direct investment (FDI) norms, potentially allowing e-commerce platforms to directly facilitate exports of Indian goods. Such reforms could turn India into a global e-commerce export hub, bolstering its resilience amid global trade uncertainties and tariff headwinds from the U.S. and other economies.

This forward-looking policy stance, coupled with the government’s plan to source price data from e-commerce giants like Amazon and Flipkart to improve inflation indices such as the Consumer Price Index (CPI), signals a growing recognition of online retail’s macroeconomic significance.

Challenges and the Road Ahead

Despite strong tailwinds, the sector faces structural challenges. High return rates averaging 17 percent continue to erode margins, leading to estimated annual losses of Rs 2 trillion. To maintain profitability, players must focus on streamlining reverse logistics, enhancing supply chain efficiencies, and leveraging AI-driven demand forecasting to reduce operational waste.

Infrastructure upgrades and last-mile delivery optimization will be essential for sustained growth, particularly as competition intensifies and consumer expectations evolve.

A New Chapter for India’s Digital Economy

According to Mohan Ramaswamy, Co-Founder and CEO of Rubix Data Sciences, India’s e-commerce story transcends mere digital adoption. “The convergence of payments, logistics, and consumer behavior is creating a powerful growth engine for the economy,” he said. “What lies ahead is not just an expansion of online retail but the emergence of a more inclusive, tech-enabled consumption ecosystem. At Rubix, our goal is to help businesses and policymakers navigate this transformation with the right intelligence and foresight.”

This convergence—between infrastructure, innovation, and inclusion—will define the next decade of India’s e-commerce evolution. As digital infrastructure deepens, investor appetite strengthens, and policy frameworks adapt, the sector is poised to become a central pillar of India’s consumption-driven growth narrative.

India’s 2025 Diwali festive season closed on a high note for the e-commerce sector, signaling the continued evolution of digital retail across the country. The order volumes during the festive period surged 24 percent year-on-year (YoY), while gross merchandise value (GMV) rose by 23 percent. The findings are drawn from over 150 million transactions processed through Unicommerce’s flagship platform, Uniware, during the 25-day festive periods of 2024 and 2025.

Tier II and III Cities Drive Festive Growth

A key highlight of this season’s performance was the growing strength of Bharat’s smaller towns. Tier II and III cities together contributed around 55 percent of total orders, underscoring the deepening digital adoption and rising purchasing power outside major metros. The data suggests that India’s e-commerce growth story is increasingly being written in non-metro markets, where improved logistics networks and digital payment adoption have made online shopping more accessible and reliable.

Regionally, Tier II cities led festive growth with a 28 percent YoY increase in orders, followed by Tier I cities and metros at 24 percent, and Tier III towns at 23 percent, according to Unicommerce. This broad-based momentum shows that festive euphoria was not confined to urban centers but extended across India, driven by aggressive discounting, improved delivery timelines, and localized marketing strategies.

Quick Commerce Emerges as the Biggest Growth Engine

Quick commerce continued its meteoric rise, emerging as the fastest-growing segment this festive season. The category recorded a massive 120 percent YoY jump in order volumes, fueled by consumer demand for instant gratification and convenience. With platforms now delivering everything from groceries and snacks to festive gifting items within minutes, consumers have increasingly turned to these services for last-minute purchases and quick replenishments during the festive rush.

Following quick commerce, brand websites witnessed a healthy 33 percent growth in order volumes, reflecting a growing trend of direct consumer engagement and the rise of D2C brands. Marketplaces, which remain the dominant sales channel, accounted for 38 percent of total purchases and grew 8 percent YoY in order volumes. Together, these trends point to a more diversified e-commerce ecosystem where brands are actively balancing marketplace presence with their own digital storefronts.

Festive Shopping Categories Reflect New Consumer Priorities

Consumer preferences this festive season painted an interesting picture of evolving lifestyles. FMCG led the pack, driven by healthy and innovative food products such as fusion sweets, dry fruit assortments, and millet-based snacks. The shift highlights consumers’ growing inclination toward healthier indulgences, even during festive celebrations.

Home décor and furniture also saw strong traction, as consumers invested in upgrading their living spaces. Meanwhile, beauty and wellness—especially makeup, skincare, and hygiene products—continued to perform robustly. Health and pharma emerged as another top-performing segment, fueled by heightened demand for supplements and preventive healthcare products, indicating that post-pandemic health consciousness remains a lasting trend.

Payments and Fulfillment Reflect Growing Consumer Confidence

On the payments front, prepaid orders grew by 26 percent, signaling stronger trust in digital transactions and payment gateways. Interestingly, Cash-on-Delivery (COD) orders also rose by 22 percent in volume and an even higher 35 percent in GMV. This indicates a shift toward higher-value COD purchases, suggesting that consumers across regions are not only comfortable transacting online but are also making more expensive festive purchases through COD—traditionally a preferred mode in smaller cities.

Adding to the sector’s robust performance, Shipway reported faster deliveries this year. Average shipping times during the 2025 festive season were 15 percent shorter compared to last year, reflecting improved supply chain readiness and operational agility. Retailers and logistics partners have increasingly leveraged predictive analytics, advanced demand forecasting, and hyperlocal delivery models to ensure seamless and timely fulfillment, even amid record festive demand.

A Strong Foundation for Future Growth

The 2025 festive season results reinforce the resilience and adaptability of India’s e-commerce ecosystem. With growing participation from Tier II and III cities, accelerating quick commerce adoption, and enhanced logistics efficiency, the industry is set for another year of sustained expansion.

As data suggests, the festive surge this year was not just about higher order volumes—it was a reflection of India’s digital maturity, where consumers across the country are embracing convenience, reliability, and personalization at unprecedented levels.

Shopping in India has changed completely. From crowded malls to scrolling through mobile screens, buying has become faster and easier. Today, social media is the new marketplace. Indian retailers are using platforms like Instagram, Facebook, WhatsApp, and YouTube to connect directly with shoppers. The rise of social commerce has made it possible to discover, interact, and buy, all in one place.

According to industry reports, India’s social commerce market is expected to cross Rs 80,000 crore by 2025, growing at a rate of nearly 60 percent every year. From beauty and fashion to electronics and decor, every category is seeing success through social selling. Here are the top 10 social commerce tactics Indian retailers use to drive instant sales.

1. Influencer-Led Live Shopping Events

Influencers have become the face of modern retail. Many Indian brands are now hosting live shopping events with influencers who showcase products, answer questions, and offer limited-time discounts.

Platforms like Myntra, Nykaa, and Meesho use this strategy to attract thousands of live viewers. The combination of real-time interaction and trusted recommendations makes customers feel confident to buy instantly. These live sessions bring entertainment, engagement, and shopping together—something traditional ads cannot achieve.

2. Shoppable Posts and Stories on Instagram and Facebook

Social media platforms have made shopping as simple as a tap. Retailers create shoppable posts and reels where each product is tagged and linked directly to checkout pages.

Brands like Lifestyle, H&M India, and Zara use Instagram reels with “Shop Now” buttons to convert casual scrollers into buyers. The visual storytelling format inspires instant purchases because customers can see exactly how a product looks and fits in real life.

3. User-Generated Content (UGC) as Social Proof

Nothing builds trust like real people using real products. Retailers encourage customers to share photos, reviews, and short videos of their purchases. This authentic content becomes powerful social proof.

Nykaa, for instance, often reposts customer videos, and Meesho highlights shoppers who style their products creatively. Seeing others enjoy a brand increases confidence and reduces hesitation among new buyers. In India, where personal recommendations matter deeply, UGC is becoming one of the most reliable ways to drive instant conversions.

4. Exclusive Flash Sales on Social Channels

Urgency is a strong sales driver. Retailers are creating social media-exclusive flash sales, special deals or collections that are available only for followers.

Tanishq has experimented with limited WhatsApp jewelry previews, while Zudio announces surprise sales on Instagram Stories. This “first come, first served” excitement makes customers keep checking brand pages regularly, leading to higher engagement and quick purchases.

5. WhatsApp Commerce and Personalized Chat Selling

WhatsApp has become a serious sales channel for Indian retailers. Brands use WhatsApp Business accounts and chatbots to send product catalogs, answer customer questions, and finalize sales in real-time.

JioMart allows customers to order groceries directly via WhatsApp chat. FabIndia also uses it for personalized product recommendations and order tracking. This one-to-one communication makes the buying experience feel personal, quick, and trustworthy, especially for customers in smaller towns who prefer chatting over browsing websites.

6. Micro-Influencer Partnerships for Local Reach

While big influencers bring fame, micro-influencers bring trust. Many Indian retailers now collaborate with regional or niche influencers who have smaller but highly engaged audiences.

D2C brands in fashion, skincare, and wellness, like Plum and The Man Company, work with influencers who speak regional languages and create relatable content. This hyper-local approach builds strong connections and makes products feel more accessible. Micro-influencers are affordable, genuine, and perfect for spreading awareness in Tier ll and Tier lll cities.

7. AR Filters and Virtual Try-On Experiences

Augmented Reality (AR) is changing how customers shop. Brands are using AR filters to let users “try on” products virtually before buying.

Lenskart’s 3D try-on feature helps shoppers see how glasses look on their faces. Nykaa’s “Try It On” filter allows makeup lovers to test shades virtually. These experiences make online shopping more interactive and reduce product returns, as customers get a clearer idea before purchasing.

8. Short-Form Video Commerce

Short videos have become one of the most powerful social commerce tools. Platforms like Instagram Reels, YouTube Shorts, and even Flipkart Video are helping retailers tell quick stories that drive impulse buys.

Brands use these 15–30 second clips to highlight product benefits, styling tips, or real-time results. Amazon MiniTV and Meesho’s short video sections are perfect examples of this trend. Short videos capture attention fast and deliver information in a format that audiences love.

9. Social Referral and Reward Programs

Word of mouth has gone digital. Indian retailers are rewarding customers for tagging friends, sharing products, or posting about their purchases.

Meesho’s referral model is one of the best-known examples. It allows users to earn commission or discounts when someone buys through their shared link. Similarly, The Souled Store runs loyalty programs where social engagement leads to redeemable rewards. These tactics turn happy customers into active brand promoters.

10. Social Listening and Trend-Based Campaigns

Retailers are now using data and analytics to listen to what their audience is saying online. By tracking trending topics, memes, and customer feedback, they quickly adapt their marketing to match what’s popular.

Brands like Bewakoof and Tata CLiQ have mastered this art. They launch meme-inspired campaigns and products that connect instantly with social media users. This real-time marketing makes their content feel fresh, fun, and shareable.

Data, AI, and the Science Behind Social Commerce

Behind every viral post or campaign lies smart data. Retailers analyze engagement rates, hashtag trends, and customer sentiment to plan better strategies. AI tools are now helping brands predict what products will sell, when to launch offers, and how to personalize recommendations.

Chatbots handle instant replies while machine learning tracks buying patterns. Together, these tools ensure that every click leads to potential conversion.

The Indian Social Commerce Market at a Glance

India’s social commerce space is expanding rapidly:

- Expected market size: $70 billion by 2030

- Over 250 million shoppers will buy through social platforms by 2026

- 60 percent of sales come from Tier ll and Tier lll cities

This growth is fueled by affordable data, increasing smartphone use, and trust in digital payments. The blend of entertainment and shopping fits perfectly with how Indian consumers spend time online.

From Likes to Loyal Buyers

Social commerce in India is not a passing trend; it’s a movement that’s redefining retail. Shoppers no longer want to browse static websites. They want connection, conversation, and confidence before buying. Retailers who use social commerce smartly can build strong relationships and drive instant sales. The key lies in mixing creativity with technology, through influencers, data, and personalized interactions. In the next few years, almost every successful retailer in India will be a social-first brand. The question is, is your brand ready to turn likes into loyal buyers?

Finding wireless earbuds with active noise cancellation (ANC) no longer has to be expensive. Today, several brands offer earbuds that block outside noise and deliver clear, high-quality sound. These earbuds are designed to be comfortable, even during long hours of use. Users can enjoy music, podcasts, or calls without distractions from traffic, chatter, or household noise. They are suitable for a wide range of activities. People who commute daily can focus on music or calls while traveling. Those who work from home can stay productive without background noise interfering. Fitness enthusiasts can use them during workouts or runs, thanks to lightweight designs and water resistance in many models. Even casual listeners can enjoy quiet, immersive sound while relaxing at home.

Many budget-friendly ANC earbuds now come with additional features such as touch controls, fast charging, and stable Bluetooth connectivity. With so many options available, everyone can find a pair that fits their lifestyle and needs. Here is a list of seven wireless earbuds with ANC that combine good performance, comfort, and affordability, offering a noise-free listening experience without a heavy investment.

Why Active Noise Cancellation Matters

ANC is a technology that reduces unwanted background noise. Imagine sitting on a noisy train or working in a busy cafe—ANC earbuds let you focus on music, calls, or podcasts without distraction. Traditionally, this feature was found in premium models only. But today, even budget earbuds can give you a satisfying noise-free experience. When buying ANC earbuds on a budget, keep an eye on these features:

- Battery Life: Look for earbuds that last at least 20–30 hours, including the charging case.

- Sound Quality: Clear vocals, decent bass, and balanced sound make a big difference.

- Comfort and Fit: Earbuds that sit well in your ears are essential for long usage.

- Connectivity: Stable Bluetooth 5.0 or higher ensures smooth pairing with devices.

- Water or Sweat Resistance: Handy for workouts or outdoor use.

Find 7 Best Budget ANC Wireless Earbuds

Affordable ANC earbuds offering clear sound, comfort, and noise cancellation, perfect for commuting, workouts, or everyday music listening

1. OnePlus Buds Z2

The OnePlus Buds Z2 are not just about technical specs, they deliver a premium listening experience at an affordable price. The earbuds have a natural, balanced sound profile that suits most genres, from soft acoustic to bass-heavy tracks. They sit snugly in the ears, making long listening sessions comfortable without any irritation. The touch controls are intuitive, allowing easy playback, volume adjustment, and voice assistant access. Pairing with smartphones is seamless, with quick auto-connect features that reduce setup time. Additionally, the earbuds maintain a stable connection even in crowded areas. Overall, they are perfect for daily commuters or home listeners who want quality sound, noise-free calls, and a hassle-free wireless experience.

- Price: Around Rs 4,500

- Key Features: ANC, 38 hours battery life, IP55 rating

- Why It’s Great: OnePlus Buds Z2 offers balanced sound and effective noise cancellation. The fit is comfortable, and it works well for calls and music alike.

- Unique Feature: Dolby Atmos support enhances audio depth.

2. Realme Buds Air 3