Sustainability considerations now influence the majority of the world’s grocery shoppers, particularly when buying packaged foods such as potato chips and cookies. About 67 percent of Indian consumers are more likely to purchase packaged food with sustainability claims up 11 points from 2019.

Compared globally, U.S. consumers were also more attuned to sustainability claims: 37 percent indicated they were more likely to purchase packaged food with a sustainability claim, a 6 point increase compared to 2019 results, according to a survey by Cargill. Whereas Brazil and Mexico saw 13 point increases in the purchase impact of sustainability claims between 2019 and 2021.

“Our latest findings clearly demonstrate that messages surrounding sustainability are having an impact on consumers,” said Nese Tagma, Managing Director of Strategy and Innovation, Cargill’s global edible oils business. “Insights like these help guide our consumer-focused approach to innovation, enabling us to partner with customers to co-create new products and solutions that reflect current consumer trends and ingredient preferences.”

In the case of the U.K., 51 percent of consumers now say they place a greater emphasis on sustainability, an 8 point jump in just two years.

“These insights further affirm our commitment to embed sustainable practices into every aspect of our operations,” said Florian Schattenmann, Chief Technology Officer and Vice President - Innovation and R&D, Cargill. “This includes everything from our sourcing practices to processing facilities, and even extends to new product development, where decisions to commercialize innovations now consider sustainability alongside performance and cost.”

READ MORE: Changing Consumer Trends and Shift Towards Sustainable Products

Cargill also provides sustainable solutions to meet consumer and customer needs for oils, from regenerative agriculture programs for row crop oilseeds to palm oil certified responsibly sourced by the Roundtable on Sustainable Palm Oil (RSPO).

Despite the increased awareness of sustainability among people in general, much of the plastic is still falling out of the “recycling chain”. The e-commerce industry which is heavily dependent on plastic packaging in its supply chain has a huge potential to raise sustainability standards by many points.

In fact, greater participation by private stakeholders and other members of the value chain is crucial to building a holistic, circular plastic ecosystem to reduce plastic leakage into nature, according to a case study developed in collaboration with WWF (World Wide Fund for Nature India) India and India’s top e-commerce firm Flipkart.

Mahesh Pratap Singh, Head of Sustainability and Social Responsibility, Flipkart said, “As a homegrown e-commerce organisation, the Flipkart Group is committed to building a sustainable business while playing the role of a catalyst in the creation of a thriving sustainable ecosystem. We are excited to have achieved a milestone of eliminating 100 percent single-use plastic packaging in our supply chain in a short span of time and look to aggressively work towards pushing the goal for our sellers and brand partners. We’ve also committed to sourcing from environmentally sustainable sources by working with various partners and becoming a proactive force for a better good."

Flipkart shared that its approach towards Sustainable Packaging relies on four pillars: Engage, Innovation, Capacity Building and Compliance.

Reportedly, Flipkart Group companies, including e-commerce marketplace Flipkart and leading fashion destination Myntra have eliminated 100 percent single-use plastic packaging in their own supply chain by working with several stakeholders across traceability, plastic reduction and brands and universities to name a few. It is also working towards adopting circularity in its plastics value chain in collaboration with sellers and brand partners.

E-commerce ecosystem can rely on this model and build their organization that aids in fulfilling the sustainability targets.

Varun Aggarwal, Associate Director - Sustainable Business at WWF India said, “A coordinated approach between e-commerce companies and all the other stakeholders in the plastics value chain is crucial to attaining a circular economy for plastics , Flipkart has a large secondary packaging footprint, making plastic waste management a key lever in its commitment to sustainability. The best practices adopted by Flipkart can be replicated by players in the same space to contribute to the mitigation of plastic waste”.

The study further mentions that companies need to customize interventions to influence consumer behavior and collaborate for improving and innovating the existing collection and recovery infrastructure and grow it further. Market leaders need to set up goals for their supply chain who wish to similarly engage and bring about a better plastics waste response to ultimately contribute towards a circular plastics economy and greater good of the society.

Through this case study, WWF has highlighted the need for active participation by the private stakeholders to ensure a holistic, circular plastic ecosystem to reduce plastic leakage into nature. As a leading digital platform engaging in online commerce of goods and services, Flipkart has a large secondary packaging footprint, making plastic waste management a key lever in its commitment to sustainability.

Some of the next steps identified include data-based goal setting to ensure a data-driven approach to waste management and regularly track the impact of alternatives, creating an ecosystem view of the entire waste management journey for packaging. It also includes creating a state-by-state playbook for training and working with sellers partners across different states to optimally implement the transition to sustainable packaging solutions. The best practices adopted by Flipkart can be replicated by other players in the same space for greater uptake to contribute to the mitigation of plastic waste and move towards a more circular system in e-commerce packaging.

Online shoppers in India are seeking new experiences in the age of social and video commerce and this has given digital-first brands a massive $250 billion market opportunity by 2030.

India's e-tailing gross merchandise value (GMV) reached $53 billion in 2021, demonstrating post-Covid acceleration, according to a report by Bengaluru-based market research firm RedSeer.

"Additionally, Indian e-tailing showed impressive growth (on-quarter) in 2021 while other global players struggled to maintain the momentum," the report stated.

"The current B2C retail landscape is evolving rapidly with the emergence of new consumer behaviours and expectations. The rise of new retail channels, particularly video and social commerce, is further changing the way consumers shop and what they expect from brands, said Mrigank Gutgutia, Associate Partner, RedSeer.

As a result, digital-first brands are finding it increasingly rewarding to engage with consumers in these channels and offer them a seamless, omnichannel experience.

"The success of such brands will depend on how effectively they leverage these new retail channels and how they innovate on the digital front to offer a superior omnichannel experience," Gutgutia added.

The findings suggest that consumers opt for these new-age brands for their quality (and not only price) with significantly high repurchase willingness.

Multiple $100 million revenue technology-first brands have been created already across the categories in just the past few years, with each having a unique winning playbook and first-of-their-kind business model.

"Over the 2021-30 period, we expect many more digital-first brands to scale exponentially, supported and incubated by roll-up platforms that are building the next wave of digital-first brands for India," the report noted.

READ MORE: Unlocking E-shopping: Decrypting the Future of E-commerce

India's fast-moving consumer goods (FMCG) market has expanded 10 percent in January year-on-year from 2021.

Experts believe that this indicates that the third Covid wave buoyed consumption for daily essentials and groceries.

Even in discretionary products like televisions, refrigerators, and smartphones, leading companies said they have grown sales at a double-digit percentage pace in January despite initial hiccups, according to retail intelligence platform Bizom.

READ MORE: 4 Key FMCG Trends to Watch Out For in 2022

"We are seeing a significantly lower impact even on a month-on-month sales basis compared to earlier waves. Commodity products continue to grow sales despite an easing of prices for key products like edible oils, indicating strong consumption," said Akshay D'Souza, Chief of Growth and Insights at Mobisy Technologies, which owns Bizom.

Also, despite restrictions on store timings and mobility in certain markets, the impact on business has been the least in the third Omicron wave compared to the previous two.

Moreover, commodity and packaged foods grew 43 percent and 38 percent each while sales of home and personal care products fell.

Samsung has topped the global smartphone shipments chart in 2021 as the market grew for the first time since 2017. Total global smartphone shipments in 2021 hit 1.39 billion units — a 4 percent on-year growth — but remained below pre-pandemic levels.

The reason for lower shipments is continued disruptions caused by Covid-19 and the ongoing component shortage, according to a report by Counterpoint Research. Q4 shipments fell 6 percent on-year basis to 371 million units.

“However, China, the world’s biggest smartphone market, continued to decline due to supply-side issues caused by the ongoing component shortages, as well as demand-side issues resulting from lengthening replacement cycles,” said Harmeet Singh Walia, Senior Analyst, Counterpoint.

Experts believe that the increased demand in Latin America, North America, and India led to the recovery in the global smartphone market. Growth in the US was driven by demand for Apple’s first 5G iPhone 12 Series, which continued throughout the year. The growth in India was attributed to higher replacement rates, attractive financing, and better availability of mid-to high-tier phones.

READ MORE: India Smartphone Market Logs 169 mn Units Shipment in 2021, Highest Till Date

"The market recovery could have been even better having the component shortage did not have the impact it did in the second half. The major brands navigated the component shortages comparatively better and hence managed to grow by gaining share from long-tail brands,” Walia further added.

How Mobile Brands Are Performing?

Overall, Samsung shipped 271 million smartphones, up 6 percent from 2020. The report attributed the increase to higher demand for the mid-tier A and M Series devices. Apple registered an 18 percent on-year growth to a record 237.9 million units on the back of the iPhone 12 Series’ strong performance. Xiaomi’s global shipments grew 31 percent on-year to a record 190 million units.

Also, Oppo, including OnePlus shipments since Q3, recorded a 28 percent growth to 143.2 million. Sister brand Vivo grew 21 percent to 131.3 million units. Motorola, on the other hand, was the fastest-growing smartphone brand among the top 10 original equipment manufacturers based on global shipments.

And, for the first time, Realme entered the top five in global Android smartphone shipments, while Honor also entered the top 10 in its first year as an independent manufacturer.

The fashion and lifestyle category has turned out to be one of the top two segments for direct-to-consumer (D2C) brands that enabled BNPL as a payment method at the checkout.

The demand in fashion and lifestyle was also led by men and women in Tier-I and Tier-II cities. While men in Tier-I cities spruced up their wardrobes and spent heavily on fashion, their women counterparts upgraded their tech and electronics while also indulging in fashion and lifestyle retail therapy. In Tier-II too, men took to spending on fashion and lifestyle, besides travel, while women spent on EdTech courses and upskilling besides electronics and fashion, according to a report by Fintech platform ZestMoney.

While most of the customers (median) were in the 23-26 years group, BNPL emerged as the preferred option for people across age groups with the youngest customer being 18 years old and the oldest at 66. The number of millennial and GenZ customer base increased by 2X and 3X respectively, indicating that the BNPL segment has been driven by young cohorts in India in line with the global trend.

Also, Bangalore, Mumbai, New Delhi, Pune, Hyderabad, Chennai, Ahmedabad, Thane, Kolkata, and Jaipur emerged as the top cities witnessing demand for BNPLin 2021, while Lucknow, Kanchipuram, Vijayawada, Visakhapatnam, Guntur, Surat, Indore, Bhopal, Tiruvallur, and Coimbatore were the other top Tier-II and Tier-III cities.

Lizzie Chapman, CEO & Co-founder, ZestMoney said, ‘2021 was an intense year, with the volatility of the pandemic coupled with its impact on the consumer we serve - from pain to recovery and then rapid demand acceleration over the last two quarters. Customers continued to lap up Pay Later because it gives them the perfect flexibility to spread out costs and plan their finances better. We've doubled our user base in the last 12 months taking our total registered user base to 15 million – almost 2X growth. It's been a well-rounded growth across categories from smartphones, electronics, travel, fashion and lifestyle, and home decor emerging as the top categories on the platform.”

“We not only added the highest number of new customers and merchants but also gained market share in an ever-growing market. We saw a 300 percent YoY growth in BNPL transactions as people took to convenience and affordability in a big way. Owing to the solid consumer demand we saw last year, we now have a 50 percent market share in the Indian BNPL market and over 70 percent market share in the online ‘Pay in 3’ no-cost interest-free offering. On the back of the strong demand and our expansion plans, we are confident of hitting a $10 billion GMV run rate in the next 3 years and cementing our position as the market leader in the country.” Chapman further added.

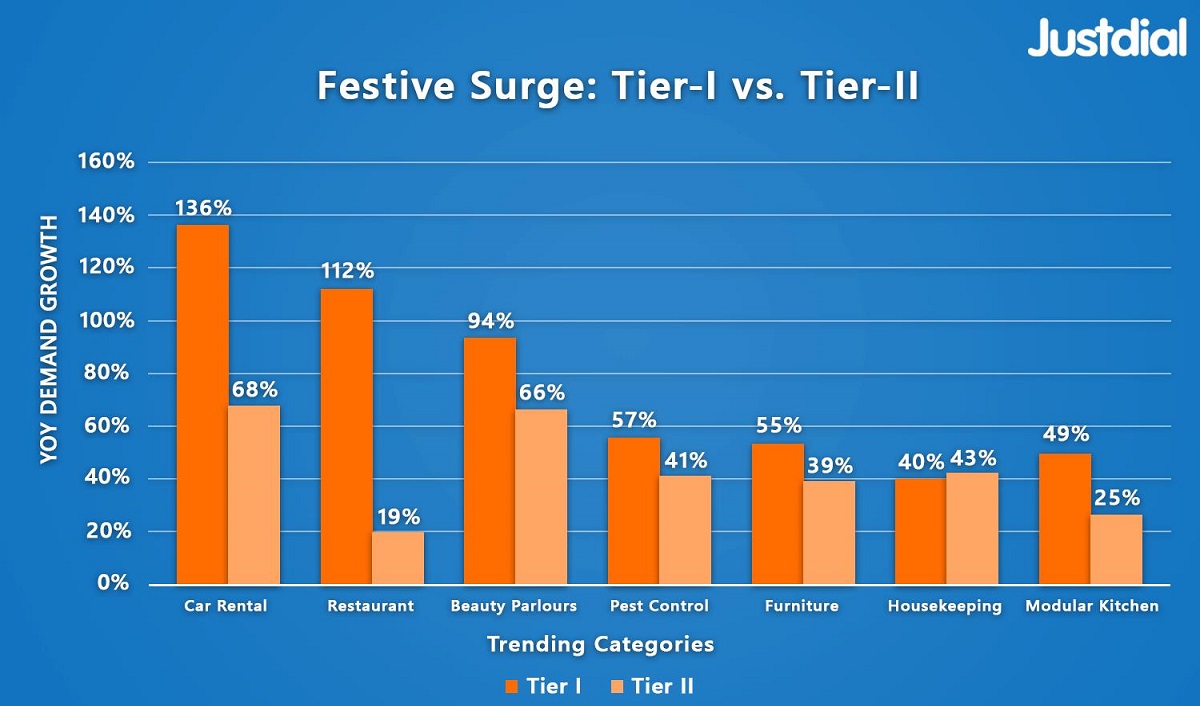

During the festive season last year, customer applications for BNPL went up by 10X with top categories being Smartphones, electronics, large appliances, fashion, furniture, and home decor. ZestMoney witnessed a 200 percent growth in transactions on Amazon, Flipkart, and Myntra compared to last year. While physical stores observed growth of 100 percent during the festive season compared to 2020.

During the festive season last year, customer applications for BNPL went up by 10X with top categories being Smartphones, electronics, large appliances, fashion, furniture, and home decor. ZestMoney witnessed a 200 percent growth in transactions on Amazon, Flipkart, and Myntra compared to last year. While physical stores observed growth of 100 percent during the festive season compared to 2020.

CMIE data shows that the average weekly index of consumer sentiments in the three weeks that ended on January 9, 16, and 23 was 59.9 and the 30-day moving average of the index of consumer sentiments as of January 23, 2022, stood at 61, higher than November 2021 when it stood at 60.3.

Consumer sentiments have improved in January by 3.9 percent after a dip in December when it fell by 4.5 percent to 57.6, though the recovery is somewhat “hesitant”.

The average weekly index of consumer sentiments in the three weeks that ended on January 9, 16, and 23 was 59.9 and the 30-day moving average of the index of consumer sentiments as of January 23, 2022, stood at 61, higher than November 2021 when it stood at 60.3, according to CMIE.

“We call the recovery seen in the early data of January as hesitant because, after that 6.9 percent increase in the week ended January 2, the weekly growth rate fell to 2.1 percent in the next week and then by 3 percent erasing much of the gains made in the preceding two weeks,” CMIE stated.

Further, while the level of the index in the latest week ended January 23 and also the 30-day moving average are impressive at 61.2 and 61 respectively, the week-to-week variations reflect some uncertainty of the January recovery, experts believe.

“The index of consumer sentiments in January is expected to cross its December level of 57.6 and could possibly cross its peak level of 60.3 reached in November,” it said, adding that the index still has a long way to go before it reaches its pre-Covid levels of around 108.

The data further showed that the index of current economic conditions went up by 6.3 percent to 58.2 and the index of consumer expectations grew by a modest 2.5 percent to 60.9.

“A faster improvement in current economic conditions with slightly higher confidence in the future as is seen in the weekly sentiments data for January 2022 is a good development. Its stride needs to be bigger and a little more confident,” CMIE added.

READ MORE: Consumer Confidence Continues To Improve, Households More Optimistic about Future

India's 'Buy Now, Pay Later' sector is expected to grow to $56 billion by FY26.

Also, India's BNPL is at an inflection point with rising e-commerce and digital P2M payments fuelling deferred payments, according to HDFC Securities.

BNPL GMV is poised to exhibit 74 percent CAGR and accounts for 5 percent of digital P2M payments by FY26E.

Experts believe the segment provides short-term financing to make immediate purchases and the credit can be paid back at a later date.

"The proliferation of BNPL as a mode of credit-based payment is gaining significant traction, particularly amongst the millennials and Gen-Z population within a short span of time," HDFC Securities stated.

According to the brokerage house, the growth of the BNPL segment is expected to be triggered on the back of rising e-commerce and digital payments penetration. "BNPL players are exploring multiple business models and are yet to establish economic viability with limited revenue drivers and high delinquencies."

READ MORE: Buy Now Pay Later: The New Financial Buzzword in Retail

Besides, the brokerage house's report cited that although 'FinTech BNPLs' enjoy favorable regulatory arbitrage, incumbents have an opportunity to expand their customer funnels either through in-house offerings or partnerships.

"We expect regulatory convergence on the back of the RBI's recent narrative for digital lenders although 'FinTech BNPLs' are likely to sustain their superior user experience," the company further added. "Within a bouquet of BNPL options, credit cards remain the most exhaustive and profitable and, in fact, offer an up-sell opportunity for credit-tested top-of-the-BNPL-pyramid customers."

Rentals of mall operators are expected to decline by 20-25 percent in Q4FY2022 as against earlier estimates due to Omicron-led third wave.

With impact on recovery in Q4FY2022, the rental recovery for FY2022 is expected to be up to 70 percent of pre-Covid levels, as compared to earlier estimates of up to 75 percent recovery, according to ICRA.

Overall, the majority of the store categories are expected to reach near-normalcy by Q1FY2023 as against earlier estimated Q4FY2022 with variance depending on the mall or brand-specific factors.

“The trading values are expected to decline to 60-70 percent of pre-Covid levels in Q4FY2022 due to the third wave as against recovery of over 85 percent in Q3FY2022. The rental recovery for Q4FY2022 is estimated to be at 70 percent of pre-Covid levels as against the earlier estimates of over 90 percent levels,” said Anupama Reddy, Sector Head - Corporate Ratings, ICRA.

The fact is that the Omicron-led third wave of the Covid-19 pandemic has resulted in a resurgence in fresh Covid-19 infections leading to restrictions by various state governments impacting the trading values for the retail store operators and hindering the rental recovery for mall operators.

The footfalls in the malls are witnessing a declining trend from the first week of January 2022 with restrictions in major cities such as closing dine-in for restaurants, occupancy restrictions for multiplexes, and their closure in a few cities along with weekend curfews. This is sure to impact the rental recoveries for Q4 FY2022 and thereby FY2022.

“Also, the rental recovery for FY2022 is expected to be up to 70 percent of pre-Covid levels, as compared to earlier estimates of up to 75 percent recovery. However, the recovery post third wave is expected to be faster than the previous waves with short-tenured restrictions and expected quick ramp up for major tenant – multiplexes, as content line up remains robust with several big-budget movies ready for release,” Reddy further stated.

With the estimated rental recoveries over 85 percent of the pre-covid level, Q3FY2022 was the best quarter for the mall operators since the onset of the pandemic. The recovery was driven by pent-up demand, high vaccination coverage, resumption of multiplexes which also coincided with the festive season, experts believe.

While certain store categories such as hypermarkets, electronics, fashion, and beauty have done extremely well with certain brands even exceeding the pre-Covid sales, tenants such as department stores and food and beverage are observed to have moderate recovery in line with the improvement in footfalls in Q3FY2022.

“Weaker H1FY2022 due to second wave and expected reduction in recovery in Q4FY2022 due to the third wave of a pandemic is expected to impact the full-year FY2022 debt coverage metrics. The projected DSCR is estimated to be in the range of 0.70-0.75 times as against earlier estimates of 0.80-0.85 times,” Reddy added.

The trading values for these stores would be impacted by the third wave in Q4FY2022. Multiplexes will be the most impacted segment due to deferred movie releases.

READ MORE: How Expectations of Consumers and Retailers are Changing From Malls

Overall, the majority of the categories are expected to reach near-normalcy by Q1FY2023 as against earlier estimated Q4FY2022 with variance depending on the mall or brand-specific factors.

“The support from sponsors, debt service reserve, and undrawn credit lines (for few issuers) have helped ICRA rated malls in meeting their obligations during the H1FY2022. With improvement in rental recoveries, there was no significant shortfall or major dependence on sponsors in Q3FY2022. However, with 20-25 percent reduction in rentals in Q4FY2022, the malls would again be reliant to some extent on available bank balances and undrawn lines, in the absence of which timely sponsor support will be critical,” Reddy stated.

India's smartphone market has registered its highest-ever shipments at 169 million units in 2021 to register 11 percent year-on-year growth from about 152 million units in 2020.

The market showed high resilience in a year that witnessed a second and more virulent Covid-19 wave as well as supply disruptions and price increases due to the ongoing component shortages, according to a report by Counterpoint Research.

Also, the increased adoption and demand for 5G smartphones was one of the key factors for high shipments in 2021, the report added. And, 5G smartphones contributed to about 17 percent of the overall shipments in 2021, registering 6x growth compared to 2020.

"Intense competition among OEMs, availability of cheaper 5G chipsets, and declining prices of 5G devices will enable brands to push more 5G devices into the market. The price of entry-level 5G devices has come down by 40 percent in the last six months. The increase in affordability of 5G devices has been a key reason for high 5G smartphone adoption," the report stated.

Consumer demand remained high in the premium price tiers (above Rs 30,000) in 2021 with shipments in these price bands growing 98 percent y-o-y.

The under-Rs 10,000 category -- which accounted for 30 percent market share, declined 5 percent, while Rs 10,000-20,000 segment (47 percent share) grew 8 percent. The Rs 20,000-30,000 tier (13 percent) grew 95 percent.

The retail ASP (average selling price) also showed high growth, increasing by over 13 percent y-o-y, the report added.

READ MORE: Smartphone Market Moving Towards a Steady Growth and Recovery Stage

"High installed base, as well as high replacement demand coupled with the increasing affordability of premium devices, led to the high growth of the premium segment. Going forward, we expect the market to continue to grow by double digits with a healthy contribution of the mid-to-high-end 5G smartphones. India's smartphone market continues to offer big opportunities for multiple players to grow and co-exist," the report said.

The consumer and retail sector showed tremendous signs of recovery in the previous year. However, with the sudden spurt in COVID-19 cases recently, concern has arisen with regards to the growth momentum of this industry. Budget 2022 holds great hope and significance for a complete revival of the sector.

54 percent of MSMEs feel that more skill development initiatives are required to make it competitive globally, according to the survey by Grant Thornton Bharat. MSMEs are the backbone for the sector and with the right talent, they can provide exceptional results.

Also, with regards to Aatmanirbhar Bharat and to promote growth in domestic manufacturing, 41 percent of the respondents wish for rationalization of basic customs duties on certain imports, after taking into consideration the FTA benefits. This was followed by 30 percent wishing for the implementation of the National Retail Policy, to strengthen and boost the retail ecosystem and facilitate ease of doing business, the report further stated.

Naveen Malpani, Partner and Consumer Sector Leader, Grant Thornton Bharat stated, “The consumer retail sector is hoping for the implementation of a National Retail Policy, and an efficient tax refund process to prevent credit blockage. With the right government support, private sector players are willing to invest more in building efficient supply chain infrastructure as well as technology innovation to improve global competitiveness.”

Looking at the success of the PLI (production-linked incentive) schemes, the survey also hinted on the government to consider rolling it out to new sectors like toy manufacturing (20 percent), footwear (23 percent) as well as personal care and cosmetics (37 percent). Talking about GST law, almost half the respondents said that they needed more clarity on the input tax credit, followed by supply and value of supply. 50 percent also wish for Income Tax special exemptions to enhance and boost the spending capacity of the people in the current fiscal. More liquidity in the hands of consumers has a direct positive impact on the consumer and retail sector since it increases the consumer’s propensity to spend.

India’s start-up ecosystem has boomed in 2021 like never before. Record $36 billion funds in 2021 were channeled to the start-up sector last year alone, with 40 start-ups entering the unicorn club. Given there is no shortage in the circulation of capital in the start-up ecosystem, what can the government bring in maybe in terms of eradicating the unique challenges faced by these companies in various sectors or bringing more start-up-friendly policies, and so on?

“The three areas that the government may focus on in the upcoming Union Budget 2022 include a) Taming inflation, b) Manufacturing incentives, and c) Cutting the export red tape. Mostly due to supply-side issues, inflation has been running high on most inputs used by the beauty and personal care industry," states Shankar Prasad, Founder and CEO, Plum.

Inflation is indeed a major macroscopic challenge for the government which may be putting a lot of toll on the start-ups particularly those that may want to scale based on the initial successes. The issue of inflation is however not unique to India, globally over the past twelve months, the rate of inflation has shot up from under 2 percent a year ago to over 5 percent by August 2021, according to a report.

While the Government has taken certain steps to ease supply constraints, concerted efforts in this direction are necessary to restore supply-demand balance. "The nascent and hesitant recovery needs to be nurtured through fiscal, monetary, and sectoral policy levels," said Monetary Policy Committee.

Indeed, the sustained challenges by the pandemic and the currently rising third wave have put several halts on the recovery graph of every sector, start-ups taking the most hit.

Abhishek Gagneja, Founder, Yoga Brands says, “Not undermining the death and devastation Covid-19 has caused, it has been a key driver for Digital and D2C Start-ups which have thrived despite the lockdowns and attracted massive funding in 2021. These disruptive business models have great potential to lead India towards economic growth, innovation, ease of living, livelihoods, and a digital economy. At the same time, it could lead to a bubble if not supported by reforms tax and administrative reforms as sooner or later Investors will expect these companies to become profitable.”

Demand for Better Tax Slabs

Presenting better tax slabs in the budget seems to be the common demand for the government from the start-up ecosystem.

Kapil Bhatia, Founder, and CEO, UNIREC states, “The fashion startups are expecting the government to improve the disposable income of the consumers as well as the reduction in GST rates of readymade clothing. Current GST rates of readymade clothes that cost above Rs 1,000 fall under the category of 12 percent and the government should bring it down to 5 percent.”

On similar lines, Rohit Sahni, Co-Founder and CEO of WK Life says: "We have an immense tax burden and we are hopeful that the budget will explore opportunities in allowing startups to carry forward losses, setting off previous losses against income and unabsorbed depreciation under Section 72A of the Income Tax Act."

Praveen Chirania, Founder, Muscle and Strength India asserts, “Self-care, preventive healthcare, and holistic wellness have taken center stage with a growing awareness around nutrition and immunity among consumers. It has become an important line of defense during the pandemic proving the dietary supplements sector to be a strong economic partner to the people. Hence to give impetus to the overall industry, we hope that the government will rationalize GST on healthcare supplements from 18 to 5 percent in the upcoming Union Budget 2022.”

Sanjay Desai, Director, Fabcurate said, "To reduce the burden, customs duties on raw materials and intermediaries should be brought down. Expectations of reduction in tax burden, to enable ease of doing business for small businesses. When tax will be reduced, it will bring in more investors and more job opportunities will arise, which will eventually help to increase the economy."

Not just direct tax reduction, the start-ups also expect to facilitate them in terms of compliances and more importantly in simplification of taxes. Just to illustrate the importance of this further, a complex unfriendly capital gains tax system is a big reason why many Indian start-ups have relocated their headquarters outside India, according to a report on direct tax administration brought out by the Bangalore Chamber of Industry & Commerce (BCIC.)

Sahni states, "The government should also consider assisting startups through policies and support mechanisms towards domestic capital participation, favorable investment climate in Tier II and Tier III cities, tax exemptions in foreign direct investments, and a high focus on startup infrastructure development.”

“In addition to tax rate reduction, easier compliance and simplification of taxes are two of the major expectations of the functional fashion startups in the market," Bhatia adds.

Besides the fashion segment, personal care, technology, e-commerce, healthcare, are some of the most thriving sectors of recent times and will surely be looking up to the budget to further their growth prospects.

Push For Local Manufacturing

With many start-up players holding huge capital that they do, it wouldn't be fair on the part of the government to not take advantage of that and foster the growth in the local manufacturing. It wouldn't be in the country's interest if those startup companies continue to rely on foreign manufacturing units to grow their business.

Lalit Arora, Co-Founder of India's leading Consumer Electronics brand VingaJoy states, “We hope that the upcoming budget will have provisions for strengthening the entire system and take progressive initiatives such as ‘Make in India’ and ‘Digital India’. We are hopeful that the Government would continue extending its valuable support as initiated in the first term with the implementation of uniform GST, 'Make in India', besides offering a host of other initiatives that would help industries to come back to the platforms."

Priyanka Salot, Co-founder of popular Indian mattress brand The Sleep Company also said, "With its expected focus on economic recovery, we can expect a further push towards boosting the startup ecosystem in the Union Budget 2022-23, particularly for companies that are working under the 'Make in India' initiative. Manufacturing startups have made a headstart in exports, but need critical support in areas like obtaining international patents and a renewed focus on the logistics sector. The focus on encouraging growth must be encouraged incentivizing business deployment along with building a robust forward-looking business ecosystem."

Bala Sarda, Founder, and CEO of VAHDAM India added: "The budget can look into widening the ambit of Special Startup manufacturing zones for companies or startups which want to foray into manufacturing. This would give the government's "Vocal for Local" initiative a timely fillip"

In the previous budget, the government in its bid to benefit the D2C sector took a number of steps, such as the extension of tax holiday for startups, an extension of eligibility period of claiming capital gains, and pushing the paid-up capital of small firms from Rs 50 lakh to Rs 2.50 crore. Experts believe that the government needs to up the game in the same spirit to further foster growth in the start-up ecosystem.

Himanshu Gandhi, Co-founder, and CEO of Personal care brand Mother Sparsh said, "We expect the Finance Minister to extend the purview of Start-up India Seed Fund Scheme to promote startups that achieved remarkable feats during the pandemic. In this budget, the government should provide financial assistance to growth-oriented startups with proven capabilities to enhance their R&D, product trials, prototype development, and proof of concept.

Truly, the government can provide specialized funds, which many industry experts would agree, depending upon the type of work the start-up is doing and the assistance needed by them. Also, more transparency in terms of the schemes and programs brought under the government’s flagship Start-up India program so that start-ups can avail the rightful benefits from the same.

India’s trade performance has improved a lot in recent times. In fact, it can hit $65 billion if the industry majors take the right steps and there is proper execution of government schemes.

Exports declined by 3 percent during 2015–2019 and by 18.7 percent in 2020, according to a joint report by global consulting firm Kearney and The Confederation of Indian Industry (CII) said. Also, during the same period, other low-cost countries such as Bangladesh and Vietnam have gained a share.

“We believe with the right actions from the industry majors and robust execution of government schemes, India can hit $65 billion in exports (implying 9-10 percent CAGR) by 2026. This, coupled with growth in domestic consumption, could propel domestic production to reach $160 billion. Given the labor-intensive nature of this industry, this growth could add 7.5 million direct jobs in textile manufacturing,” said Siddharth Jain, Partner, Kearney.

There are in fact a variety of factors that have contributed to India’s recent trade performance. India has factor cost disadvantages (for example, power costs 30 to 40 percent more in India than it does in Bangladesh). Lack of free or preferential trade agreements with key importers, such as the European Union, United Kingdom, and Canada for apparel as well as Bangladesh for fabrics also put pricing pressure on exporters.

"The high cost of capital and high reliance on imports for almost all textiles machinery makes it difficult to earn the right return on invested capital, especially given India’s slight cost disadvantage. Longer lead times than for Chinese manufacturers make India uncompetitive, especially in the fashion segment. For example, India’s lead time is 15 to 25 percent longer than the competition in fabrics. Limited presence in the global trade of man-made fiber products. The trend of nearshoring in western economies has not helped either," the report further added.

Textile products hold a key position in the global value chain, with India being the world’s fifth-largest exporter for apparel, home, and technical products. The Textile industry employs almost 45 million people in the farming and manufacturing sectors. However, many experts say that the country’s recent performance in global trade has not been commensurate with its abilities.

“Covid-19 has triggered the redistribution of global trade shares and a recalibration of sourcing patterns (“China plus one” sourcing), providing a golden opportunity for Indian textiles to stage a turnaround and regain a leadership position as a top exporting economy. We believe India’s textile industry should target 8 to 9 percent CAGR during 2019–2026, driven by domestic demand growth and significant growth in annual exports (reaching $65 billion by 2026),” Neelesh Hundekari, Partner and APAC Head - Lifestyle Practice, Kearney said.

Achieving the $65 billion export target up from $36 billion in 2019 will require India to double down in the five key areas - apparel, fabrics, home textiles, man-made fiber and yarn, and technical textiles, experts believe. And, the path to achieving these targets will entail both government and industry taking crucial steps. And the government seems geared up for the challenge.

“The recent launches of multiple schemes such as MITRA, PLI, RoDTEP highlights the strong government focus on this sector. It will be critical for the government to follow up these launches with efficient implementation and even more critical for industry players to leverage these schemes effectively,” Jain added.

Given a lot of retail markets in Tier-I cities have reached close to a saturation point, businesses have started to explore and expand into rural markets and non-metro cities. Consequently, these businesses have been eyeing to understand consumer trends and stats that will help them build their strategies to thrive in the market.

Soaps, candies, snacks, beauty products, sanitary pads, and electrical products happen to be the front runner for sales, according to a report by B2B aggregator platform Xpand. The company itself has been growing 46 percent MoM growth since August in rural markets.

With hygiene being of importance due to the pandemic, soaps and antiseptics have been the best-selling products. Additionally, house cleaning solutions have contributed a significant 68 percent to the business, the report added. It also dissects the geographical representation of the total business contribution. While the North of India contributes 54 percent of the total sales, the West and the South stood at 16.4 percent each. The East, however, comes at the lower end with a contribution of 12.3 percent.

Another observation is with growing aspirations, many suburbanites/rural Consumers do not seem to be minding paying more for premium products that may provide value Vs its price. In the smaller SKUs, this choice has been more evident. Cheese crackers and digestive biscuits have had more buyers than the regular glucose ones.

Sanjay Kaul, Founder, and CEO, Xpand, said, “There is significant untapped potential in the commercial space in the suburban areas and a great opportunity for brands to establish themselves in one of India’s big markets segments. While our recent report highlights many insights, but one key observation has been the growing aspirations of the villagers. As the Euromonitor International lifestyle survey suggested, many suburbanites are looking to elevate their lifestyle standards. We will keep ingressing towards the market in the rural space and support with a consistent flow of relevant categories to help them simplify their daily lives.”

The third wave is expected to push the recovery in multiplexes by up to five months as governments resort to the temporary closure of movie halls to contain the spread of the Covid wave.

Also, the full revenue recovery of the multiplexes will be pushed back to the second half of the next fiscal as against the first quarter earlier, according to a report by Crisil Ratings.

However, once the restrictions are lifted, the pace of recovery is expected to be sharp - as was witnessed after the second wave - and should limit further downside in the credit profiles of multiplex operators along with healthy balance sheets, experts believe.

"The temporary closure of operations in New Delhi/ National Capital Region, Bihar, Haryana, and restrictions in other key states, such as Maharashtra, will push back new film releases," said Nitesh Jain, Director, Crisil Ratings.

Stating that a few big-ticket films such as 'RRR' and 'Jersey' have already been postponed indefinitely, Jain said in his base case, he assumes the third wave to peak in February and bottom out by the end of March, which will mean the release of big-ticket content to resume in the first quarter of fiscal 2023.

In fact, occupancy doubled to 20 percent in December 2021 from 10 percent in September, indicating healthy demand, and could have improved to over 25 percent this quarter compared to 30 percent pre-pandemic as several big-ticket films were scheduled for release, the report further added.

Right now, there will be operating losses because of the third wave but healthy liquidity of Rs 880 crore as of September 2021 would comfortably cover operating expenses and debt obligations for the next 4-6 months, many experts believe.

"Theatre releases will also bolster revenue from the food and beverages (F&B) segment, which accounts for 25-30 percent of the topline of multiplex operators," said Rakshit Kachhal, Associate Director, Crisil Ratings.

Downside risks for the industry, which need to be watched include sustainability of cost-control measures and the prolonged impact of the pandemic.

Over 40 percent of the total online businesses at present are run by women entrepreneurs. Also, more women-led DTC businesses have come to light in recent times given the phenomenal success they've experienced.

Also, looking forward, the year 2022 is expected to be ruled by consumer sentiment. As e-commerce grows, brands will be conscious of the product they are selling, and also how they are selling it, according to a report by full-stack digital solutions provider Instamojo. And, there will be a heightened focus on sustainability, not just for the product but for the entire supply chain.

Sampad Swain, CEO, and Co-Founder, Instamojo, said, “As entrepreneurs and small businesses increasingly learn the benefits of selling independently online, we can expect the DTC model to catalyze business growth significantly in the coming quarters. In the last couple of years, both digitization and changing consumer behaviors have made it imperative for small businesses to move and/or expand online."

In fact, last year, we have seen several D2C businesses becoming unicorns.

"To this front, in the post-pandemic world, the DTC model can be an effective solution to accelerate business recovery. It is heartening to see the digital growth of this sector which has mostly been defined by traditional business models. As we witness the shift of DTC businesses to the online medium, we aim to support the growth journey of more than 250,000 small business owners as they strive towards becoming digitally independent,” Swain further said.

Secondly, another major important trend that has become hugely popular is social commerce. It is likely to be the preferred channel for e-commerce from a consumer PoV, according to the report.

To share some figures, 40 percent of the entrepreneurs on Instamojo that signed up in 2021 had a business profile on social media. Also, to replicate the mall experience, people are hopping on social media LIVE streams to shop while feeling like a part of a community.

Thirdly, revenue-based financing takes center stage. "As homegrown and independent businesses rise in number, there will also be a significant shift to revenue-based financing over traditional venture capital," the report further stated.

And lastly, SEO (Search Engine Optimisation) is expected to become the most important marketing channel. Moreover, SEO to become the biggest free acquisition channel for DTC brands in India in 2022, the report added.

Gen Z and Millennial shoppers are now more likely to order products directly from brands, and 72 percent of all shoppers expect to have significant interactions with physical stores once the pandemic subsides – up from 60 percent pre-Covid.

More than two-thirds (68 percent) of Gen Z and over half (58 percent) of Millennials have ordered products directly from brands in the past six months, compared to 41 percent on average across all age groups. Only 37 percent of Gen X and 21 percent of Boomer shoppers have ordered directly from a brand in the last six months, according to a new Capgemini Research Institute report.

Also, for those who have bought directly from brands, almost two thirds (60 percent) cite a better buying experience as a reason for purchasing directly, and 59 percent cite access to brand loyalty programs.

Moreover, in return for these benefits, consumers are willing to share their data. Currently, almost half (45 percent) of all shoppers say they are willing to share data on how they consume or use products and more than a third (39 percent) say they are willing to share personal data such as demographic information or product preferences. However, 54 percent of all shoppers say that offers, deals, and/or discounts would make it more likely for them to share their data directly with brands.

Tim Bridges, Global Head of Consumer Goods and Retail, Capgemini said, “Younger consumers’ willingness to go straight to brands when purchasing goods presents a real opportunity for consumer product companies. This enables them to collect consumer data and helps create a more mature direct-to-consumer channel. Being data-powered enables the consumer product and retail organizations to translate supply and demand trends into intelligent decisions on where best to stock their products, customize products and services and enhance customer experience.”

Also, despite the growth in the e-commerce channels of shopping, it is not likely to replace in-store shopping entirely, experts believe.

The surge in e-commerce over the last two years due to safety concerns and the desire to avoid physical stores has now plateaued. The notion that online may replace in-store entirely has been disproven, and the majority of consumers (72 percent) expect to have significant interactions with physical stores after the pandemic subsides – exceeding pre-Covid numbers (60 percent).

Globally, all age groups expect their level of in-store interactions post-pandemic to be higher than their online interactions. Boomers are the most likely to interact in-store (76 percent), and Gen Z is the least likely (66 percent).

However, the nature of these interactions is changing as the distinction between online and in-store continues to blur. For instance, post-pandemic, 22 percent of shoppers expect to have a high level of interactions with click-and-collect orders. This trend is highest for Millennials (33 percent) and lowest for Boomers (11 percent).

Delivery and fulfilment services gain importance in certain segments

With convenience remaining a key priority for consumers, delivery and fulfilment are increasingly being transformed from a cost centre to a growth driver for many organizations. In the health and beauty and grocery segments, shoppers place greater importance on delivery and fulfilment than in-store experiences. This is especially true for groceries shoppers across all age groups, where 42 percent of shoppers say that delivery and fulfilment are the most important service attributes.

Prices of air conditioners and refrigerators have shot up in the new year as consumer durables makers pass on the impact of rising raw material costs and higher freight charges to customers, while home appliances like washing machines may witness 5-10 percent price hike later this month or by March.

Several companies including Panasonic, LG, Haier have already reviewed prices upwards, while other makers such as Sony, Hitachi, Godrej Appliances may take a call by the end of this quarter.

Moreover, the industry makes hike prices from January to March in the range of 5-7 percent, according to the Consumer Electronics and Appliances Manufacturers Association (CEAMA),

"With an unprecedented surge in the cost of commodities, global freight and raw materials, we have taken steps to increase prices of our products by 3 to 5 percent in the refrigerator, washing machines, and air conditioner categories," said Satish N S, President, Haier Appliances India.

Similarly, Panasonic, which has already increased prices up to 8 percent for ACs, is considering hikes further. It is also mulling a similar move for home appliances.

"Air conditioners have already seen a price hike of around 8 percent and this may further go up depending on rising costs of commodities and supply chain. We can also see a reflection of price hike for home appliances too in near future," stated Fumiyasu Fujimori, Divisional Director, Consumer Electronics, Panasonic India.

South Korean consumer electronics major LG, which has also increased prices in the home appliances category, said a constant hike in input raw material costs and logistics cost has been a concern.

"We have tried best to absorb the same through cost innovations but prices need to increase for business sustainability," said Deepak Bansal, Vice President - Home Appliances and Air Conditioner Business, LG Electronics India.

Other industry leaders have similar views on the matter.

Eric Braganza, President of, CEAMA said, "The industry had postponed the price increase due to the festive season. However, currently, manufacturers have no other option but to pass on the price hike to customers. We expect the industry to do a round of price hike from January to March in the range of 5-7 percent."

Implementation To Vary

However, experts believe that the implementation would vary from company to company as some of the manufacturers have already hiked prices and some are in the process of doing it.

Companies such as Sony and Godrej Appliances said they are yet to take a call.

"Price correction is not on the cards at the moment," said Sunil Nayyar, Managing Director, Sony India.

And, Kamal Nand, Business Head & Executive Vice President, Godrej Appliance has said, "I said going forward, the company will evaluate taking any further hike, given the current drop in demand due to increasing coronavirus infection rate."

Super Plastronics Pvt Ltd (SPPL), which has a branding license for international brands, including Thomson, and White-Westinghouse, said the consumer electronics industry has been observing price hikes on various levels at the backend of things.

"We are assuming that in the last quarter of this financial year, consumer electronics' prices will be hiked on all levels across most categories," Avneet Singh Marwah, CEO, SPPL added.

Gurmeet Singh, Chairman and Managing Director, Johnson Controls-Hitachi Air Conditioning India added, "Increase in input costs - raw material prices, taxes, and transportation fares are pushing brands to increase prices of air conditioners. In a phased manner, upto April, prices will go up by at least 8-10 percent. Prices have gone up from around the same time last year December to this year by nearly 6-7 percent."

"The onslaught of Cost Up is continuing and now with Anti Dumping Duties being imposed on Aluminium and Refrigerants, we see another increase by 2-3 percent. This will be over and above the actual commodity increase on these items and is inevitable. We rationalise the price as much as possible at our end. We make sure that the consumer gets the best cutting-edge technology good quality products at the price they are paying," Singh further added.

Last year’s figures for the luxury segment have shown several positive signs, despite the slow growth since the post-pandemic period. For instance, in the first nine months of 2021-22, the value of gold imports exceeded the last full year’s number of $34.60 billion to reach $37.98 billion. Given the pent up demand and revenge buying, the luxury fashion segment has also seen noticeable growth in recent times.

For the gems and jewelry industry, specifically, due to the period of festivities in the last couple of months, spending on luxury goods has seen an unprecedented hike.

Pankaj Khanna, Chairman of Khanna Gems shared, “With the festivities being celebrated with full fervor and people’s inclination towards investment, people came with a higher purchasing power which has benefitted us.”

Given the demand, Delhi-based Khanna Gems has shifted focus from sales to expansion and launched 8 stores in different states, thereby expanding its reach. The company further plans to launch more stores based on the positive response from the various newly opened stores in Bengaluru, Delhi/ NCR, Lucknow, and Mumbai.

“We witnessed record demand for Astrological gemstones in the post-Covid era, to ease out the rising scenario of anxiety and depression in the country. For the further expansion of the business, we plan on investing heavily in traditional forms of advertising like hoardings, etc. in addition to the investment in digital marketing," Khanna further added.

In fact, more than 80 percent of companies in the top 100 reported lower luxury goods sales in FY2020, which reflected the adverse impact of the pandemic, according to a report by Deloitte. However, despite a fall in luxury goods sales growth, more than half of the top 100 companies were profitable in FY2020.

"We have definitely seen an increase in sales during the festive and end of year season. Most people saved a lot with smaller weddings and are investing that in buying jewelry. There is a lot more money that has now been kept aside for big jewelry purchases, both for celebrations and as investments. This rise in purchasing power has also allowed people to look favorably towards luxury minimal jewelry," said Vastupal Ranka, Director, Rare Jewels - A Ranka Legacy.

However, with the third wave coming in, the slow but steady trajectory of the sector is now expected to be affected, yet again. However, with the country being hit by the pandemic majorly twice, this time the industry is expected to be more prepared than earlier.

Rohan Gupta, Managing Director, Gargee Designer's shared his views on the matter: “The luxury sector has been on a slow yet steady recovery, but not up to its full potential. If the impact of the expected 3rd wave of the pandemic does not turn to be as harsh as it was the last time, and if things are under control, then the luxury sector will rise back and flourish."

Founded in 1980, Gargee Designer’s is a popular name in the men’s designer wear space and has a long experience working in the luxury space.

Possibilities In 2022

Despite the ups and downs in the luxury goods market, the sector holds massive potential for growth. According to Euromonitor International, India's luxury goods market will be worth $8.5 billion in 2022, against $6 billion in 2021.

And, like other sectors, technology is going to play a major role in the growth of the luxury sector. A report by McKinsey stated that nearly 80 percent of luxury sales today are digitally influenced - whether it is asking a friend on social media or checking out an influencer’s recommendation on Instagram. Also, it forecasts nearly one-fifth of global luxury sales will take place online by 2025.

Not only that, looking at the possibility that the sector holds, businesses are expanding their portfolio to include luxury goods.

For instance, B2B fashion marketplace Louoj is planning to open its luxury vertical of customized clothing B2C platform in the coming months.

Bibhuti Bhusan Dash, Founder and CEO, Louoj commented on the growth in the luxury sector, saying, "Established or new fashion brands - all share similar concerns of keeping up with the technology, dealing with a lean budget and taking a downward trend retail outlets sale."

Thus luxury firms are optimistic and are adopting new technologies and strategies to upgrade their processes, and when the situation gets better, they are going to implement all the necessary means to get their business in action.

"Going ahead we are only expecting this demand and shift in luxury jewelry to rise. We plan on introducing a new range of luxury minimal jewelry and a range of special bridal jewelry too," Ranka further stated.

Khanna of Khanna Gems too echoed similar thoughts, stating, "We expect 2022 to be even more favourable for the gems and jewelry industry as the pent-up demand in the national market and export markets also needs to overcome.”

The $492 billion global social commerce industry is expected to grow three times as fast as traditional e-commerce to $1.2 trillion by 2025.

The growth is predicted to be driven primarily by Gen Z and Millennial social media users, accounting for 62 percent of global social commerce spending by 2025, experts believe.

Social commerce means a person’s entire shopping experience — from product discovery to the check-out process — takes place on a social media platform. Also, it uses networking websites such as Facebook, Instagram, and Twitter as vehicles to promote and sell products and services.

Just under two-thirds (64 percent) of social media users said they made a social commerce purchase in the last year, which reflects nearly 2 billion social buyers globally, according to a report by Accenture.

“Driven by mobile-first consumer preferences and the launch of new hyperlocal social commerce platforms, the emerging success of social commerce in India is a testimony to the power of people and communities,” said Anurag Gupta, Managing Director and Lead - Strategy & Consulting, Accenture in India.

“To take advantage of this growing opportunity, it will be crucial that these social commerce platforms offer consumers the right experience built around trust and satisfaction, and broaden their appeal through the use of local languages and video interfaces. Furthermore, brands need to work with a thriving ecosystem comprising platforms, creators, influencers, resellers that helps users discover and evaluate potential purchases,” Gupta further stated.

While the opportunity is significant for large businesses, individuals and smaller brands also stand to benefit. More than half (59 percent) of social buyers surveyed said they are more likely to support small and medium-sized businesses through social commerce than when shopping through e-commerce websites, Furthermore, 63 percent said they are more likely to buy from the same seller again, showing the benefits of social commerce in building loyalty and driving repeat purchases, the report further said.

Also, half of social media users surveyed, however, indicate they are concerned that social commerce purchases will not be protected or refunded properly, making trust the biggest barrier to adoption, as it was for e-commerce at its beginning.

Understanding Consumer Demand

By 2025 the highest number of social commerce purchases globally are expected in clothing (18 percent of all social commerce by 2025), consumer electronics (13 percent), and home décor (7 percent), the report further added.

Fresh food and snack items also represent a large product category (13 percent) although sales are nearly exclusive to China. Beauty and personal care, although smaller in terms of total social commerce sales, is predicted to quickly gain ground on e-commerce and capture over 40 percent of digital spend on average for this category in key markets by 2025.

If we look at it globally, consumers in developing countries are more likely to use social commerce and do so often. Eight out of ten social media users in China use social commerce to make purchases for a given category, while the majority of social media users in the U.K. and the U.S. have yet to make a purchase via social commerce.

Three out of every four Indians now prefer asset owning over renting to secure their future in the post-pandemic world. Also, one in four Indians feels purchasing a home of their own is crucial in securing their future, second to securing a career.

Moreover, one in two Indians reveal that they have started looking for a new house for themselves; almost one in every third Indian believes buying a new house is the best investment option at present, according to the latest study, Post 'Generation-Rent' commissioned by Godrej Housing Finance (GHF).

Manish Shah, MD and CEO, Godrej Housing Finance, said on the matter: "The pandemic has brought about a clear shift in preference amongst Indian consumers. They are gravitating towards future-proofing through long-term investments. With affordability at an all-time high, there has probably never been a better time to buy a house, which is both an important element of asset allocation and a key pillar of financial security. That said, customers believe that this change requires enhanced support from their financial partner to advise and guide them through this long-term commitment."

Industry experts predict a continued uptick in the coming months, easing the long period of pent-up demand across sectors. The survey validates the sentiments as most of those surveyed stated they are now more open to investing in a property of their own divagating from the earlier notion of being labelled as the 'Generation-Rent'.

Specifically, around 62 percent of Indians highlighted that they now preferred purchasing their furniture, car, home, and wedding apparel rather than renting them as this provides them with greater stability in future.

The study also found that 25.5 percent of the Indians consider owning a home the second-most important aspect defining 'personal security', with job security leading the chart with 40.6 percent voting for it.

Flexibility on policy, credibility and transparency of the brand, digital offerings, and relative turnaround time for processing are the top factors that drive the selection of financing partner. This can be attributed to consumers becoming accustomed to the on-demand gratification of their requirements aided by digital technology, experts believe.

Also, digital-first and frictionless processes are perceived as both an advantage and a starting point for consumers while choosing today's financing brands. Companies and services that offer end-to-end digital solutions gain an edge in consumer preference over more traditional financing models.

72 percent of consumers have spent more on fashion in 2021 than the previous year, indicating a resurgence in consumer spending and demand in the segment. Customers in the age group of 18-30 drove the demand for online fashion with 71 percent of them spending on the category.

The average ticket size of transactions by women shoppers is 20 percent higher than that of male transactions, according to a consumer survey authored by fintech firm ZestMoney.

58 percent of the respondents have said they have spent more than Rs 5,000 on their fashion needs over the last 3 months. About 54 percent said they would prefer BNPL to finance their fashion purchases. Debit, credit cards, and cash were the other popular options.

The top Tier I cities driving demand for fashion and beauty are Delhi, Bangalore, Mumbai, Hyderabad, and Pune. Top Tier II and III markets fuelling demand included Assam, Anantapur, Haridwar, and Kanchipuram.

E-commerce platforms remained the preferred means of buying for the majority of customers, with 72 percent preferring online shopping due to the enhanced convenience and hassle-free experience it provides. However, 76 percent said they were also comfortable purchasing in person at physical stores

“Globally, fashion and beauty are the biggest categories for BNPL. In India, fashion and lifestyle are emerging as one of the largest categories for us. Consumers love the flexibility and convenience of paying later for their fashion purchases and we expect the category to see increasing adoption,” said Lizzie Chapman, CEO and Co-Founder ZestMoney.

Today’s digitally-savvy millennials and Gen Z are increasingly taking to pay later to fund their fashion needs. In fact, we have seen a 100 percent growth in transactions for the category with the merchant base doubling over the last three months. We are adding the largest merchants in the space, especially direct-to-consumer (D2C) brands who want to enable affordability for their customers. This is a category that will see a lot of action in the coming year too.”

Among other trends, observable 73 percent said they are environmentally conscious and prioritize sustainability while shopping for fashion. This indicates the rising trend of customers making eco-friendly choices and supporting brands that endorse ethical fashion. 75 percent of respondents preferred supporting local, home-grown brands over International brands to push made in India. 88 percent of respondents stated that comfort continues to drive their sense of style and fashion purchases. Fashion influencers were the go-to for 51 percent of respondents while opting for a particular brand or style.

The retail sales in November 2021 showed 9 percent growth over the pre-pandemic levels (November 2019) and 16 percent (YoY) growth (compared to November 2020).

Also, across regions, retail businesses have indicated growth in sales as compared to pre-pandemic levels with West India signaling the growth of 11 percent, followed by East and South India at 9 percent while North India indicated a growth of 6 percent each as compared to sales levels in November 2019, according to a recent survey by the Retailers Association of India (RAI).

Kumar Rajagopalan, CEO, Retailers Association of India (RAI), said, “Business is improving and we do hope that this will sustain. However, there are still worries around Omicron and the third wave, leading to a feeling of cautious optimism.”

In categories, CDIT (Consumer Electronics, Durables, IT, and Telecom) which did not show great growth in October showed good growth (32 percent as compared to November 2019) in November since customers ended Diwali with some CDIT product purchases.

Furthermore, Sports Good category reported a growth of 18 percent and the Apparel category indicated a consistent growth at 6 percent compared to November 2019. While Food and Groceries and Quick Service Restaurants (QSR) continue to indicate growth, categories such as Footwear, Beauty, Wellness & Personal Care, and Furniture are inching towards recovery.

Experts believe with a firm focus on digital transformation, the industry has set a steady pace of recovery, which the industry hopes will accelerate in the coming year.

Despite the uniquely unpredictable situations in the last 2 years, the year-end holiday gifting ritual has remained a constant amongst Indian shoppers. Consumers’ approach towards traditional gifting has significantly shifted, however, with 68 percent of shoppers willing to purchase gift cards that give back to causes and 91 percent intending to send gifts to people who’ve experienced hardships.

Consumers will purchase an average of 22 gift cards, the Indians are expected to spend 89 percent of their holiday gifting budget on gift cards, with fashion and health and beauty being the most popular gift card categories, as per the forecast by Global branded payments provider Blackhawk Network.

Additionally, 84 percent of Indian shoppers said they do not want to deal with the hassle of returns or exchange of gifts. Interestingly, 62 percent acknowledged that they receive at least one bad gift every year.

This changing perspective towards gifting presents a new opportunity for retailers to connect with their consumers, as both retailers and shoppers seek newer ways to navigate the challenges that the 2021 year-end holiday season has to present. The report also stated that almost 96 percent of Indian respondents want to gift digitally in the upcoming holiday season.

“In India, year-end gifting has become a big trend as it is an occasion to gift friends and family. The past year, we’ve seen a growing preference for gift cards among Indian shoppers owing to convenience, choice, and safety. Our research reveals that consumers are planning to spend more money on buying gifts this year than they did in 2020," said Theresa McEndree, Head of Global Marketing and Corporate Brand, Blackhawk Network.

"However, consumers’ preferences and priorities have notably changed. This shift has posed unique challenges for retailers and businesses to engage and delight customers. Year-end 2021 opens new windows for retailers to align their strategy to meet the expectations of shoppers,” McEndree further said.

As some areas of the globe become over-farmed, over-populated, or otherwise reach their maximum potential, opportunities in Tier II, III cities, and rural areas emerge for brands to explore. Cross-border logistics, broader network coverage, and ease of connectivity will further support the increasing penetration of e-commerce players across untapped regions.

Winners will be those who move first and build a deep-rooted, broad reach across customers, experts believe. In fact, to face the increasing competition, conventional retailers and mom-and-pop stores are now connecting with customers via business-to-business (B2B) e-commerce platforms and selling products online both domestically and internationally.

Benefiting from advanced digital and transportation infrastructure, together with the rising middle classes in tier-II cities, China, Asia-Pacific (APAC) and the Middle East are spearheading a revival in conventional retail and mom-and-pop stores through digital commerce, according to a recent study 'E-commerce megatrends to watch’ by transportation firm FedEx Express.

“The Asia Pacific, Middle East, and Africa (AMEA) region will be at the forefront of e-commerce growth for many years to come. With rising disposable incomes, growing internet penetration, and emerging cross-border e-commerce markets, there is a huge amount of growth yet to be realized here,” said Kawal Preet, President of the Asia Pacific, Middle East, and Africa (AMEA) region, FedEx Express.

“Logistics is the backbone of the e-commerce ecosystem. The simplicity of click to buy must be matched by the speed and convenience of delivery. We continue to build robust networks that offer smart supply chain solutions as well as highly personalized delivery services to help businesses unlock new opportunities as the frontiers of e-commerce advance,” Preet further added.

Reportedly, e-commerce is expected to grow at an average of 47 percent in the next five years globally. The Asian market leads the field at 51 percent, followed by Europe (42 percent) and North America (35 percent).

In the Middle East and Africa, the combined e-commerce market value is expected to reach $73 billion by 2025. However, growth in China, in particular, has eclipsed the rest of Asia, with e-commerce sales in 2020 that reached $1.3 trillion with a projected increase to nearly $2 trillion by 2025.

India's FMCG industry has seen a decline in volume in the September quarter this year, though it registered a value-led growth of 12.6 percent.

While the metro market saw an upswing, rural markets slowed down due to consumption decline, according to a report by data analytics firm Nielsen. Earlier, rural was ahead of urban in terms of growth, after quickly recovering from the first wave of the pandemic.

The slowdown is also because of the fact macro-economic factors such as high commodity prices continued to impact consumption growth during the quarter.

The price-led growth is largely driven by the food basket, which contributes 59 percent to the FMCG industry. This was seen especially in staple foods like cooking mediums (edible oils), habit-forming foods like hot beverages such as tea, and impulse foods like salty snacks and confectionery. Volume growth is driven by packaged rice, breakfast cereals, butter margarine, and chocolates.

Moreover, small players were impacted the most while large players consolidated, the report said.

Of the total value growth of the FCMG industry in the September quarter, as compared to a year ago, 76 percent contribution came from large manufacturers, while small players had just 2 percent, the rest coming from mid-size players.

Moreover, brick-and-mortar was back in focus, as modern trade stores grew 17 percent in the quarter, registering double-digit growth as compared to the year-ago period.

The e-commerce channel growth remained steady during the quarter on account of the base effect, given the high growth of foods in e-commerce post the first wave of COVID-19 in the country.

According to the report, urban markets led by metros including Kolkata, Hyderabad, Mumbai and Pune led this growth.

Indian milk production is gauged to increase by 5-6 percent in the financial year 2021-22, aided by normal monsoon and early onset of the flush season in some regions of the country.

According to Icra’s report, the industry-wide demand to grow by 9-11 percent in the financial year 2021-22.

The report stated that the dairy industry is expected to grow by 9-11 percent in 2021-22, driven by a revival in economic activities, increasing per capita consumption of milk and milk products, changing dietary preferences due to rising urbanization.

"Demand recovery was stunted by the resurgence in COVID-19 cases in the first quarter FY22, and the impact was severe in institutional segments. However, there has been a healthy revival in demand in recent months with a sharp fall in fresh COVID cases and resumption in business activities. The organized dairy segment, which accounts for 26-30 percent of the industry has seen faster growth compared to the unorganized segment and we expect the trend to continue," Sheetal Sharad, Vice President and Sector Head at Icra, said.

Revival of Diary Industry

After the impact of the epidemic, the industry has seen a steady recovery in consumption throughout end segments. The report informed that revival in economic activities, increasing per capita consumption of milk and milk products, changing dietary preferences due to rising urbanization, and continued government support to the dairy industry will drive demand.

"With the expected recovery in demand during the festive season, skimmed milk powder (SMP) prices are likely to improve and lead to the liquidation of stocks in FY22. Raw milk procurement prices, which were subdued in FY21 due to weak demand, have increased in the current fiscal supported by a recovery in demand. Nevertheless, the higher procurement costs are not compensated by an equivalent increase in selling prices, which coupled with elevated fuel costs will result in contraction of 150 bps margins for dairy players in FY22," Sharad added.

Growth over the medium term would continue to be driven by demand from stable liquid milk consumption growth and steady recovery in institutional demand for the VADPs segment.

Government Supporting the Sector

Most industry players continue to maintain high SMP inventory levels as the procurement remained high in H1 FY22. As per the report, besides this, many soft SMP prices are expected to result in additional working capital debt requirements, though inventory levels are expected to decline from FY23 onwards as demand-supply dynamics normalize, it added.

The rating agency also expects private players to continue their capital expenditure on the VADPs segment, given its better margins.

The report stated that the financial risk profiles of pure-play ice-cream manufacturers are expected to be under pressure in the near term given the slow pace of recovery, it added. Further, the industry will remain supported by the government's continued support and favorable cost of funds leading to growing processing capabilities. Despite moderation in margins and increase in long-term debt and working capital debt (mainly due to SMP stocks), coverage indicators for integrated players are expected to be comfortable, it said.

The demand for logistics space in India remained resilient in the July-September quarter. Online retailers and related third-party logistics (3PL) firms led the leasing demand, in turn, preparing for year-end sales promotions. According to a report, net absorption of nine million sq ft occurred in the September quarter.

Going by CBRE's Asia Pacific report, the net absorption reached 27.4 million sq ft in Asia, a record quarterly high, despite disruption to manufacturing and container shipping.

"During the quarter, several occupiers were seen extending their distribution networks, particularly last-mile facilities, to shorten delivery times for consumers," the report said.

Around 172 million sq ft of new logistics supply is scheduled to be completed in Asia Pacific's primary and secondary markets in 2022, the highest annual total on record.

Strong Demand in Warehousing Segment