Mamaearth’s IPO valuation has become a topic of intense debate today. The proposed, super-premium initial public offering of Rs 2.900 crore has compelled industry insiders and think tanks to thrash out a multitude of factors to deduce its feasibility. At a time when the brand has been investing a lion’s share of its revenue (nearly 40 percent) on influencer marketing, the return on ad spend hasn’t inspired the trade much. The IPO valuation of $3 billion, as opposed to $1.2 billion in January last year, amounts to a staggering 1,000x jump in its profits, inviting intense scrutiny on social media platforms such as LinkedIn. The heat is such that even co-founder Ghazal Alagh’s and Varun Alagh’s defensive update denying the numbers doing the rounds, with a zing of Mamaearth’s vision, has done nothing to stifle the noise.

“Sharing below to throw some clarity on all the noise around valuations around our prospective IPO. In our DRHP as is the standard practice there is no mention of valuation. Valuation discovery is a process that will take place over time as we get into deeper conversations with the investor community. We have not quoted or subscribed to the valuation numbers which are getting mentioned in various posts on social media,” said Varun Alagh, Co-founder, Mamaearth in a LinkedIn post.

His statement was echoed by Ghazal Alagh, Co-founder, Mamaearth, who wrote, “We started Mamaearth with the purpose of providing toxin-free products for babies since we ourselves could not find the right products for our baby. God has been kind, luck favored us, consumers loved us and our team has put in crazy efforts to take it to a level where we are today with 6 amazing brands serving millions of Indian consumers.”

Chatter on ‘Unreal’ IPO

Numbers do the talking, and angel investor Devansh Lakhani, Director and Startup Fundraising Expert of Lakhani Financial Service has provided a blow-by-blow account of Mamaearth’s lukewarm profit run in a LinkedIn post.

“In FY23, H1 the company made a sale of Rs 684 crore with a marketing spend of Rs 272 crore. This gives them an ROI of 2.5 which isn’t that alluring. The company recorded a restated cumulative profit after tax (PAT) of Rs 3.67 crore in the first and second quarters of FY23, according to filings filed with SEBI. I doubt that investors would be interested in investing in a company that is worth 1,000 times its profit,” Lakhani stated.

Darshan Sheth from Reliance M&A called the valuations ‘atrocious’. In his scathing remark on LinkedIn, Sheth underscored how the company’s adjusted EBITDA for 1H FY23 ‘is only Rs 27 crore’. “Assuming a 5x growth in 2nd half FY23 (too aggressive), the consolidated EBITDA for the year is Rs 163 crore. The valuation being asked is $3 billion (Rs 24,000 crore). Thus EV/EBITDA is 148x!” he commented.

Now deemed to be a rumored offering, certain professionals have equated Mamaearth’s IPO figure with that of ‘value destroyers’ in the food aggregation and online payment platform verticals in India.

“The Western D2C Companies like Warby Parker, Casper, and Allbirds which had rapturous IPOs in 2021, saw crashing of their share prices by 70-90 percent and now trade at 1 times sales. Mamaearth, on the other hand, is bringing its IPO at 23 times sales! It is able to demand this valuation seemingly because it’s the first Indian D2C company to list on Indian bourse,” stated TusharKansal, Founder & CEO at Kansaltancy Ventures.

Option Value Also Vital for Correct Evaluation

Amidst all the critique, Sougata Basu, Founder, CashRich has urged the trade to give the founders “a fair chance to find the real valuation via the book-building process.” Arguing that there are several small-cap startups with initially low earnings which have performed well, he stated that the real valuation of the Gurugram-based unicorn brand should comprise DCF valuation and option value.

“The DCF valuation (based on revenue, profit, cash flow, etc.) alone will not be enough to understand the true valuation. The real option value will try to capture any major work that's underway which could result in exponential growth (not linear). If we don't understand the above concept, then by default, all startup investments will be avoided,” Basu opined.

Bringing the Dialog Back to Customer Connections

Make no mistake, as the other side of the searing debate on financial profitability and fair valuations harps strongly on the strong emotional connections that Mamaearth has made as a successful D2C brand. Some claim that a significant part of the IPO proceeds will be used on marketing spending, thus generating employment opportunities for Indian youth. Explaining how all hope is not yet lost on Mamaearth, serial entrepreneur Nishant Mittal, Founder, SpotHealth cited the example of Magicpin, which has managed to raise $100 million despite having very low brand recall, thanks to rewarding relationships with investors who trust the brand vision in the long run.

Conclusion

All said and done, Mamaearth seems to weather this particular storm quite effectively with their latest video commercial, #GoodnessResolution, greeting 2023. Originating as a baby-care label, emotions run high in the core messaging of the brand, which was evident in the commercial wherein we see a couple lamenting over a pot of plant lying on the road out of utter negligence. Soon, a schoolgirl spots it, turns it back up, and waters the plant. While many may argue how Mamaearth is pushing for its plantation drive in association with product sales, the brand might also imply big bets on past achievements, so that investors don’t hesitate to fuel their ambitious growth plan.

![[D2C 100] Yes Madam: From Marketplace to Beauty Ecosystem](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20Manyank%20Arya.jpg.jpg)

Yes Madam began its journey as a marketplace addressing critical gaps in the beauty services industry—trust, hygiene, and standardization. At a time when consumers were wary of inconsistent service quality, the brand positioned itself as a reliable, tech-enabled solution. Over the years, it has evolved into a more integrated beauty platform, combining at-home services with a growing D2C product ecosystem.

“We started with a clear mission to solve trust and standardization challenges in the beauty services space, but over time, we realized the opportunity was much larger—to build a holistic beauty ecosystem,” said Mayank Arya, Co- Founder, Yes Madam.

Transitioning to a Product-Led Ecosystem

A key milestone in Yes Madam’s journey has been its expansion into D2C products through in-house brands like Sokora and Organica Da Roma. These brands have significantly contributed to repeat customer demand, with Sokora emerging as a strong driver of customer loyalty and product adoption.

Each product is designed with a blend of science-backed formulations and sensorial appeal, aligning global skincare innovation with local consumer needs. This strategic shift has enabled Yes Madam to move beyond services and build a deeper, long-term relationship with its users.

“Our product ecosystem is a natural extension of our services business. It allows us to engage customers beyond a single transaction and build lasting affinity,” added Arya.

A Digital-First Omnichannel Model

Yes Madam operates on a digital-first, service-led omnichannel strategy. Unlike traditional beauty brands that rely heavily on physical retail, the platform follows an online-to-offline (O2O) model, where discovery, booking, and engagement are managed digitally, while services are delivered at home.

This asset-light approach enables scale without the constraints of physical infrastructure. The platform currently fulfils over 2.5 lakh monthly bookings, driven by strong repeat usage and word-of-mouth growth.

Strategic Collaborations for Cultural Relevance

Collaborations have played a vital role in amplifying Yes Madam’s brand visibility. The onboarding of Shraddha Kapoor as brand ambassador significantly boosted reach, while partnerships with personalities like Ekta Kapoor, Shweta Tiwari, and others have strengthened audience connect.

The brand’s focus on moment-led marketing—aligning collaborations with cultural trends and conversations—has helped it remain relevant and relatable.

The Road Ahead

Looking forward, Yes Madam aims to expand into new cities while strengthening its partner ecosystem. The company is also focused on enhancing operational efficiency and maintaining profitability.

“Our vision is to scale sustainably while continuing to innovate across both customer and partner experiences,” Arya concluded.

With a strong foundation in services and a growing D2C layer, Yes Madam is steadily redefining the beauty ecosystem in India.

![[D2C 100] Jiaara: The Rise of Affordable Luxury](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20jiaara.jpg.jpg)

India’s jewelry market, valued at $94–105 billion in 2025, continues to be a cornerstone of the retail sector, with strong growth projected over the next decade. Within this, the fashion and semi-precious jewelry segment—currently estimated at $1.28–4.98 billion—is undergoing a notable transformation. Consumers are moving away from purely transactional, trend-driven purchases toward more conscious, design-led consumption. This shift has opened up a significant whitespace between fast fashion and traditional luxury—giving rise to the “affordable luxury” segment, where quality, design, and meaning intersect.

A Brand Born from Purpose and Community

Jiaara’s journey reflects this new wave of retail entrepreneurship. Founded by three sisters across geographies, the brand began with exhibitions and direct selling, allowing the founders to build a strong, feedback-driven community from the ground up.

Identifying a clear gap for jewelry that is bold yet wearable, and premium yet accessible, Jiaara evolved into a digital-first brand offering handcrafted pieces made from clean metals and natural stones. The brand also places a strong emphasis on empowering women artisans, embedding purpose into its core business model.

As Ankita Singh, Co-Founder, Jiaara puts it, “Jiaara was built across geographies, but rooted in one shared belief—that jewelry should empower both the woman who makes it and the woman who wears it.”

Omnichannel as a Natural Consumer Experience

Jiaara’s omnichannel strategy is built on the understanding that modern consumers do not differentiate between channels. With a current business split of 60 percent digital and 40 percent offline, the brand leverages its website, social platforms, WhatsApp commerce, and physical touchpoints like pop-ups to create a seamless experience.

While offline channels help build trust and provide a tactile connection, digital platforms enable scale and international reach, with early traction in markets such as the UK and Australia.

Technology Meets Craftsmanship

Despite its handcrafted ethos, Jiaara is deeply invested in leveraging technology. AI and data are used across demand forecasting, marketing optimization, and customer engagement. The brand is also exploring innovations like virtual try-ons to enhance the online shopping experience.

“We use technology to scale the business, but craftsmanship to define it—both have to coexist,” added Singh.

The Road Ahead

Looking forward, Jiaara aims to strengthen its global footprint, expand its omnichannel presence, and deepen its impact by empowering more artisans.

As Singh summarizes, “The future of this category lies in affordable luxury that doesn’t compromise on design, quality, or meaning—and that’s the space we are building in.”

With evolving consumer preferences and a clear focus on purpose-driven growth, brands like Jiaara are well-positioned to shape the next chapter of India’s jewelry retail landscape.

![[D2C 100] Ubuy Eyes Global Growth as Cross-Border E-Commerce Surges](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Dhari%20AlAbdulhadi.jpg.jpg)

The global cross-border e-commerce market is entering a high-growth phase, with projections indicating it will surpass $3 trillion in the coming years. Riding this wave is Dhari AlAbdulhadi, whose platform Ubuy has carved a niche by enabling seamless access to international products across markets.

Founded in 2012, Ubuy was built with a clear vision—to bridge the accessibility gap for consumers in regions where global product availability was limited. “From the outset, our goal was to simplify international shopping by building a scalable cross-border infrastructure rather than a traditional inventory-led model,” said AlAbdulhadi.

Today, Ubuy operates across more than 180 countries, offering access to over 300 million products sourced from key global markets such as the US, UK, Germany, and Japan. The platform runs on a multi-million dollar GMV scale, backed by a robust global supply chain and fulfillment network. Its business model focuses on localized user experiences, transparent pricing, and end-to-end logistics, ensuring a frictionless international shopping journey.

The brand caters primarily to digitally savvy consumers, ranging from urban middle-class buyers to premium shoppers seeking authenticity, variety, and global access. “We are also seeing strong traction in emerging markets, where cross-border ecommerce is increasingly becoming a key consumption driver,” he noted.

Operating as a digitally native platform, Ubuy’s omnichannel strategy is rooted entirely in online ecosystems. With nearly 100 percent of transactions happening digitally, the company leverages multiple touchpoints including web platforms, mobile apps, localized domains, and even assisted commerce channels like WhatsApp. This diversified approach ensures accessibility and convenience for a wide consumer base.

Technology remains central to Ubuy’s scale and efficiency. The platform uses automation and AI to enhance product data, streamline operations, and improve customer experience. “We leverage intelligent systems to enrich product content and use AI to summarize customer reviews, helping users make quicker, more informed decisions,” explained AlAbdulhadi.

Strategic collaborations also play a critical role in Ubuy’s expansion. Partnerships with global logistics providers and localized payment solutions enable smoother cross-border transactions, while regional licensing alliances—particularly in the Gulf—support faster deliveries and localized offerings.

Looking ahead, Ubuy is focused on aggressive global expansion. “Our roadmap for 2026–2027 includes strengthening our presence in Europe, Asia, and the Middle East, with planned entries into markets like Spain and France,” he shared. The emphasis will remain on enhancing last-mile delivery, fulfillment efficiency, and overall customer experience.

As cross-border e-commerce continues to redefine global retail, Ubuy stands at the intersection of global supply and local demand, enabling consumers worldwide to shop beyond borders with ease.

![[D2C 100] How ZOFF Foods is Spicing Up India’s Modern Kitchen](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20Akash.jpg.jpg)

India’s branded spice market is witnessing strong momentum, with the organized segment projected to reach Rs 50,000 crore by 2025. Positioned within this evolving landscape, ZOFF Foods has carved a niche as a digital-first, premium spice and kitchen-solutions brand catering to modern Indian households.

“The branded spice market is still highly under-penetrated, which presents a significant opportunity for organized, quality-driven players like us,” said Akash Agrawalla, Co-Founder, ZOFF Foods. “Our focus has always been on delivering purity, convenience, and consistency to consumers.”

From Regional Startup to National Brand

Founded in 2018 in Raipur, ZOFF began with a simple yet powerful vision—to make spices fresher, cleaner, and more trustworthy. Early differentiation came through its cold-grinding technology, which preserves natural oils and aroma, along with zip-lock packaging that ensures freshness—both of which became strong brand identifiers.

Building a robust D2C foundation played a crucial role in its early growth. Direct engagement through its website and marketplaces enabled the brand to gather real-time feedback and continuously refine its offerings.

“Our D2C journey allowed us to stay closely connected with our consumers and evolve quickly based on their needs,” Agrawalla explained.

Expanding Beyond Spices

A key inflection point in ZOFF’s journey was its expansion from whole spices to blended spices and further into adjacent categories such as dry fruits, ready-to-cook gravies, and marinades. This strategic diversification has repositioned the brand as a holistic kitchen-solutions provider.

Offline expansion through partnerships with major retailers like Reliance Retail and D-Mart has further strengthened its reach. Additionally, brand-building efforts, including its association with Shilpa Shetty and onboarding Chef Natasha Gandhi as a digital ambassador, have enhanced consumer trust and engagement.

Crossing Rs 150 crore in revenue in FY26 and raising $2 million in a Pre-Series B round have marked significant milestones in its growth trajectory.

Omnichannel Growth with a Digital Core

ZOFF’s omnichannel strategy is anchored in digital, with quick commerce contributing nearly 70 percent of sales, followed by e-commerce at 15 percent, and the remainder coming from modern and general trade.

“We are omnichannel by design, but digital continues to be our strongest growth engine, especially with the rise of quick commerce,” said Agrawalla.

The Road to a Rs 1,000 Crore Brand

Looking ahead, ZOFF aims to deepen its presence across channels while expanding into new product categories. The brand is targeting revenue of Rs 250–300 crore in the near term, with a long-term ambition of building a Rs 1,000 crore-plus food brand.

“Our vision is to build ZOFF into a complete kitchen-solutions brand while maintaining profitable and sustainable growth,” Agrawalla concluded.

With a strong blend of product innovation, omnichannel strategy, and consumer-centricity, ZOFF Foods is well on its way to becoming a staple in Indian kitchens.

![[D2C 100] Traya’s Rapid Rise in Hair Wellness](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20saloni.jpg.jpg)

India’s hair loss treatment market, currently valued at over $280 million, is poised for significant expansion, with projections indicating it could nearly double over the next decade. Alongside this, the broader hair care market continues to grow into a multi-billion-dollar opportunity, creating substantial headroom for innovation in personalised wellness solutions.

Operating at the intersection of healthcare and beauty, Traya has emerged as a leading player in this space with its integrated approach combining Ayurveda, dermatology, and nutrition. The brand caters to urban, health-conscious individuals aged 25–45 across Tier I and II cities who are seeking effective, science-backed solutions for chronic hair concerns.

From Digital-First to Omnichannel Expansion

Traya began as an online-only D2C brand, leveraging digital platforms to build awareness, educate consumers, and establish a loyal customer base of over 1.2 million users. Its strong focus on personalized treatment plans and root-cause analysis helped differentiate it in a category often dominated by generic solutions.

“In FY24, we strategically expanded into offline retail to address the need for more personalized, face-to-face consultations around hair loss—an area where trust and guidance play a critical role. Since then, we have launched three stores in Mumbai, five in Pune, four in Hyderabad, and one in Nagpur,” highlighted Saloni Anand, Co-Founder, Traya Health.

Strong Growth Backed by Consumer Trust

Traya’s growth trajectory reflects the increasing demand for holistic and result-oriented hair care. The company’s revenue scaled from Rs 61 crore in FY23 to Rs 236 crore in FY24 and is projected to reach Rs 500–600 crore in FY25. Backed by approximately Rs 150 crore in funding, the brand is well-positioned to accelerate its expansion across channels and markets.

A key driver of this growth has been its ability to combine medical expertise with a consumer-first approach, ensuring both efficacy and engagement. Its digital foundation continues to power acquisition and retention, while offline stores are emerging as critical touchpoints for deeper consultation and conversion.

Expanding Holistic Wellness and Global Reach

Looking ahead, Traya’s vision extends beyond business growth to building a culture of well-being. The brand aims to raise awareness around the importance of in-depth diagnosis and personalized solutions in combating hair loss, while also protecting consumers from misleading, mass-market offerings.

In addition to strengthening its leadership in male hair fall solutions, Traya is expanding into female-specific concerns through its Santulan range, targeting root causes unique to women. The brand also plans to extend its expertise into adjacent areas such as gut health and skin health, leveraging its core philosophy of root-cause treatment.

Geographical expansion is another key focus, with pilot operations already underway in the UAE.

![[D2C 100] Comet: India’s Rising Sneaker Disruptor](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20Utkarsh.jpg.jpg)

India’s sneaker market, currently valued at approximately $3 billion, is witnessing a cultural and commercial shift driven by rising demand from Gen-Z and fashion-forward millennials. At the forefront of this evolution is Comet, a homegrown, design-first sneaker brand that is redefining how Indian consumers engage with footwear through a sharp D2C-led strategy and strong cultural storytelling.

Founded in 2022 by Utkarsh Gupta and Dishant Daryani, Comet was born out of a clear gap in the Indian market—while global brands thrived on innovation and narrative, the local sneaker landscape remained largely functional. Comet set out to change this by building a bold, culture-first brand rooted in storytelling and design differentiation. After nearly a year of development, the brand launched in July 2023 with its debut drop, Mango, a nostalgia-led concept that quickly resonated with consumers and established its unique positioning.

“Since then, we have expanded our portfolio with multiple silhouettes including xLows, Aeons, Alters, and Slides, alongside limited-edition collaborations such as Comet x Naru, Comet x Farak, “Extra Toppings Only,” and Scribble. These drops have not only driven strong organic engagement but also contributed to high repeat purchase rates, underlining our focus on product quality, comfort, and fit,” said Utkarsh Gupta, Co-Founder, Comet.

Omnichannel Strategy

Comet operates on a D2C-first model, with its website serving as the primary sales and engagement channel. This approach enables the brand to stay closely connected to its community, gather real-time feedback, and continuously refine its offerings. Complementing this is a growing physical retail presence with experience-led stores in Bengaluru, Hyderabad, and Delhi, designed to deepen brand interaction and drive discovery. While digital continues to account for the majority of revenue, offline retail is emerging as a strategic growth lever.

Expansion Plans

Over the next two years, Comet’s vision is to evolve from a fast-growing D2C sneaker brand into a leading Indian lifestyle footwear brand with strong cultural equity.

“From an expansion standpoint, we’re looking at widening our product portfolio with new sneaker silhouettes and adjacent footwear categories, while continuing to innovate on materials, comfort, and fit. Physical retail will expand selectively into key metros through experience-led stores that strengthen brand connection, supported by an increasingly integrated omnichannel ecosystem,” he added.

International exploration and strategic collaborations are also on the horizon, allowing us to introduce Comet’s design-first, culture-led approach to new audiences.

![[D2C 100] Miraggio Building an Accessible Premium Handbag Brand](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Article%20Image%20Mohit%20jain.jpg.jpg)

India’s women’s handbags and accessories market, valued at over Rs 25,000 crore, is witnessing strong growth, driven by rising fashion consciousness and an increasing shift toward accessible premium brands. Positioned within this space, Miraggio has emerged as a digital-first, D2C brand operating at a multi-hundred-crore GMV scale.

The brand caters to the modern, urban Indian woman—style-conscious, digitally native, and seeking trend-led yet functional handbags at accessible price points. By blending fashion-forward aesthetics with practicality, Miraggio has carved a niche in a category that is rapidly evolving beyond basic utility to lifestyle-driven consumption.

A Design-Led Journey

Founded in 2019, Miraggio began with a clear vision—to create a premium-looking handbag brand rooted in fast-moving fashion trends and consumer insights. Leveraging a D2C-first approach, the brand has stayed agile, with quick design cycles enabling it to remain closely aligned with changing consumer preferences.

A key driver of its growth has been its ability to build cultural relevance through strategic collaborations. Partnerships with celebrities such as Shanaya Kapoor, Athiya Shetty, Gabriella Demetriades, and Sharvari have significantly boosted the brand's visibility and strengthened its connection with its target audience.

Strong performance across its own website and leading marketplaces, combined with key funding milestones, has enabled Miraggio to scale its product portfolio and invest in supply chain capabilities. This design-led, consumer-first strategy continues to underpin its growth in the competitive D2C ecosystem.

Omnichannel Expansion and Tech-Driven Experience

While Miraggio remains deeply rooted in digital channels, it is actively building a structured omnichannel presence. The brand is set to launch its first physical store, marking a significant step toward enhancing consumer engagement and brand experience. As offline retail scales, Miraggio expects a more balanced business mix between online and physical channels.

Technology plays a critical role in driving efficiency and improving customer experience. The brand has implemented advanced inventory planning tools to enable accurate demand forecasting, optimised stock allocation, and disciplined cash flow management.

“On the consumer side, we are enhancing the online shopping journey through initiatives such as a 24/7 WhatsApp commerce bot, enabling seamless browsing and purchases. Additionally, we are developing an interactive visualization tool to address a key online challenge—bag size clarity—offering real-life comparisons and simulated views to help customers make informed decisions,” asserted Mohit Jain, Founder & CEO, Miraggio.

Collaborations and the Way Forward

Miraggio’s collaboration strategy is curated and purpose-driven, focusing on partnerships that align with its design-first ethos. Collaborations with brands like Deme by Gabriella Demetriades and select celebrity tie-ups have enabled the brand to expand its reach, drive innovation, and introduce limited-edition collections.

Looking ahead, the brand aims to accelerate growth while strengthening its position as a premium lifestyle label. Plans include scaling revenue, expanding retail presence, and creating immersive, experiential spaces. With a focus on innovation, storytelling, and consumer-first strategies, Miraggio is poised to deepen its market presence while building a strong emotional connection with its community.

India’s direct-to-consumer (D2C) industry is entering a decisive new phase. What began as a digital-first disruption led by urban startups and social media-led brands has now evolved into a deeply consumer-driven ecosystem powered by trust, repeat consumption, community influence, and cultural relevance. As the market matures, the conversation is no longer limited to customer acquisition or online visibility — it is increasingly about retention, credibility, and long-term brand affinity.

The timing of this D2C evolution aligns with India’s larger retail growth story. According to the latest report by SGA PR, India’s retail market is projected to cross $1.5 trillion by 2030, with the sector expected to grow at a CAGR of 9–10 percent between FY25 and FY30. This makes India one of the fastest-growing retail markets globally.

Yet despite the buzz surrounding digital-first brands, the report notes that D2C players still account for only a small portion of the total retail market. This leaves significant room for expansion across multiple categories, including beauty, fashion, wellness, nutrition, and lifestyle.

What is particularly noteworthy is how consumer expectations have evolved. Indian shoppers today are no longer buying products purely based on celebrity endorsements or discount-led marketing. Instead, they are increasingly prioritizing efficacy, ingredient transparency, authenticity, and community trust. This behavioral shift is reshaping the playbook for emerging brands.

Tier II and III India Become the New Growth Engine

Perhaps the biggest takeaway from the report is the rapid rise of Tier II and III India as a major driver of D2C growth. Cities such as Indore, Ahmedabad, Coimbatore, and Udaipur are no longer merely consumption hubs — they are also becoming breeding grounds for nationally scalable digital-first brands.

This marks a major shift from the earlier perception that premium skincare, wellness supplements, protein nutrition, and trend-led fashion were largely metro-centric categories. Consumers in smaller cities are now embracing science-backed skincare, health-focused food products, and premium lifestyle offerings through online channels at an unprecedented pace.

Affordable internet access, growing digital literacy, UPI-led payment adoption, and improved logistics infrastructure have significantly accelerated this trend. Additionally, aspirational consumption is rising sharply in non-metro markets, with consumers seeking products that align with evolving lifestyle aspirations rather than simply fulfilling utility-driven needs.

Rahul Jain, CEO of SGA PR, said, “India’s D2C ecosystem is becoming increasingly behavior-led, where consumers are buying into trust, communities, and cultural relevance, not just products. The founder who cracks Patna today is building something as valuable as the one who dominated Powai a decade ago.”

Digital Beauty Consumption Witnesses Explosive Growth

The beauty and personal care category continues to emerge as one of the strongest growth drivers within the D2C ecosystem. The report highlights that online beauty penetration in India, which stood at just 6 percent in FY20, is projected to rise sharply to 34 percent by FY30.

This growth reflects a larger transformation in how beauty products are being discovered and consumed. Consumers today are increasingly relying on creators, skincare educators, peer reviews, and short-form video content to make purchase decisions. Ingredient-focused conversations around retinol, niacinamide, peptides, and dermat-backed routines are becoming mainstream, especially among Gen Z consumers.

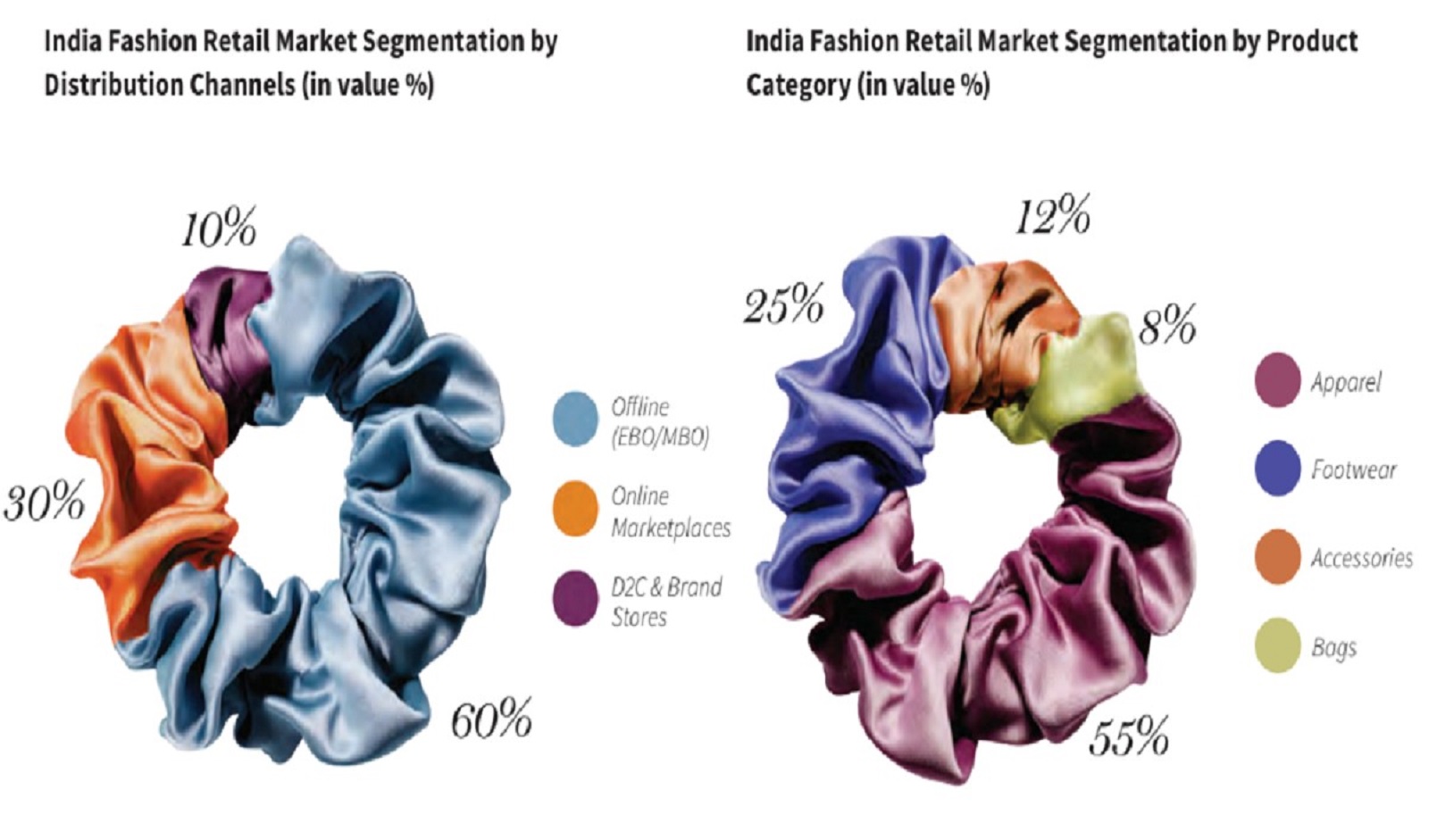

The rise of online marketplaces has further amplified this shift. According to the report, marketplaces currently contribute nearly 60 percent of fashion retail by value, while D2C and brand-owned stores contribute another 30 percent. This demonstrates how digital channels are now central to modern retail consumption patterns.

Men’s Grooming and Wellness Categories Accelerate

One of the most interesting findings from the report is the rapid rise of men’s skincare and wellness consumption in India. Men’s skincare consumption has doubled in recent years, while nearly half of Gen Z men are now actively engaging with facial care products.

This represents a major cultural shift in Indian consumer behavior. Grooming is no longer viewed as a niche or vanity-driven category among male consumers. Instead, skincare, wellness, and self-care are increasingly being normalized across younger demographics.

The wellness segment overall is also witnessing strong investor confidence. Health and wellness D2C brands alone have attracted nearly $971 million in disclosed funding, while fashion-focused D2C brands have raised close to $390 million.

Consumers are also increasingly prioritizing convenience-led wellness purchases. The report notes that nearly 45 percent of protein category revenue now comes from quick commerce and e-commerce platforms, highlighting how instant delivery is reshaping impulse-led health consumption.

Quick commerce platforms are no longer limited to groceries and essentials. They are rapidly emerging as high-frequency discovery channels for protein snacks, supplements, skincare, and personal care products — categories that traditionally relied on planned purchases.

Shark Tank India and Investor Validation

The report also sheds light on the growing influence of startup visibility platforms such as Shark Tank India in accelerating D2C growth. Around 80 percent of brands featured on the show were digital-first at the time of pitching, while nearly 30 percent subsequently secured follow-on venture capital funding.

This highlights how storytelling, founder visibility, and community engagement are increasingly becoming critical components of brand-building in the D2C ecosystem. Consumers today are not just buying products; they are investing emotionally in founder journeys, brand missions, and community narratives.

Offline Retail Expansion Gains Momentum

Even as D2C brands continue to dominate digital channels, offline retail is becoming an increasingly important growth lever. In H1 2025 alone, D2C brands leased nearly 595,000 sq. ft. of retail space, accounting for 18 percent of total retail leasing activity — up significantly from just 8 percent a year earlier.

Fashion and apparel brands contributed nearly 60 percent of this expansion, reflecting the growing importance of experiential retail. Consumers still value touch-and-feel interactions, trial experiences, and immersive brand environments, particularly in categories like fashion, beauty, and lifestyle.

This signals the emergence of a true omnichannel era, where successful D2C brands are integrating online discovery with offline engagement to build stronger customer relationships.

The Road Ahead

India’s D2C ecosystem is no longer operating in an experimental phase. It is becoming a serious force within the country’s retail economy. The next wave of winners will likely be brands that move beyond aggressive marketing and focus instead on building long-term trust, product efficacy, repeat behavior, and culturally relevant storytelling.

As digital adoption deepens across smaller cities and consumer expectations continue to evolve, India’s D2C sector is poised for its most transformative decade yet. The shift from “attention” to “acquisition” may have defined the first chapter of India’s D2C revolution, but the next chapter will belong to brands that can sustain loyalty, build communities, and remain deeply connected to changing consumer lifestyles.

![[D2C 100] Plush: From Period Care to Everyday Essentials](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Plush.jpg)

The Indian feminine hygiene market is witnessing strong momentum, currently valued at approximately $1.16 billion and expected to reach $2.29 billion by 2031, growing at a CAGR of 11.7 percent. While penetration has improved over the years, the real opportunity now lies beyond access—in upgrading the overall consumer experience. Increasingly, women are shifting from simply using available products to actively choosing options that offer greater comfort, safety, and alignment with their lifestyles.

At the center of this shift is Plush, which has emerged as one of the fastest-growing players in the category. Operating through a Q-commerce and D2C-led model, the brand has scaled to a multi-crore GMV business driven by strong repeat usage. Its core audience—urban women aged 18–45 across metros—is actively seeking better alternatives across period care, hair removal, and intimate wellness.

Plush’s journey has been methodical. In its early phase, the brand focused on deep consumer research, identifying gaps in product quality and emotional connection. Its initial offering—sanitary pads with cottony top sheets and a relatable brand voice—helped establish trust. As the brand scaled, retention, repeat purchases, and word-of-mouth became key growth levers, supported by digital-first distribution.

Omnichannel: Driven by Access and Convenience

In just a few years, Plush has earned the trust of over 1M+ consumers, emerging as one of the fastest-growing brands in its category. “We are present across leading online platforms including Amazon, Nykaa, Flipkart, BigBasket, Zepto, Blinkit, Swiggy Instamart & more while also expanding offline through modern trade partners like Health & Glow, Wellness Forever, D-Mart, Guardian Pharmacy, Apollo Pharmacy & more,” said Prince Kapoor, Co-Founder, Plush.

Leveraging Tech for Smarter Growth

The brand is also integrating technology and AI in a focused manner. Current applications include creative testing to accelerate marketing output and dashboarding tools for better decision-making. Rather than overhauling operations, Plush is layering AI into existing workflows to improve efficiency, speed, and clarity across teams.

From Monthly to Daily Relevance

Looking ahead, Plush aims to evolve into a high-frequency personal care brand rather than remaining a “once-a-month” period care option. Its two-year vision focuses on increasing usage frequency, expanding into adjacent everyday categories, and deepening consumer relevance.

In a category historically dominated by price competition and limited innovation, Plush’s growth strategy signals a broader shift—where success will be defined not just by distribution, but by meaningful product differentiation, stronger emotional connection, and consistently superior consumer experiences.

![[D2C 100] Palmonas Shaping India’s Demi-Fine Jewelry Market](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-05/Palmonas%2012.jpg)

Palmonas is at the forefront of India’s fast-evolving demi-fine jewelry segment, positioned between fine and imitation jewelry. This category is gaining strong traction as consumers increasingly seek versatile, durable, and design-led pieces that can transition seamlessly across occasions.

Built as an omnichannel-first brand, Palmonas combines digital discovery with immersive physical retail experiences. It caters primarily to modern, style-conscious urban consumers—especially women—who view jewelry as an extension of personal style. By offering accessible, premium-looking designs without the high price barrier of fine jewelry, the brand has carved a strong niche in the everyday wear segment.

A Rapid Growth Journey

Launched in 2022 as a digital-first brand, Palmonas focused on building awareness and shaping the demi-fine jewelry category from the ground up. The brand’s early success online laid the foundation for its expansion into offline retail in 2023, with the launch of its first two stores—marking a key step in validating its omnichannel strategy.

A major inflection point came in 2024 with the association of Shraddha Kapoor, who joined not only as the face of the brand but also as a co-founder. This significantly boosted category awareness and strengthened consumer trust. The momentum continued in 2025 with the brand’s appearance on Shark Tank, followed by a Series A funding round that enabled further scale. In 2026, a Series B investment further accelerated its growth trajectory, positioning Palmonas for expansion across channels and categories.

Omnichannel Strategy Powered by Technology

Palmonas operates a well-balanced omnichannel model, with approximately 60 percent of its business driven by digital channels and 40 percent from offline retail. Digital platforms remain the primary engine for discovery and demand generation, while physical stores play a critical role in building trust and offering tactile experiences that drive conversion.

The brand also leverages marketplaces and quick commerce platforms to enhance accessibility. Technology is deeply embedded across operations, with data-led insights guiding product development and identifying emerging design trends. AI-powered tools support creative production, cataloguing, and personalized consumer engagement at scale.

On the backend, integrated systems enable efficient inventory planning, demand forecasting, and supply chain visibility, ensuring speed and operational efficiency. Customer experience is further enhanced through automation and intelligent support workflows, creating a seamless omnichannel journey.

Scaling a Design-Led Jewelry Brand

Collaborations and partnerships form a key pillar of Palmonas’ growth strategy. By working with celebrities, cultural platforms, and lifestyle brands, the company creates storytelling-led collections that drive relevance and expand its consumer base. These alliances also enable experimentation with new themes while maintaining brand consistency.

Looking ahead, Palmonas aims to strengthen its position as a leading omnichannel jewelry brand in the everyday wear segment. Plans include expanding its retail footprint across key cities, deepening its digital reach, and building stronger awareness for the demi-fine category. The brand is also exploring adjacent categories, enhancing gold-led offerings, and investing in technology to elevate the overall consumer experience—while continuing to scale sustainably as a trusted, design-led brand.

![[Funding Alert] Supply6 Bags Rs 48 Cr in Funding Led by Unilever Ventures](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-07/jddebdbg.jpg) The daily supplements brand plans to strengthen its presence across D2C, marketplaces, and quick commerce after securing fresh funding of Rs 48 crore.

The daily supplements brand plans to strengthen its presence across D2C, marketplaces, and quick commerce after securing fresh funding of Rs 48 crore.![[Funding Alert] The Func Lab Bags $1.5 Mn to Expand Nutrition Biz](https://indian-retailer.s3.ap-south-1.amazonaws.com/s3fs-public/2026-06/jwednedn.jpg) The nutrition startup will use the fresh capital to grow its product portfolio, enhance distribution and scale operations nationwide.

The nutrition startup will use the fresh capital to grow its product portfolio, enhance distribution and scale operations nationwide. The Lincrusta range offers textured wall coverings for residential, hospitality and commercial spaces. Maishaa says the collection combines craftsmanship with modern design preferences.

The Lincrusta range offers textured wall coverings for residential, hospitality and commercial spaces. Maishaa says the collection combines craftsmanship with modern design preferences. XElectron has expanded its display portfolio with the launch of the ARZOPA Z3FC. The monitor offers high refresh rate performance and portability for work and entertainment use.

XElectron has expanded its display portfolio with the launch of the ARZOPA Z3FC. The monitor offers high refresh rate performance and portability for work and entertainment use.

Copyright © 2009 - 2026 Franchiseindia.com Ltd